BT Debt Collection Agency – Do You Need to Pay?

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you concerned because you’ve received a letter from BT Debt Collection Agency? Don’t worry; this article is here to help you understand what’s going on.

Every month, over 170,000 people come to our website for advice on debt matters. You’re not alone in this. We’re going to help you figure out:

- Who BT Debt Collection Agency are, and what they want.

- If BT Debt Collection is a real firm.

- If you really need to pay or if you can ignore the letter.

- How to handle the situation if you can’t afford to pay.

- What happens if you don’t pay.

We know how scary it can be to get a letter from a debt collector. Our team has faced this too. We’re here to guide you and help you feel less scared.

Let’s dive in!

Who is BT Debt Collection, and what do they want?

Nearly every company has a debt collection agency that they use when payments fall behind. Some of the larger companies have their own in-house debt collection department. In the case of BT, the telecommunications company, they have BT Debt Collection, otherwise known as BT Debt Recovery Unit, which carries out the initial debt recovery.

BT Debt Collection will have sent you a letter if you have fallen behind on your BT payments.

This includes all connectivity options, such as broadband, landline telephone and mobile networks.

What are my next steps?

It’s never nice getting a letter that says you owe money – after all, they often come when we’re least expecting them. The worst thing you can do in this situation, though, is to ignore the letter. This won’t make the debt or BT’s debt recovery unit go away – in fact, if you leave it too long you could actually end up being taken to court and there’s even the possibility of a prison sentence if things really escalate.

Here are some top tips about the next steps to take if you’ve had a letter from BT Debt Collection:

Keeping a diary

From the moment you get that first letter, make sure you keep an accurate diary about your process in dealing with BT Debt Collection. Note down the date and the times of the letters and the phone calls you receive from BT Debt Collection.

By doing this, if they accuse you of any shortcomings, you will have an accurate and precise record of all your correspondence with them.

Follow our ‘prove it’ guide with letter templates and get them to prove that you owe the money.

Gathering information

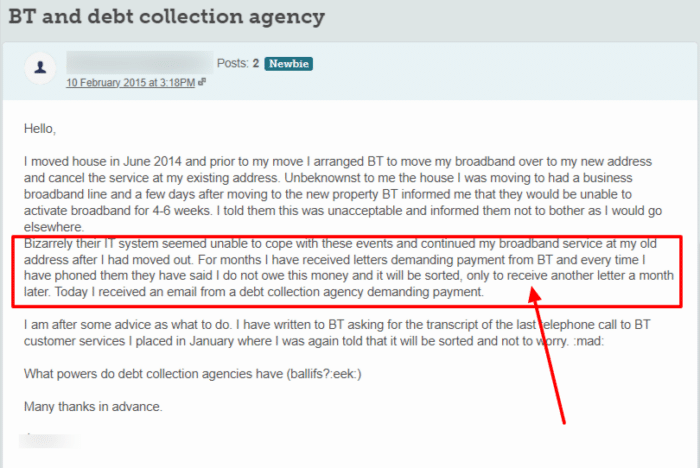

You might think that the debt isn’t yours. Unfortunately, debt collection agencies like BT Debt Collection rarely send letters in error. However, it is good practice to go through all your bills and records and cross-reference all your information with what BT Debt Collection is claiming you owe.

This is really important to do, because if they have made the slightest mistake, you might not have to pay the debt. You can also see if they’ve added any interest to the original amount. Take a look at this example.

This person did the right thing by asking for evidence that the debt is theirs. That said, they might have been better off asking the debt collection company for proof rather than BT. If you are in a similar situation and aren’t sure who to contact for proof, you can contact a debt charity for some free and specific advice.

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Is your debt statute barred?

If it has been 6 years – or 5 years in Scotland – since you last paid towards your unsecured debts and you have not written to your creditor about your debt during this time, it is statute-barred.

This means that the debt is not enforceable. It still technically exists, and you still technically owe the money, but there is no legal way for you to be forced to pay or for the debt to be enforced.

Keep in mind that not all debts become statute-barred!

Any HMRC debts, for example, will stay enforceable for decades. Any debt that had a County Court Judgement (CCJ) attached to it during the 5 or 6-year window will be enforceable for the duration of the CCJ.

If your debt is statute-barred, you can use my free letter template to write to BT and explain the situation.

If you are unsure about the status of your debt, you can contact a debt charity for some advice. Their advisors will be able to look at the debt in question, determine its status, and advise you on your next steps.

Paying the debt

If you have gone through these previous steps, and you’re certain that the debt is yours, and you also have the financial means to settle the amount, you should pay them. By doing this, you will stop BT Debt Collection from sending you any further letters or making any further phone calls.

Not being able to pay the debt

If you aren’t able to pay the debt in full, you should be active and get in touch with BT Debt Collection as soon as you can. BT Debt Collection has a very useful document that lays out the process they go through with regards to debt collection, which you can find on this page.

To summarise the options they offer if you cannot pay the bill in full:

» TAKE ACTION NOW: Fill out the short debt form

What Happens If I Don’t Pay My Debts?

We’ve all wondered – what exactly will happen if you stop paying off your debts? Well, the answer is a whole lot of bother.

- Your creditor will send you reminders and then demands to get you to pay any missed payments

- If you don’t pay, your account will default

- If you still don’t pay your debts, your creditor can choose to sell your debt to a debt collection agency or employ an agency to chase you for the missed payments. This is where BT’s debt collectors will come in.

- If you don’t pay the collectors, your creditor or the collection agency might be able to take legal action against you to get their money back. Legal action usually starts with a CCJ.

Can I get a debt solution?

If you are facing financial hardship so that you can’t pay for your debts, even if you were liable, you might want to consider a debt solution.

There are several different debt solutions available in the UK, so I recommend speaking to a debt charity as soon as possible. Their advisors will be able to look at your finances in detail and help you work out which debt solution will work best for you.

I have linked a few charities that offer these advisory services for free below.

Debt Management Plan (DMP)

A DMP is an informal debt solution that lets you pay off your debts via a single monthly payment.

Because it is informal, it is not legally binding so you are not tied into a DMP for a minimum number of payments.

Individual Voluntary Arrangement (IVA)

An IVA is a formal agreement between you and your creditors. You agree to pay a monthly sum that is distributed amongst your debts, and your creditors agree not to contact you during your IVA.

IVAs typically last for 5 or 6 years, and any outstanding debt is wiped off when it ends.

Keep in mind that IVAs are not suitable for everyone. You need to owe several thousand pounds to more than one creditor to be eligible. You also need to demonstrate that you have some disposable income every month.

Trust Deed

IVAs are not available in Scotland. Instead, you will need to opt for a Trust Deed.

Trust Deeds work in the same way as an IVA – you pay an agreed sum each month that is shared amongst your creditors, they can’t contact you, and any leftover debt at the end of your Trust Deed term is written off.

Debt Relief Order (DRO)

A DRO is a good option for those facing financial hardship with no assets and little income.

For 12 months, you make no payments, but your creditors freeze your interest and don’t contact you.

If your finances haven’t improved during this year, you may be able to write off your unsecured debts.

Bankruptcy

If you have debts but no realistic possibility of ever paying them off, you may need to declare bankruptcy.

Bankruptcy has an unfair stigma attached to it as it may be your only way of getting a financial fresh start. That said, it is a serious financial situation that should not be taken lightly.

Sequestration

Sequestration is the Scottish version of bankruptcy.

If you have little income and no valuable assets, you may be able to apply for a minimal asset process bankruptcy (MAP). A MAP is a quicker, cheaper, and more straightforward version of sequestration, so worth considering.

Checking for Other Debt Collectors

There are a lot of ways to get into debt. In fact, it’s not uncommon to owe money to several companies at once.

Perhaps you have a mortgage, a car loan, a couple credit cards and an item or two you bought on buy-now-pay-later schemes. It’s easy to lose track.

That’s why it’s important to regularly check your credit report and bank statements to make sure you haven’t missed anything.

If a debt collector has purchased your debt, it appears on your credit report.

Some of the debt collectors you’re most likely to come across are PRA Group, Lowell and Cabot Financial.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

How do I make a complaint against BT’s debt collectors?

If you think that the debt collectors BT have authorised to chase you debt have been unreasonable or behaved inappropriately, you can make a complaint. You can also make a complaint if you feel that they have broken any of the Financial Conduct Authority’s (FCA) guidelines.

Make your first complaint to BT debt collectors so that they have the chance to sort out the issue themselves. If you feel that they have not taken your complaint seriously enough or have not addressed your issue properly, you can escalate matters.

You can make any secondary complaint to the Financial Ombudsman Service (FOS). They will investigate and, if your complaint is upheld, BT’s debt collectors may be fined. You could even be owed compensation.

BT Contact Information

| Address: | BT Group plc, 1 Braham Street , London , E1 8EE |

| Phone: | 020 7356 5000 |

| Twitter: | @btbusinesscare |

| Website: | https://www.bt.com/ |