MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

If you’re worried about paying off many debts and not sure which ones should come first, this is the right place for you. We’re going to talk about ‘priority debts’ and the new 2023 rules.

We understand it can be stressful when thinking about how to manage your debts. So, we’re here to explain things in a way that makes sense and helps you feel more at ease.

Over 170,000 people visit us each month to get advice on matters like this. They find our guidance useful, and we’re sure you will too.

In this article, you’ll learn about:

What a priority debt is.

How to tell if a debt is a priority or not.

The types of debts that are often top priority.

Ways to manage your priority debts.

Questions you might have about priority debts.

We’ve offered guidance to many people in the past, so we know what it feels like to be unsure about debts. But don’t worry; we’re here to help you through it.

Let’s dive in and learn more about priority debts and how to handle them.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

What is considered a priority debt?

To put it simply, your priority debts are debts that can cause very serious problems for you if you don’t pay them back or don’t pay them back in a timely manner.

As opposed to non-priority debts, which hold lesser significance and pose a smaller problem for you when you’re not paying them, priority debts can post significant harm to the quality of your lifestyle if you avoid paying them or don’t spend the most resources on them.

You need to learn which debts are priority debts and which debts you don’t have to invest as much time and focus on.

This is not to say that you should completely ignore non-priority debts in favour of priority debts.

But this does mean that you should be more concerned with dealing with your priority debts and can move on to your non-priority debts once they are handled.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

In this section, I’ll be giving you debt advice that helps you identify what debts of yours count as priority debts and what debts you can choose to focus a bit less on.

Let’s get right into it.

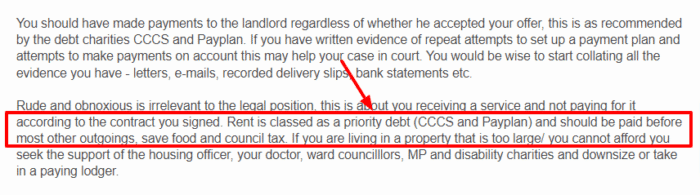

1. Rent payments

Your rent payments are absolutely a priority debt that you need to place a lot of importance on.

The reason why is pretty simple. If you don’t pay your rent, your landlord has the right to evict you from where you’re living, and that can be a huge problem and inconvenience.

Your rent arrears should be a high priority for you to pay back. Your landlord can take legal action to have you evicted if you don’t leave the house/apartment upon their request.

Your mortgage arrears (or other secured debts) are definitely priority loans. The reason why, is because if you don’t focus on paying back a secured debt, such as a mortgage loan, you may run the risk of losing very valuable assets of yours.

You should definitely prioritise mortgage loans as a high-priority debt. Remember a valuable piece of debt advice: if your debt is secured against some form of collateral, it automatically holds a good amount of priority.

3. Council Tax payments

Council tax payments come with severe consequences if you don’t pay them.

Here’s what can happen; your local council can take you to court, and if it is found that you have enough money to pay the tax but you’re deliberately not doing so, you could get jail time.

Your utility bills, such as your gas bills, electricity bills, and internet bills also count as priority debt. There are definitely consequences of not paying these priority debts too.

For one, your supplier will cut off your gas and electricity if you don’t pay your bills. Obviously, that will have a significant detrimental impact on your standard of living.

Make sure you pay these bills on time, since they’re easy to lose track of.

5. Court fines and payments

Just as with council tax, if you get a court fine and choose to not pay it even though you have the money to, you can be sent to prison.

You get court fines when you break a law, such as speeding. These fines count as important loans, since your freedom and rights are at risk in the event where you fail to pay them.

6. Income tax (unpaid) or VAT, overpaid tax credits, and unpaid child maintenance

All of these loans in question are important debts. The HMRC will inform you if you are liable to pay these loans.

If you don’t pay them yourself, the money can be taken from your account or from any benefits that you are entitled to.

If you don’t pay them back even when you can, you can face court action.

Which loans are not priority loans?

Equally as important to the discussion as priority loans are non-priority loans. You should certainly be aware of the types of loans that you can afford to spend a little less time on.

Here’s a list of debts that count as non-priority debts:

Credit-based loans (these include credit card debts) or card balance storage.

Payday loans.

Unsecured loans (this includes a wide variety of loans that are not associated with collateral, such as unsecured bank loans).

Unpaid utility bills, such as your water bill.

Unpaid parking tickets.

Informal loans, such as the money you owe to a relative.

This list can be expanded to include more types of loans, but these are the most common non-priority loans.

You don’t have to worry as much about these as you do about your priority creditors. Make sure you deal with your priority creditors in a focused manner.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

No, you should not be doing that. You should be spending a good amount of time on these loans as well, but they won’t harm you as much as priority loans in the event where you’re unable to pay them.

Can I go to jail for not paying my loans?

It is a very real possibility. If your creditors can prove that you possess the resources to pay them back but aren’t doing so, you can face court action, and eventually, jail time.

How can I know if a particular debt is a priority loan?

Assess if the loan can significantly harm the quality of your life if you don’t pay it back. If so, it is probably a priority loan.

What happens if I don’t pay my mortgage or rent?

You can lose ownership of your house, or you can be kicked out of the home where you’re living on rent. Citizens Advice has some good content that can help you in this regard.

Can my creditors take legal action against me?

Yes.

Your creditors can take legal action against you if you are deliberately not paying them back even when you can afford to.

That legal action may just have you sent to prison, so be very careful.

But again, it is always best to get support from an independent debt charity. Get in touch with:

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.