Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Deciding whether to cancel your IVA can be a tough choice. If this is your concern, you are in the right place. Every month, more than 170,000 people visit our website for help with debt solutions.

In this article, we’ll help you understand:

The process of IVA and how to cancel it

The reasons one might want to cancel an IVA

What happens if your creditors and IP do not accept your cancellation

The consequences of failing an IVA

Common questions about IVA

StepChange stress the need for professional debt advice, noting that 60% of adults in financial trouble hesitate to seek help.1

Our team includes people who have faced debt challenges themselves. We understand that you may be feeling confused about the IVA process or worried about how to pay off a debt.

But don’t worry; we’re here to help you understand your options.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

IVA Cancellation

You should talk to your insolvency practitioner for advice before taking this step.

Remember, if you cannot afford the minimum monthly repayments on your IVA, your insolvency practitioner may be able to reduce that amount and make your budget more flexible.

You should only cancel an IVA if your circumstances are expected to change tremendously, and you can pay your debt back soon.

Don’t just contact your practitioner one day and ask them to cancel your IVA. Take your time to go over this decision with him and consult other sources for debt advice as well before finalising your cancellation.

Termination of IVA

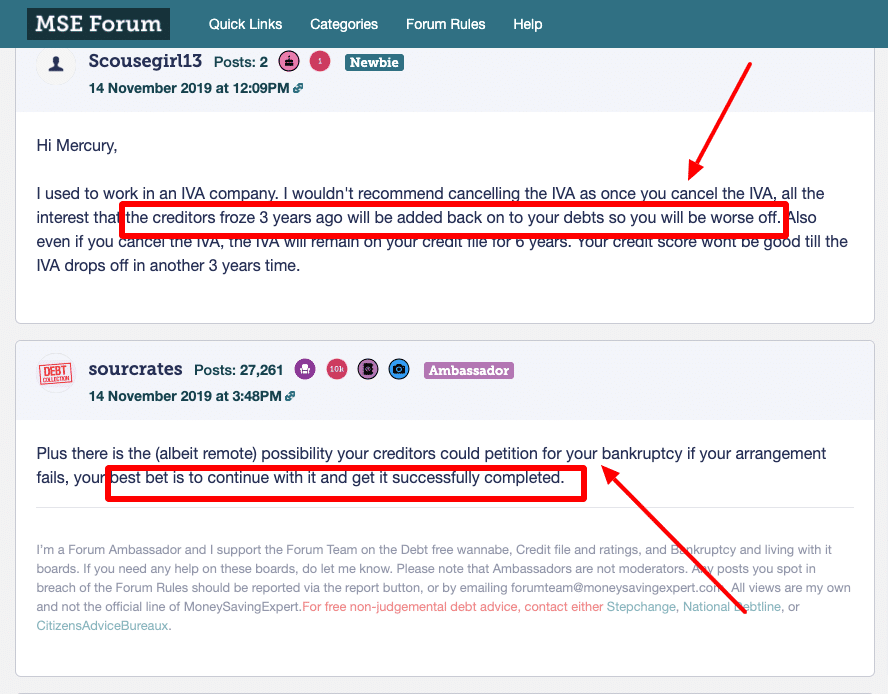

An IVA is terminated when you stop making your repayments to your lenders. IVA termination consequences usually mean that the debt you owe still stands, and you will have to pay the practitioner the fees you owe him for their services so far. Some may charge an IVA cancellation fee.

You will have to pay back your debt. In addition, the relevant interest and statutory interest also have to be paid back to your lenders. All of your debts will still show on your credit score.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

If, for example, you have a long-term mental illness and it is unlikely for you to complete the IVA duration, it is pointless to demand monthly repayments from you.

In such a case, you can talk to your insolvency practitioner and get your IVA cancelled. They can give you sound financial advice for an IVA cancellation.

In other cases, if your circumstances change and you’re expected to come up with some inheritance or extra cash soon, you can cancel your IVA and promise your lenders their repayments as soon as the windfall money comes into your hands. This is called an IVA windfall clause.

Here’s a table showing the average IVA amounts, so you can use it for reference and decide whether cancelling your IVA is the way to go.

IVA Averages

Amount

Average Household Debt

£32,049

Average Monthly Payments Pre-IVA

£587.23

Average Duration of IVA (Years)

5

Average Payments Post-IVA

£158.80

Average Savings per Month

£428.73

Data from 132 verified insolvency cases of MoneyNerd readers taking out an IVA with The Debt Advice Service in 2023

Ways to Cancel

Here are the ways you could cancel your IVA:

IP and Creditors Agreement

In this method, you talk to your practitioner and creditors and explain your reason for IVA cancellation. If they agree with your case and want you to cancel the arrangement, you can only proceed with the decision.

Remember that your lenders will only agree to the cancellation if you provide a better alternative to the IVA and promise them their money back.

Stop Making Payments

I don’t advise doing this as it can get you to court. Not notifying your practitioner before stopping repayments can become very problematic for you. Your lenders will usually come directly after you in such a case and take you to court.

Legal proceedings when you owe someone a debt can be very frustrating as the court can even order you to sell your assets to pay off your debt.

If you’re a logical human being, this question will go over many times in your head:

“Should I really cancel my IVA?”

Someone with expertise in debt advice best answers this question and who is aware of your personal circumstances regarding the repayment of the debt.

Only a person in close contact with your IVA and fully aware of your circumstances can determine whether or not it would be advisable for you to cancel your agreement entirely.

This is why it is advised to consult a licensed practitioner and explain your situation to him or her, then move forward with whatever you have in mind based on their advice.

Your practitioner is usually obligated to ensure data protection and they cannot disclose your case to anyone.

The data protection goes to the extent that they can’t even talk about your debts or IVA hardship to someone you know. The most they can ask them for is your contact information. No one except the insolvency practitioner will know of your debt problems, so there’s no harm in taking their suggestions.

While it’s a financial arrangement at its core, the effects on a person’s mental well-being can be profound, leading to stress and uncertainty. This aspect may not be often considered, but for those grappling with the decision, it’s crucial to understand the emotional repercussions involved fully.

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

What If the Creditors and IP Don’t Accept the Proposition?

If they don’t accept the proposition, you cannot continue your current agreement until the initial agreed duration. The only way to cancel an IVA is to get all the creditors on board with the cancellation.

Could you legally write off some debt?

Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.