Find out how much equity you could release by answering below.

In partnership with Age Partnership.

Our preferred equity release adviser is Age Partnership. For free and impartial money advice you can visit MoneyHelper.

Featured in...

Our preferred equity release adviser is Age Partnership. For free and impartial money advice you can visit MoneyHelper.

If you’re thinking about equity release, you’ve come to the right place. This article will tell you all about the best home reversion plan providers in the UK.

Over 7,000 people visit our website each month seeking advice about equity release, so you’re in good company.

In this article, we’ll discuss:

How equity release works and what it involves

The benefits and drawbacks of home reversion plans

The top home reversion companies, such as Hodge Lifetime and Crown Equity Release

Other ways you can use your home to help your finances

Things to think about before you decide on a home reversion plan

So, let’s get started. It’s time to learn more about home reversion plans and how they could help you.

Find out how much equity you could release by answering below.

Find out how much equity you could release by answering below.

In partnership with Age Partnership.

What are the different types of equity release?

There are two types of equity release loans to choose from, but both of them can be accessed as a lump sum or regular drawdown loan.

The most used equity release scheme is a lifetime mortgage, which charges interest on the loan amount but does not demand interest repayments either. The interest gets added to the total amount owed each month to create a bigger debt over time, which eventually gets repaid using the sale proceeds. There are a number of variations on the standard lifetime mortgage.

The second type of equity release scheme is a home reversion plan, which is the focus of this MoneyNerd guide. Read on to learn how a home reversion plan works and what home reversion companies are around in the UK today.

Do you receive a tax-free lump sum?

When you use an equity release, you receive tax-free cash. This can be a cash lump sum to the value of the loan, or it can be a drawdown facility. A drawdown loan provides an initial cash lump sum and leaves the rest of the money in a cash reserve with the lender, which can be accessed when the homeowner chooses.

Taking a drawdown loan over a lump sum loan could offer several benefits, including the avoidance of unnecessary interest (lifetime mortgage only) or maintaining eligibility to receive means-tested benefits. It could be preferred just to help with retirement budgeting as well.

What is the catch?

Using equity release to retire early or improve the quality of life within your retirement can sound like a fantastic idea. Without having to make monthly repayments, the chance that you will only repay after death can make equity release tempting.

However, equity release is not an easy decision because the cost of repaying the loan is much greater than the initial loan amount. No matter what type of equity release loan you use, most people should expect to pay back more than double the original loan amount when the time comes. This could significantly reduce your wealth while living in a care home, or it would substantially reduce the value of your estate, which your beneficiaries would inherit.

A home reversion mortgage is another name for a home reversion plan. You may also hear them referred to as a home reversion scheme or just reversion schemes. They all work as described above, although lenders may insert their own terms and clauses into credit agreements. Always read the fine print of any home reversion plan agreement.

How equity release could help

More than 2 million people have used Age Partnership to release equity since 2004.

How your money is up to you, but here’s what their customers do…

Find out how much equity you could release by clicking the button below.

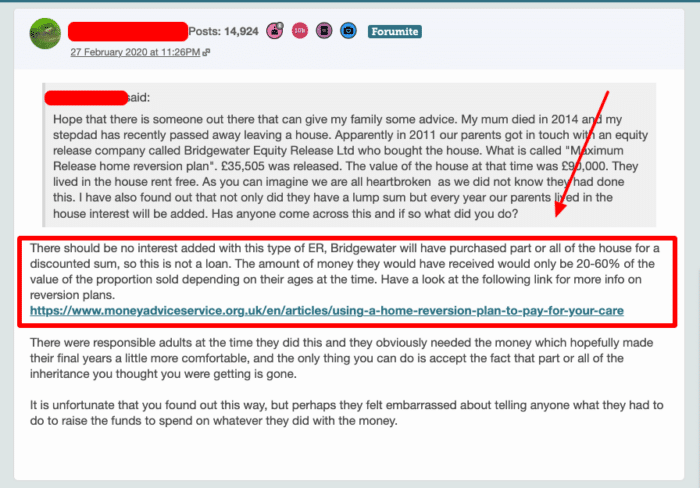

Home reversion plans provide the homeowner with a loan, usually between 20% to 60% of the value of their home, as long as they have no debts secured against the property. If they do have outstanding debts, then they probably will not be able to apply.

This loan is not charged with any interest. The loan is cleared when the homeowner dies or moves into care, at which point the property will be sold, and the lender will take a percentage of the property’s sale proceeds.

The amount the lender takes to clear the debt is agreed right at the start of the loan, which could be years or even decades previous. The percentage that is taken from the property sale will be much greater than the percentage of equity released. For example, an equity loan worth 20% of the equity may cost the homeowner 60% of the eventual property value in the future. You might want to think of it as selling a share of your home in the future.

Because property values tend to increase over time, this means the homeowner will end up paying back more than x3 the initial loan amount to clear the debt. It may be possible to repay the debt with cash from the estate and keep the family home. However, if the estate beneficiaries have to pay money into the estate to do so, their stamp duty could be applied.

The pros and cons

The primary advantages of using a home reversion plan are:

Spend the loan on whatever you need to or keep it saved

There are no loan repayments to make

Keep living in your home with no rent to pay

The main disadvantage of using a home reversion scheme is that you must give the lender a large part of your home sale proceeds in the future, which makes them very expensive to repay. The knock-on effect is that your estate beneficiaries will inherit less wealth when you die, and they won’t likely inherit the family home, which then reduces the inheritance tax threshold.

There are a number of other drawbacks, including:

High early repayment charges to get out of the loan

High set -p costs

Could stop your eligibility to receive some benefit payments

Is it a good idea?

A home reversion plan might be a good idea for you, but it will depend on your personal circumstances and any alternative options available. The way to make an informed decision is to get financial advice first.

Do not just use any financial adviser, but opt for advisers who work frequently in equity release. You may want to give preference to finance advice companies that are members of the Equity Release Council.

A home reversion plan can help many people with their money problems, but it has a lot of legal complexities that need to be carefully negotiated to protect the homeowner’s best interests. To make sure the transaction is legal, clear, and fair, it is important to hire a solicitor who knows about equity release and what it means.

Exploring Alternative Financial Routes

Before opting for a home reversion plan, it’s crucial to explore various alternative financial paths that might align better with your financial strategy, personal circumstances, and long-term objectives. Here’s a breakdown of some alternative routes to consider:

1. Downsizing:

This involves selling your current property and moving to a smaller, less expensive one to free up cash.

Pros: Potential to release a substantial lump sum and lower living costs.

Cons: Emotional and practical implications of leaving a family home, moving costs, and possible impact on inheritance.

2. Renting Out Part of Your Property:

This involves creating an income stream by renting out a room or a section of your home.

Pros: Ongoing additional income without having to move and eligibility for the Rent a Room Scheme tax benefits.

Cons: Loss of privacy, the potential for disruptive tenants, and the possible need for landlord insurance.

3. Lifetime Mortgage:

This is a type of equity release where you take a loan against your home’s value, and the loan plus interest is repaid when the property is sold after your death or moving into long-term care.

Pros: Retain ownership of your home, potentially benefit from future house price rises, and no mandatory monthly repayments.

Cons: The debt can grow quickly due to compound interest and may significantly reduce the inheritance.

4. Drawing on Savings or Investments:

This involves using your savings or liquidating investments to fund your retirement or specific needs.

Pros: No need to encumber your property or accrue debt.

Cons: Reduces your financial buffer and might expose you to higher risks depending on your investment portfolio.

Homeowners should only consider home reversion plans that are offered by legitimate lenders and loan providers in the UK. This means ensuring that the company is authorised and regulated by the Financial Conduct Authority, which you can verify on the Financial Services Register.

The Equity Release Council is another body that aims to improve standards of lending within the industry and to provide homeowners with additional protection when taking out home reversion plans or a lifetime mortgage.

Lenders are not forced to become a member of the Equity Release Council but many do. When they joint they agree to follow a number of rules which benefit the senior homeowners, such as the infamous negative equity guarantee that stops lenders from chasing debts not completely repaid via the property sale. However, this particular rule only benefits people who have a lifetime mortgage loan.

Join thousands of others who release equity

Age Partnership have helped over 2 million people release equity from their home.

Mrs Wareham

“I am more than pleased to have taken out Equity Release with Age Partnership.”

Reviews shown are for Age Partnership. Search powered by Age Partnership.

Who are the providers (UK)?

At the start of our guide, we mentioned that home reversion plans are more difficult to find than lifetime mortgages. This is simply because more people choose to use a lifetime mortgage. Nevertheless, there are a couple of notable lenders offering home reversion plans, such as:

Hodge Lifetime

Crown Equity Release

Newlife

Bridgewater Equity Release

I always advise you to complete your own research so you don’t miss out on changes in the industry and new deals. But remember to only consider those that are regulated by the Financial Conduct Authority.

Start by looking at an equity release calculator

When you do find a home reversion provider you want to consider, check to see if they have an equity release calculator on their website. This will help you understand how much you could borrow and how much the loan will cost to repay using this specific reversion company. An equity release calculator is not entirely accurate, so take the information given with a pinch of salt.

For more information on lifetime mortgages, reversion schemes and anything else to do with equity release, you’re already in the right place with MoneyNerd!

Things to consider

Equity release will involve a home reversion or a lifetime mortgage, which is secured against your property and will reduce the value of your estate and impact funding long-term care. Our equity release partner, Age Partnership provides a personalised illustration to explain the full details. The money you release, plus the accrued interest is then repaid when you die or move into long-term care. Advice is required before proceeding with equity release and any existing mortgage must be repaid. Age Partnership provide initial advice for free and without obligation. Only if your case completes would Age Partnership’s advice fee of £1,895 be payable. Other lender and solicitor fees may apply.

Find out how much equity you could release by answering below.

Find out how much equity you could release by answering below.

In partnership with Age Partnership.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!