Debt Consolidation Loan with No Credit Check

Getting a debt consolidation loan with no credit check can be tough as most money lenders use credit checks to measure risk.

In this article, we’re going to help you understand your choices. Our website guides more than 170,000 people each month on money matters.

Here’s what we’ll go over:

- What a debt consolidation loan is.

- The true cost of a bad debt consolidation loan.

- How your credit score is worked out.

- What debts you can fix with a consolidation loan.

- If getting a debt consolidation loan is a good idea for you.

We understand that dealing with debt can be hard, but remember, you’re not alone. There are many ways to manage debt, and we’re here to help you understand them.

Let’s start learning more about debt consolidation loans with no credit checks

Debt consolidation in a nutshell

Debt consolidation is when you pay off multiple existing debts using new credit. For example, you might want to borrow a lump sum that is enough to pay off personal loans, store cards, credit cards and any other type of credit you may have. Instead of managing these smaller existing debts with different monthly repayments, debt consolidation allows you to make just one monthly payment to repay the new loan you took out.

There are different ways of refinancing debts. The two most common methods are using a consolidation loan or a balance transfer credit card. The latter is a consolidation method only suitable for people with credit card debts by transferring those balances to a new card. We’ve provided more details in this guide on clearing debts on your credit cards.

We explain the former in more detail below.

Debt consolidation loans no credit check

When you apply for a debt consolidation loan, it is almost certain that the lender will conduct an affordability assessment to check your credit score. The FCA does not have a hard and fast rule to say they must do this, but they do say:

“The CONC 5.2.1R requirement is to make a reasonable assessment of creditworthiness based on sufficient information, obtained from the borrower where appropriate and from a credit reference agency where necessary.”

If the lender didn’t check your score via a credit reference agency, they would be vulnerable to being penalised by the FCA for irresponsible lending. If you have been searching for a debt consolidation loan with no credit check and have yet to find one, this is probably the reason why.

Loan providers do not want to risk sanctions and potentially heavy fines by not checking your file. The FCA has a track record of coming down with a heavy fist on irresponsible lending techniques.

Hard vs soft checks

When lenders look at your credit file after applying for credit, they do a hard search. Unlike a soft search, the lender flags your file so other lenders know you have applied for credit. It essentially leaves a credit footprint. Doing so makes other lenders aware that you may be in financial trouble, especially if you apply for lots of credit quickly, resulting in many hard searches and flags.

If you find lenders offering debt consolidation loans without checking your credit score, you should be cautious. There is a chance that they are not a legal lender.

This is not the same as getting an application determination before a credit score is checked, which some lenders offer. Such a determination can give you an idea of the outcome of your application without leaving a hard search flag.

Debt consolidations loans for all purposes

- Stuck paying high interest on credit card debts & loans?

- Looking for a better interest rate?

- Stuck with the confusion of multiple repayment plans?

Polly

“This was by far possibly one of the nicest experiences I’ve had getting a secured loan.”

Reviews shown are for Loans Warehouse. Search powered by Loans Warehouse.

Will I qualify for a debt consolidation loan?

Common debt consolidation loan eligibility criteria include a sustainable source of income, the ability to make repayments, and reasonable credit history.

Experian is a reputable credit reference agency in the UK, and they state that debt consolidation loans usually require a “good” or “excellent” credit score. However, you can still access debt consolidation loans with bad credit history, but you may be offered a higher interest rate. This is one of many alternate options we discuss in detail further below.

The FCA allows each lender to determine how they use the information from your credit file. Whereas one lender could reject you, another might not. So, there is no stringent credit score you require.

As I see it, shopping around for the most favourable terms and making an interest rate comparison before committing is a good idea.

» TAKE ACTION NOW: Compare deals from the UK’s leading lenders

Can a consolidation loan be declined?

Yes. You can be refused a debt consolidation loan for several reasons. Loan rejection reasons include poor credit rating, too much debt, and insufficient income. You can improve your chances by checking and improving your credit score. There are also plenty of alternative debt management solutions if your loan application is declined.

If you’re feeling stuck, you can always seek free financial advice from a reputable debt organisation like the National Debtline.

Will a debt consolidation loan affect your credit score?

Applying for a single loan to consolidate debts will not negatively affect your credit score. However, your score will be impacted if you apply for multiple together or fail to meet your monthly payments.

Applying for a debt consolidation loan causes the loan provider to search for your credit file. This type of search is known as a hard search because the lender will also flag that they have been looking. This is to let other loan providers know that you have made an application. Suppose you apply for lots of credit in a short period. In that case, multiple hard search flags will be applied, signalling to other providers that you could be in financial difficulty and to be cautious before agreeing to credit.

The only other way that debt consolidation can harm your credit file is if you do not keep up with repayments. You could even be taken to court and face bailiffs if no repayments are made.

However, if you consistently repay your debt within the agreed timeframe, you can actually improve your credit score. In turn, this can have a positive effect on future borrowing.

What debts can I resolve with a consolidation loan?

A consolidation loan could be used to pay off a range of current debts and arrears, not limited to credit card debt, unsecured loans, catalogue debts, and even household debts such as unpaid energy bills.

Is it a good idea to get a debt consolidation loan?

There is no way of saying 100% that consolidating debt is the right move for you. Suppose you can reduce your monthly payments into just one monthly repayment. In that case, it should make managing your finances easier and safeguard you from accumulating more debt and damaging your credit file.

However, you must access the full loan amount needed to consolidate, and it’s essential to find a lower interest rate to save money on repayments. Without these factors, debt consolidation may not be a good idea.

It’s highly recommended to speak with a debt advice charity regulated by the Financial Conduct Authority (FCA) first. They could identify a more beneficial solution based on your circumstances and credit score. Or they could support you in getting debt consolidation right. They also offer free impartial debt advice tailored to your personal situation.

Potential risks of debt consolidation

Before applying for a debt consolidation loan, you should know the potential pitfalls. For instance, if you extend the loan term, you will need to pay more interest over time. Some loans come with added fees, and you may be charged if you wish to make an early repayment. Additionally, if you cannot manage your spending wisely, you could get into a debt spiral.

It is essential to carefully read and understand loan terms before signing anything. This way, you can avoid nasty surprises such as hidden fees.

Feeling like Chandler?

All of this information can feel a bit overwhelming.

Don’t panic! There’s plenty of help available.

After lots of research, I decided to partner with Loans Warehouse. They’re an award-winning service who can help find the right loan for you.

You can find out what’s available for you below.

Fill out this short form to get started

Your alternative options

Just because you are unlikely to find a debt consolidation loan without a credit check doesn’t mean you can’t consolidate your debts or get out of debt another way. I’ve put together some alternative options you may be able to use.

- Debt consolidation loans for bad credit

Debt consolidation loans for bad credit are advertised widely online. You won’t find these with the big high-street banks, but they are advertised with some legitimate online loan providers. A debt consolidation loan with bad credit is advertised as being easier to be approved for. The downside is that you are at a greater lending risk, so the interest rate you’re offered is likely higher.

Some lenders that offer bad credit debt consolidation loans are:

- Consolidation Express

- Ocean Finance

- Norton Finance

- Likely Loans

- Lending Works

- Solution Loans

- Creditfix

These providers may not have the best interest rates. They are listed to show that some advertise consolidation credit for people with a low credit rating.

- Debt consolidation loans with a guarantor

An unsecured debt consolidation loan with a guarantor is for people who cannot get approved for a debt consolidation loan on their own because they have a significantly bad credit history. Or you could decide to go down this route instead of the bad credit loan lenders above to try and get a better interest rate on the loan repayments.

The guarantor becomes responsible for the debtor to pay back the loan on time and in full. If the credit is not repaid as agreed, the guarantor also becomes accountable for refunding. Most guarantors are partners, parents or extended family. The guarantor’s credit history may be checked before approval, or they may need to own a home in the UK at a certain age.

Here are some options if you are considering applying for a debt consolidation guarantor loan:

- TFS Loans

- Buddy Loans

Again, the interest rates offered by the providers above may not be the best on the market. They are just examples of where you can find guarantor loans.

- Debt Management Plan

A Debt Management Plan is an informal debt solution that is regarded as very similar to debt consolidation without actually consolidating your debts. The bonus with this method is that you don’t have to apply for any more credit, so your credit history won’t get checked.

You don’t have to worry if you have poor credit.

So, how does it work?

In England and Wales, you can ask existing creditors to agree to a plan to make one monthly repayment proportionally split between everyone you owe. For example, one lender may receive a larger cut from your monthly repayments because you owe that lender more than you owe another one.

This is similar to debt consolidation because you now only have to make a single monthly payment rather than juggle all creditors at different times of the month. Monthly budgeting is advisable to ensure you can afford the agreed-upon payments.

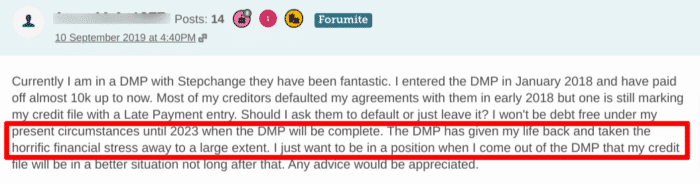

As you can see above, this MoneySavingExpert forum user enlisted the help of debt charity StepChange and is successfully paying back their debt with a DMP.

To organise a DMP, you can arrange it yourself, pay for financial services or get an equivalent service from a debt charity. Informal debt solutions are not legally binding and can give you more flexibility in managing your debts.

There’s an equivalent to this in Scotland known as a Debt Arrangement Scheme (DAS).

- Secured loan

Secured loans use your assets as collateral in the event of failure to repay the secured loan. They depend less on your credit score than unsecured loans because the asset reduces the risk the creditor can claim from you.

Secured loans to consolidate debt are not as common, but they are not impossible. They are usually available in the form of remortgaging and second charge property loans. Bear in mind that remortgaging to consolidate debt has implications, such as early repayment charges.

It’s essential to avoid illegal loan sharks offering secured credit.

Before committing to a loan, ensure the lender is authorised by the FCA.

- Other debt solutions

If none of the above options are available, there are other ways to get out of debt. A debt advice charity could help assess your options based on your personal finances. For example, you may be able to write off all of your debt with a Debt Relief Order (DRO) or make significant debts affordable with an Individual Voluntary Arrangement (IVA).

Filing for bankruptcy is also an option, although from my experience it is a last resort for many people.

Some exceptional debt advice charities registered in England, Wales and Scotland can also help. They include StepChange and Citizens Advice. It is best to consult these organisations for financial counselling before deciding how to get out of debt.

From my experience, getting advice early can save you money and time.

More debt consolidation loan FAQs answered!

MoneyNerd covers plenty of FAQs on debt consolidation. Search our site with your questions for explanations, definitions, and reviews.