Studio Debt Collection – Should You Really Have To Pay?

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Welcome to our guide on ‘Studio Debt Collection Should You Really Have To Pay?’ If you’ve had a surprise letter from a debt collector, you may be feeling lost and worried. You might be wondering where this debt came from or if it’s right.

It can be especially tough if you’re not sure you can pay. But don’t worry; you’re not alone. Every month, over 170,000 people come to our website for advice on how to deal with debt.

In this guide, we’ll help you by:

- Explaining who Studio is and why you might owe them money.

- Showing you what happens if you can’t pay.

- Teaching you how to deal with Studio debt collection.

- Discussing ways to manage or even write off some debt.

- Giving you tips on how to keep up with your debts in the future.

Research shows that 64% of UK adults find interactions with current debt collectors stressful1. So, we know how it feels.

We’ve had team members in your shoes, dealing with debt collectors. With our experience, we’ll help you figure things out.

What happens if you can’t pay Studio?

The average unsecured debt amount has increased by 27% year-on-year (to £16,174)2. So, it’s common for people to struggle with debt.

If that’s your case and you can’t afford to pay Studio, don’t worry. Studio has a page dedicated to payment problems. The first thing they advise you to do is to get in touch with them if you’re struggling.

In such circumstances, they may need to assess your financial situation to come up with a repayment plan that can help.

However, if you simply ignore the situation and fail to make payments or reach out to them, it’s likely that they’ll pass your case over to their debt collection department. This escalates the matter and can make your life difficult.

Typical Debt Collection Process

The actions involved in the debt collector timeline may escalate if you ignore Studio Debt Collection. To prevent this from happening, it’s crucial to understand the key stages of this process. That’s why we’ve prepared this table.

| Stage | Actions | What you should do: |

|---|---|---|

| Missing one or two small payments | Calls and letters from the debt collector asking for payment. They may enquire about reasons for missing payments. | Contact the debt collector and offer to pay what you can. If you are struggling to pay the debt, get in touch with us to explore your options. |

| Missing large or multiple payments | Their contact will become more frequent, urgent, and threatening. | Contact the debt collection agency and offer to pay what you can. You may also make a complaint if you think the letters are a form of harassment. |

| Debt collector visit | After a few months, if the debt is significant (£200+) you will receive notice of a debt collector visit. They have to notify you before arriving. Debt collectors cannot take anything from your home – they may only ask for payment. | If a debt collector shows up at your home, ask them to show proof of the debt and their ID through a window. Do not open your door or let them in. You can arrange a payment plan with the debt collector, but make sure to get a receipt of this. |

| Court | If you still do not pay your debts to the original lender/debt collector agency, they will take you to court and either attempt to: – File a CCJ against you. – File an attachment of earnings order. – File a lawsuit against you. |

You must show up to your court date. From here, you can either dispute the debt, or the judge will likely suggest a manageable repayment plan for you. |

How to deal with Studio debt collection

Studio is a company that was recently in the news, thanks to a sudden increase in interest rates. This left many people getting a letter from Studio debt collection, the department responsible for getting people to pay what they owe.

If you’ve received a call, letter or email from Studio debt collection, it’s probably because you’ve an unpaid amount on your Studio account. It can be daunting trying to deal with this situation, but there are several steps you can take:

Follow our ‘prove it’ guide with letter templates and get them to prove that you owe the money.

Don’t ignore them

We always recommend responding to debt collectors – even just to question the debt’s validity. Remember, you have the right to request proof of the debt. They have to prove it or they can’t charge you.

Ignoring debt collection letters will often make the situation worse, as they can continue to escalate the matter. You could end up facing a County Court Judgement or a visit from a bailiff.

Neither is desirable, and both can have serious implications for your finances. Take this example.

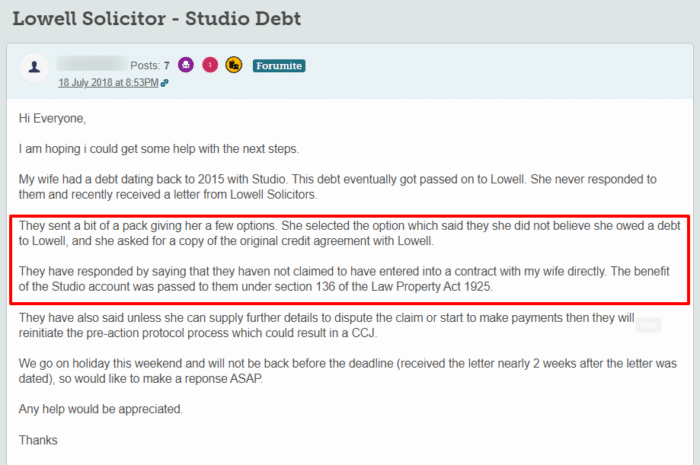

Even if your debt is passed to a different debt collection agency or your creditor employs someone else to chase your debts, you owe the debt. In this case, Studio employed Lowell to chase the missed debt.

We have a guide for Lowell Solicitors so you can make sure that you know how to deal with them.

If this person had not ignored the debt collection letters, they wouldn’t be stressing about it before their holiday!

Check the debt

Before you reach out to Studio debt collection, you should check the debt. In some rare cases, you might have been contacted in error. If this is the case, you can simply let them know they have the wrong person.

As well as checking whether the debt is actually yours, you should also check whether it is statute-barred.

If it has been 6 years – or 5 years in Scotland – since you last paid towards your unsecured debts and you have not written to your creditor about your debt during this time, it is statute-barred.

This means that the debt is not enforceable. It still technically exists, and you still technically owe the money, but there is no legal way for you to be forced to pay or for the debt to be enforced.

Keep in mind that not all debts become statute-barred!Any HMRC debts, for example, will stay enforceable for decades. Any debt that had a County Court Judgement (CCJ) attached to it during the 5 or 6-year window it will be enforceable for the duration of the CCJ.

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Know your rights

It’s important to know what rights you have when you’re dealing with a debt collection agency like Studio. There are several things that they cannot do when they’re trying to reclaim money, including:

- Threaten or harass you, either verbally or physically

- Enter your home without your permission or seize your property

- Speak with anyone else about your debt without your permission

- Pretend that they have legal powers that they don’t actually have

Here’s a table that will help you better understand what debt collectors can and can’t do. If you’d like to learn more about your rights, make sure to check out our detailed guide.

| Debt Collectors Can | But They Can’t |

|---|---|

| Contact you by phone or mail. | Call you after 9pm or before 8am. |

| Conduct home visits (on rare occasions) and knock on your door. | Forbily enter your home, or stay if you ask them to leave. |

| Threaten to take you to court by suing you for payment on a debt. | Harrass you, including threats of violence, repeated calls and visits, or abusive language. |

| Negotiate a debt settlement. Tip: make sure to get this new arrangement in writing. | Visit your workplace. |

| Access your bank account, but only after a court judgment has been made. | Take anything from your home or threaten to do so. |

| Sell your debt. | Speak to other people about your debt without your permission. |

| Contact you frequently. | Keep doing so if you request that they reduce communications. |

Reach out to them

Once you know what your rights are and the exact situation of your debt, you can try reaching out to Studio debt collection. Discussing the matter may mean that the debt collectors stop chasing you, and can give you the chance to work out a means of repaying the money.

Make a payment

Whether you agree to a monthly repayment plan or pay off your entire debt at once, it can soon resolve the matter if you make a payment to Studio. Of course, you should only do so if you’re sure that you owe what they’re claiming you do.

Get help

If you’re struggling to make even a small monthly repayment to Studio, there are several resources you can draw on for help and support.

There are several charities and organisations in the UK that offer free debt counselling services and free financial advice. Their advisors will be able to walk you through your options and find the best solution for you.

» TAKE ACTION NOW: Fill out the short debt form

What If I Can’t Afford to Pay Studio?

If you can’t afford to pay Studio, you may be able to afford one of their repayment plans. They have to offer you different payment options so you may be able to negotiate a payment schedule that suits you.

But if you can’t afford any of their payment offers, you may be able to benefit from a debt solution.

There are several debt solutions options in the UK, so we recommend speaking to a debt charity for free advice. Their advisors will be able to take a detailed look at your finances and find the best solution for you.

Debt Management Plan (DMP)

A DMP is an informal debt solution that lets you pay off your debts via a single monthly payment.

Because it is informal, it is not legally binding so you are not tied into a DMP for a minimum number of payments.

Individual Voluntary Arrangement (IVA)

An IVA is a formal agreement between you and your creditors. You agree to pay a monthly sum that is distributed amongst your debts, and your creditors agree not to contact you during your IVA.

IVAs typically last for 5 or 6 years, and any outstanding debt is wiped off when it ends.

Keep in mind that IVAs are not suitable for everyone. You need to owe several thousand pounds to more than one creditor to be eligible. You also need to demonstrate that you have some disposable income every month.

Trust Deed

IVAs are not available in Scotland. Instead, you will need to opt for a Trust Deed.

Trust Deeds work in the same way as an IVA – you pay an agreed sum each month that is shared amongst your creditors, they can’t contact you, and any leftover debt at the end of your Trust Deed term is written off.

Debt Relief Order (DRO)

A DRO is a good option for those facing financial hardship with no assets and little income.

For 12 months, you make no payments, but your creditors freeze your interest and don’t contact you.

If your finances haven’t improved during this year, you may be able to write off your unsecured debts.

Bankruptcy

If you have debts but no realistic possibility of ever paying them off, you may need to declare bankruptcy.

Bankruptcy has an unfair stigma attached to it as it may be your only way of getting a financial fresh start. That said, it is a serious financial situation that should not be taken lightly.

Sequestration

Sequestration is the Scottish version of bankruptcy.

If you have little income and no valuable assets, you may be able to apply for a minimal asset process bankruptcy (MAP). A MAP is a quicker, cheaper, and more straightforward version of sequestration, so worth considering.

Do I Still Pay Studio If They Are In Adminstration?

You should carry on making your agreed payments if Studio has gone into administration – carry on as normally as possible!

In these types of situations, the administration process will have no effect on the repayment terms of your contract. The debt collection processes will also not change if Studio goes into administration. So if you decide to stop paying because you’ve heard that Studio are in administration, your account could be sent to debt collectors and chased as normal.

This is because administration is just one stage of the corporate insolvency procedure – your creditor is by no means bankrupt if they enter administration. Most companies exit administration and begin trading as normal. In these instances, administration can be used to reshuffle the company’s finances and will have no effect on your account.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

What if I Don’t Pay Studio Debt Collection?

If you continue to refuse to pay Studio for a debt that you actually owe, the situation can escalate quite quickly. Studio can try taking you to court with a County Court Judgement.

If it rules in their favour, you’ll be legally demanded to pay what you owe, plus any court fees and interest. If you don’t have the funds, the court may appoint a bailiff to come and take your belongings to cover the cost of the debt. You want to make sure you act before it comes to this.

If you are facing potential court action, you can contact a debt charity for free legal advice. We have linked some at the bottom of this page.

Will Studio Debt Collection Affect My Credit Score?

Understanding credit scores is important if you want to get back in control of your finances. Generally, the better your score, the better your financial health, and the better credit you are eligible for.

But yes, Studio may affect your credit score. However, this will only happen if you don’t make any payments as part of a repayment schedule that you have negotiated.

If you let your missed payments build up until Studio have to get a CCJ against you, your credit score will be very badly affected.

Unless you pay within one month of the CCJ being issued, it will be recorded in the Register of Judgements, Orders and Fines for 6 years. If you pay off your debt within these 6 years, you can request that your judgement is marked as ‘satisfied’ on the register.

To do this, write to the court with proof that you have paid off the debt in full.

If you manage to pay within one month of the CCJ being issued, the judgement will not be recorded in the register. You will need to write to the court explaining that you have paid and provide proof.

CCJs are also visible on your credit file for 6 years. This will make it almost impossible for you to get credit during this time.

This is because companies use your credit file to see if you are a ‘high-risk’ customer – someone who might have difficulty paying their bills on time. If you have a CCJ, you have had such trouble paying back your debt that someone had to go to court about it.

Understandably, companies are going to be reluctant to give you credit!

After 6 years, it is no longer visible on your credit report and you should find it easier to get credit again.

How Do I Make A Complaint About Studio Debt?

If you think that Studio has been unreasonable or behaved inappropriately, you can make a complaint. You can also make a complaint if you feel that they have broken any of the Financial Conduct Authority’s (FCA) guidelines.

Make your first complaint to Studio so that they have the chance to sort out the issue themselves. If you feel that they have not taken your complaint seriously enough or have not addressed your issue properly, you can escalate matters.

You can make any secondary complaint to the Financial Ombudsman Service (FOS). They will investigate and, if your complaint is upheld, Studio may be fined. You could even be owed compensation.

Studio Debt Collection Contact Details

| Registered Company Address: | Church Bridge House, Henry Street, Accrington, United Kingdom, BB5 4EE |

| Registered Company Number: | 718151 |

| Parent Company: | Express Gifts Ltd |

| Consumer Credit Licence: | 348351 |

| Phone: | 03713 765680 |