MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you wondering how credit cards work? You’ve come to the right place. Each month, more than 170,000 people visit this website seeking advice on debt.

In this article, we’ll address the following questions:

How do credit cards work?

What will happen if you’re unable to pay your credit card bills?

Is it possible to negotiate credit card debt?

How does credit card balance transfer work?

What credit cards can you get?

Will credit cards affect your credit score?

We know that credit cards can be a bit confusing. But don’t worry; we’re here to help you figure things out and make an informed decision.

Let’s dive in!

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

How Do Credit Cards Work?

A Credit card is a plastic card which you can use to purchase items or services. You can also use a credit card to withdraw money from a cash machine.

Credit cards can be issued by banks, finance companies, clubs and some stores.

Credit Limit

You’re only allowed to spend up to a certain amount on your credit card every month. This monthly limit is known as your Credit Limit. How high or low your credit limit is depends entirely on your financial circumstances.

Balance

Every time you purchase goods or services using your credit card, that amount is added to your account. This amount is what you owe and it’s known as your Balance.

Interest-Free Period

Credit cards have an interest-free period for you to pay off your balance. As the name suggests, this is the period where no interest is charged towards the amount that you owe. Usually, this period is anywhere between 20 to 55 days long.

After this period, your credit card company will start charging interest on the amount of money you owe. It’s a very good idea to pay off what you owe before the interest-free period ends because credit cards usually have very high interest rates.

You can opt to look for credit cards that have special offers according to which you are not charged interest even if you don’t pay off your balance entirely.

Your credit agreement will give you all the details about how long your interest-free period will be as well as how much interest will be charged once that period ends.

Statement

Your credit card company will send you a statement every month which will have complete details about your payments as well as the amount you owe.

Here are the details that your statement will contain:

Details about each purchase you’ve made using your card since your last statement.

Details about how much interest you’re being charged currently as well as any additional charges on your account.

The amount of money you owe, i.e., your balance.

The minimum payment you can make towards your balance.

The date by which you must make your payment.

How and where you can make your payment.

Your provider’s contact details.

Your statement can be a great tool for figuring out your repayment plan as well as for recalling how much you owe in case you forget.

Be sure to check your statement thoroughly every time you get it and make sure all the information is correct. If you spot a purchase that you feel is incorrect, contact your provider immediately to get it removed.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

What will Happen if I’m Unable to Pay My Credit Card Bills?

According to your credit agreement, you have to make at least the minimum payment towards your balance. But what if you can’t afford to do that?

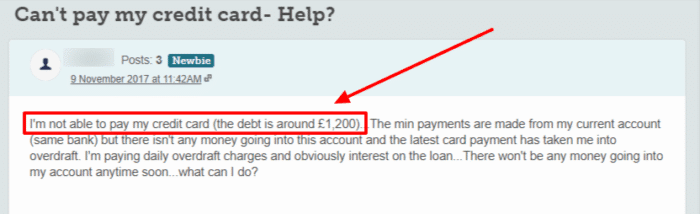

Unfortunately, lots of people find themselves in a similar position to this forum user.

If you don’t make this payment, then:

Your creditor will contact you inquiring about why you have not made the minimum payment and will request you to make the payment as soon as you can.

After this, if you wait too long or just simply refuse to make the payment, your account will default

If you still do not pay back the money you owe, further action could be taken against you such as debt collectors being hired to collect money from you.

Your creditors could also take out a County Court Judgment (CCJ) against you which could cause bailiffs to come to your home and seize your goods in order to pay back the money you owe.

Is it Possible to Negotiate Credit Card Debt?

If you’re falling behind on your payments and have a valid reason for it, you can definitely contact your provider and explain to them why you’ve been falling behind.

Explain to them why you have been missing payments and they may offer you a reduction in the amount you owe or a payment holiday so that you have time to get your financial affairs in order.

You can contact an independent charity for free debt advice such as StepChange or National Debtline. They can analyse your financial situation and give you advice about what the best course of negotiation with your provider could be.

You can also contact an independent charity for advice on a debt management plan. They can help you plan it which you can then propose to your provider.

Debt Management Plan

A debt management plan (DMP) is an agreed-upon payment schedule between you and your creditors which states the amount and number of payments you’ll be making to them each month.

You can work out this plan by analysing your income and expenditures and seeing how much money you can set aside to pay towards your credit card debt.

If you have multiple credit cards, you can make minimum payments towards all of them if they are sufficient enough to pay off the debts completely and keep you out of persistent debt.

If this is not the case, then you should make minimum payments to all of your cards except for the card that has the highest amount of money you owe. For this particular card, you should make payments larger than the minimum payment.

Be sure to pay priority debts first before you start paying non-priority debts like credit card debt. Priority debts are payments that can have serious consequences if you don’t pay them. This can include council tax arrears, rent arrears, etc.

Also, be sure to take care of your basic living costs and expenditures first before you start making payments towards credit card debt. Never feel pressured to pay more than you can afford.

Most credit card providers and companies registered in England are authorised and regulated by the Financial Conduct Authority. Thus, they have to stick to a close set of rules when pursuing you for your debt.

Always know that even if you cannot afford to pay your debt, there are many options out there for you to explore. Do your research and reach out to a professional that can help you. It’s a very good idea to reach out to a professional debt charity for advice if you are in debt that you cannot afford to pay.

Not only will they give you advice on which debt solution would be best for you but they will also build upon this advice by telling you how to apply for that solution and set it up.

I always tell my readers to seek advice from an independent charity rather than a private debt management company. This is because the latter will charge you for their advice whereas the former will give it to you free of charge.

If you have a lump sum of money that is quite large but not as large as the amount you owe, you could opt for a ‘full and final settlement’ offer.

A full and final settlement is usually less than the amount you owe but your creditors will be willing to accept it if it’s a one-time lump sum payment. Be sure to seek advice from a professional if you’re considering this option.

Is it Possible to have Joint Credit Card Debt?

According to the law in the UK, a credit card can only be in one person’s name. Due to this, it’s impossible to have “joint credit card debt”.

That being said, you can definitely ask your provider for a second card for your spouse or child to use.

Keep in mind, however, you will still be responsible for the money spent on these cards. The second card holder is not liable for the money spent on the card. Only the primary cardholder, i.e. you, is responsible for the balance owed on a credit card.

How does Credit Card Balance Transfer Work?

Some credit cards allow you to transfer the balance to another card. This can actually be a great way to reduce your debt.

You can do this by transferring the balance from your current card to a card that charges a lot less interest than your previous card did. This can help you pay off your debt a lot faster.

While this is definitely a great way to reduce your debt, it can prove to be quite difficult. This is because getting a credit card with low or 0% interest can be very hard if you have a poor credit score, which you most likely will since you’re trying to pay off debts.

You should also keep an eye out for transfer fees when transferring your balance. In most cases, this fee is 2 – 3% of the total amount you’re transferring.

Once you completely transfer the balance over to a new card, I advise that you cut up your old card and throw it away as well as close your old account.

This is because if your old account is still active, you may be tempted to spend money on it and then you’ll end up with two debts instead of one.

What Credit Cards Can I Get?

There are lots of different credit cards available, so knowing what is right for you can be difficult. You can contact a debt charity for some advice if you need it.

Here is a quick breakdown of the different cards available:

Reward cards: This card will give you rewards when you use it. These rewards can be anything from air miles to store discounts. These cards can have high interest rates.

Credit builder cards: These cards could be a good option for those who want to build a positive credit history.

Balance transfer cards: You might be able to reduce your total interest by combining your credit card debts onto one card.

Purchase cards: These cards can be a good option if you need to make a big purchase but they do have strict criteria to qualify.

Money transfer cards: A transfer card essentially lets you borrow money. You transfer money from the card to your bank account and usually pay a small fee.

Will Credit Cards Affect My Credit Score?

Yes, credit cards can affect your credit score.

Once you have missed a few payments or defaulted on an account – which negatively impacts your credit score, too – your debt might be sold to collectors, it will appear as a second collection account on your credit file, and the original entry may be marked as ‘sold’ which doesn’t look good!

If they don’t add a second entry to your credit file, the entry for your original debt can be changed to add the debt collection company’s information.

While it is unlikely that they will do this for smaller debts, they have the legal right to.

These collection accounts will negatively impact your credit. They are visible for 6 years and will impact your ability to get credit or use some credit products during this time.

This is because companies use your credit file to see if you are a ‘high-risk’ customer – someone who might have difficulty paying their bills on time. If you continue not paying until you have a CCJ against you, you have had such trouble paying back your debt that someone had to go to court about it.

Understandably, companies are going to be reluctant to give you credit!

After 6 years, it is no longer visible on your credit report, and you should find it easier to get credit again.

You also need to be aware that any debt solutions that you use will also be visible on your credit file for 6 years, and your credit score may be affected. However, once these 6 years are over, your debt solution will no longer be visible, and you may find it easier to get credit again.

That said, using credit cards responsibly can help you improve your credit score. If you can use your cards and make all of your payments on time, you will build a positive credit history. Positive credit history looks good to potential lenders and can help you get more competitive credit.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

The first step to staying out of credit card debt is to realise that it’s definitely possible to use your credit card regularly and stay out of debt.

The trick to this is to only use your credit card for purchases based on the cash you have in hand. This means you should try to only use your credit card as a convenient payment tool, not as a debt instrument.

If you only make purchases that you’re sure you’ll be able to pay for immediately when your credit card bill comes, then by all means, go for it. However, if you feel you’re going to be having trouble paying it back, you may want to reconsider it.

My advice would be to have a self-imposed spending limit on yourself in addition to your credit limit.

Short-Term Loans can be Beneficial at Times

Some readers may disagree with what I’ve said above and might be of the opinion that using credit cards in this way would be minimising their potential.

I agree with this sentiment to an extent; Sometimes, using your credit card to make a purchase that you can’t pay for immediately can be a smart move. However, it’s important that you’re able to pay off your balance as quickly as possible. The reason for this is the high interest rate on credit cards.

Thus, if you can’t pay for something all at once but are sure you’ll be able to pay for it in short-term instalments (4 – 5 months), you should use a credit card for it. You can seek advice from a professional if you’re unsure if you’ll be able to make the payments in a short amount of time.

However, if you feel you’ll be making minimum payments towards your balance for months on end, I suggest you don’t make such a purchase using your credit card. This can lead to persistent debt and you may reach a stage where you’ve paid more in interest than you have towards the actual original debt.

Be Wary of Your Credit Limit

When you first start out with your credit card, your credit limit will most likely be very low. This will automatically stop you from spending too much money.

However, over time, your credit limit will begin to increase. Thus, it can definitely be very tempting to spend a lot more money once the credit limit has increased.

You must keep in mind that even though your credit limit has increased, more likely than not, your financial budget has not. Thus, you must keep yourself in check and ensure you’re not making extravagant purchases that could drown you in debt.

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.