MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Getting a mortgage when you have a Debt Management Plan (DMP) can feel tough, but don’t worry; this article is here to help answer your big question: ‘Which mortgage lenders accept DMP?’

Every month, over 170,000 people like you come to our website seeking advice on debt solutions. We’re experts in this field, and we understand your concern about how a DMP might affect your chance to get a mortgage.

In this article, we’ll cover:

What a Debt Management Plan is and how it works.

How a DMP can affect your mortgage options.

The different types of lenders who may accept a DMP.

The pros and cons of working with a mortgage broker.

Other possible options if you’re struggling with debt.

Many of us have been in your shoes, as we’ve dealt with debt and understand the stress it can bring. It’s our mission to guide you through this process and help you find a solution that fits your needs. Let’s dive in and start exploring your mortgage options after a DMP.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

What are Your Options to Get DMP Mortgages?

Don’t worry if you have been rejected by commercial banks or mainstream lenders due to your credit history or credit issues. There are some Mortgage Solutions for DMP Holders that you can explore:

Bad Credit Mortgages Lenders

If you have been rejected for a mortgage due to your bad credit score or credit record by high street lenders. Many institutions might be able to help you. These institutions usually accept people with low credit scores on their credit files.

You might get a mortgage if you apply to these institutions. This is a link that shows the best financial companies that offer mortgages to people with low credit on their credit files.

They also have a bad credit mortgage calculator that you can use to know more about the details of your mortgage. However, you can expect to pay more with bad credit mortgage lenders as you face higher interest rates and fees throughout the process.

This means with a higher charge to pay on your mortgage overall, it might become unaffordable and land you in more debt.

Help to Buy Scheme

There are UK Government schemes for home buyers, which were started a few years ago. This scheme provides equity loans to persons who are building their homes for the first time.

The loan values might be different depending on where you live in the UK.

You can apply to this scheme only if you are purchasing your first house. Those who are opting for their second house or looking to rent the property out might not be able to avail of this scheme.

A direct lender is a person who lends to you directly without any involvement of a third party.

Direct lending is usually secured against collateral because it is a high-risk venture for your potential creditors. The debt amount might be paid to you in a lump sum and your home may be repossessed.

Mortgage Brokers or Credit Reference Agencies

Mortgage brokers are specialist lenders finders. Their specialist area is to find lenders and persons who need the money.

Usually, the agreement has a mortgage with a settled amount of interest and a down payment, which is fixed by both parties. Mortgage brokers charge a fee for their services.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

There are no direct implications of a DMP with an existing mortgage, however, there are some indirect problems that might occur if you have a DMP as well as a mortgage.

Handling mortgages for people is quite difficult at times. If you have a DMP with a mortgage, the mortgage payments might be disturbed. It might be hard to keep up repayments on your mortgage at the same time as clearing debts that you owe to people might harm your financial life.

Can You Get a New Mortgage with a DMP?

Debt management plans and home ownership might not be as easy as it seems. Usually, the institutions that allow mortgages are commercial banks that are authorised and regulated by the financial conduct authority.

Your DMP mortgage eligibility will depend on quite a few factors. These institutions or lenders conduct risk and gearing analysis to minimise the chances of loss on their part.

Applying for a mortgage might be difficult if you have a DMP because your chances of not paying back are higher compared to a person who doesn’t have a DMP along with their mortgage application.

This is because you might have problems keeping up repayments of your mortgage and debts at the same time and it may put off the whole mortgage scheme. This will bring youcredit problemsas well.

Hence, your credit report will be analysed and every detail of your credit report will be a crucial factor in the success of your application. Things such as how old the DMP is, other marks on your credit report, and if your DMP has been satisfied, how long ago it was settled.

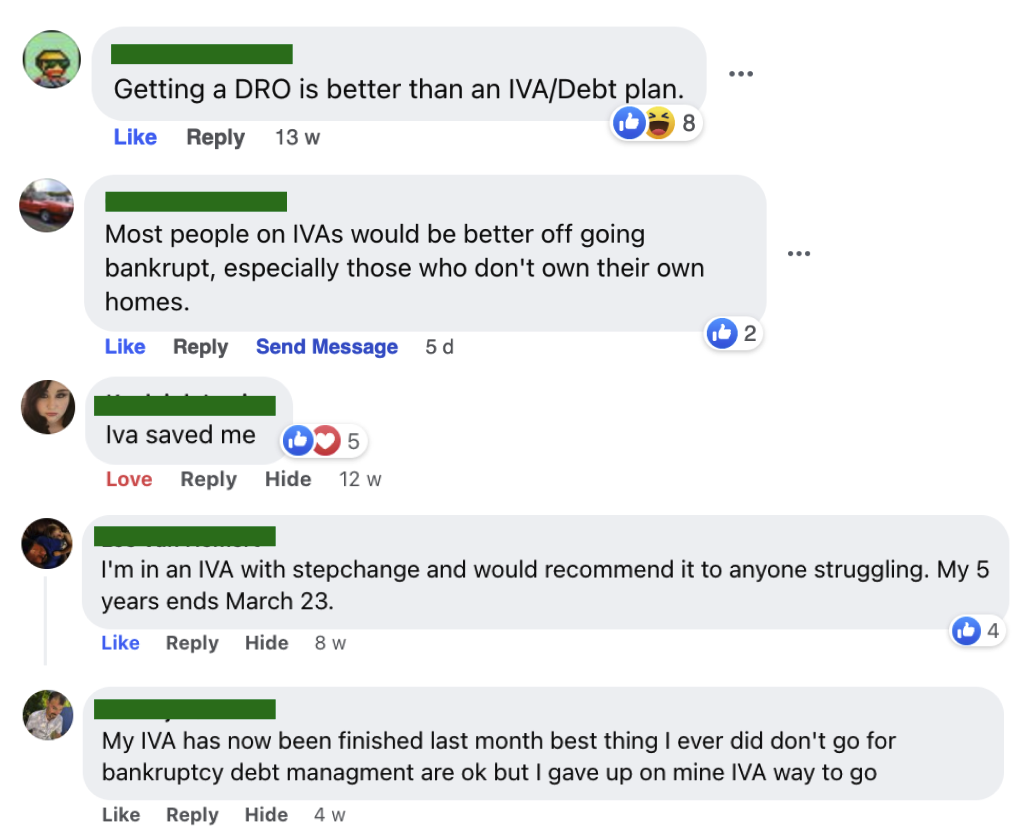

You can see here this user of MoneySavingExpert struggled to find a lender 7 months after they’d paid off their DMP. However, it does show that you can use specialist brokers to help obtain the loan you need.

You might be able to get a good mortgage deal even though you have a DMP, this depends on the bank and your credit scores.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Deciding how to tackle your debt is a very personal decision and you certainly can’t get the answer through a simple blog post. It’s made worse by the strong opinions you’ll often find online.

The best option is to get help from a debt expert to find out all your options and see which is right for you.

I’ve partnered with The Debt Advice Service and you can access their expert support by filling out the short form below.

DMP does not directly affect your credit rating but if you are unable to pay your debts back, such as credit cards debt, etc. It might affect your financial score and credit events.

Are DMP and IVA the same?

No. DMP is not similar to IVA. IVA is a solution to avoid bankruptcy and has major drawbacks and limitations on your financial life. Debt management plans are used as a strategy to remove debt and pay them back.

Is it a Good Decision to get a DMP mortgage?

There is no straight answer to this question. It depends on what your circumstances are and how well you can manage the debt repayments along with the non-priority debts.

Hence, if you deem yourself capable of managing a Debt management plan with a mortgage, you might do so.

What are the best DMP companies?

Many good companies are giving sound and solid mortgage advice. Many high street banking institutions are also good. This article refers to the best companies for DMP.

How to Apply for a Mortgage?

You can apply for a mortgage by filling out a mortgage application with mortgage specialists lenders. The form usually holds private information and other relevant information.

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.