Comprehensive Secured Debt Guide with FAQs

Representative example: If you borrow £34,000 over 15 years at a rate of 8.26% variable, you will pay 180 instalments of £370.70 per month and a total amount payable of £66,726.00. This includes the net loan, interest of £28,531.00, a broker fee of £3,400 and a lender fee of £795. The overall cost for comparison is 10.8% APRC variable. Typical 10.8% APRC variable

Representative example: If you borrow £34,000 over 15 years at a rate of 8.26% variable, you will pay 180 instalments of £370.70 per month and a total amount payable of £66,726.00. This includes the net loan, interest of £28,531.00, a broker fee of £3,400 and a lender fee of £795. The overall cost for comparison is 10.8% APRC variable. Typical 10.8% APRC variable

Are you wondering what does it mean when a debt is secured? You’ve come to the right place. Every month, our website is visited by more than 6,900 people who are seeking advice on similar matters.

In this easy-to-understand article, we’ll address the following questions:

- What does it mean when a debt is secured?

- Is it easier to get approval for secured debt?

- Does secured borrowing offer lower interest rates?

- Which assets can be used to secure a debt?

- What happens if you do not pay back a secured debt?

- What are the pros and cons of a secured debt?

- Can secured debt be written off?

- Can you get secured debt with bad credit?

I know that understanding secured debts can be a bit tricky. But don’t worry; we’re here to help you figure things out and make an informed decision.

Let’s dive in!

What does it mean when a debt is secured?

Secured loans will require the individual to use an asset as security in the agreement.

When a debt is secured, it means that the lender can repossess and sell this asset if the borrower fails to make payments as agreed in the credit agreement. The lender will not seize and sell the asset after one missed payment, but if continuous payments are missed with no communication, they will progress to take the asset used as collateral.

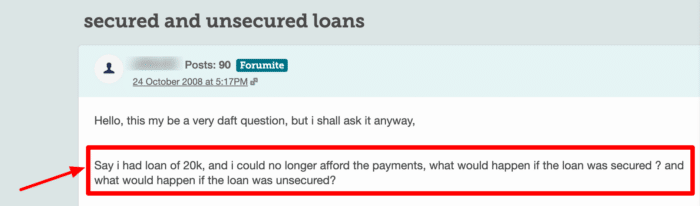

This forum user on MoneySavingExpert is unsure about the difference between secured and unsecured loans, as many people are.

What if I fail to make repayments on an unsecured loan?

You should also be aware that not paying back an unsecured debt can also lead to having valuables and assets repossessed.

The lender can take the debtor to court and ask a judge to enforce the debt using bailiffs or other means. The bailiffs, also known as enforcement officers, can come to your home and take valuables to be sold at auction to recover the money owed. The process is long-winded and more expensive compared to repossessing assets as part of a secured debt.

Is it easier to get approval for secured debt?

In comparison to unsecured personal loans and credit cards, a secured debt may be somewhat easier to get approval for. Using an asset mitigates your lending risk and makes lenders more comfortable to lend to you. However, applications for secured loans must still pass affordability tests, and your credit history will still need to be checked.

Lenders will also consider other factors, such as your employment status and income stability, as well as the loan-to-value ratio (LTV) of the asset.

What is Loan to Value (LTV)?

LTV is a measurement within a risk assessment completed by lenders before agreeing to award mortgages. The calculation is used to determine the element of risk when lending a certain amount to you. A lower LTV ratio generally means you can get a lower interest rate because it poses less risk to the lender.

Lender |

APRC |

Monthly payment |

Total amount repayable |

|---|---|---|---|

| United Trust Bank Ltd | 5.99% |

£218.73 |

£26,247.92 |

| Pepper Money | 6.86% |

£220.24 |

£26,429.17 |

| Together | 6.95% |

£220.40 |

£26,447.92 |

| Selina | 7.5% |

£221.35 |

£26,562.50 |

| Equifinance | 7.7% |

£221.70 |

£26,604.17 |

| Spring | 10.5% |

£226.56 |

£27,187.50 |

| Loan Logics | 11.2% |

£227.78 |

£27,333.33 |

| Evolution | 11.28% |

£227.92 |

£27,350.00 |

Representative example: If you borrow £34,000 over 15 years at a rate of 8.26% variable, you will pay 180 instalments of £370.70 per month and a total amount payable of £66,726.00. This includes the net loan, interest of £28,531.00, a broker fee of £3,400 and a lender fee of £795. The overall cost for comparison is 10.8% APRC variable. Typical 10.8% APRC variable.

Search powered by our partners at LoansWarehouse.

Does secured borrowing offer lower interest rates?

Secured loans usually offer lower interest compared to unsecured debt, but this is not guaranteed. The interest rate you are offered will depend on your personal finances and your credit history. Someone with an excellent credit score could get a better interest rate with unsecured credit compared to someone with bad credit using a secured loan.

Does secured borrowing allow me to take out more credit?

Secured loans also generally offer the chance to take out more credit because the asset reduces perceived lending risk and makes it easier for the lender to recover larger sums of unpaid debt. If the debt is secured with home equity, the loan may allow you to borrow against a percentage of your home equity, which might be a substantial amount.

Which assets can be used to secure a debt?

The most common assets used to secure a debt are property and vehicles.

» TAKE ACTION NOW: Compare deals from the UK’s leading lenders

You can find some secured debts that use other assets, even sometimes something like fine art, but these are less common.

When the debt is secured with an asset, that asset can still be used by the individual. For example, you can still live in your home or use your car when it is being used as collateral in a credit agreement.

Secured loans for all purposes

- Stuck paying high interest on credit card debts & loans?

- Looking to fund a home improvement project?

- Dreaming of finally taking the once-in-a-lifetime trip?

Polly

“This was by far possibly one of the nicest experiences I’ve had getting a secured loan.”

Reviews shown are for Loans Warehouse. Search powered by Loans Warehouse.

What happens if you do not pay back a secured debt?

If you do not pay back a secured loan, the lender will first write or call you and ask you to pay immediately. If you ignore this notification, they will send you a final reminder. You may even have to pay late fees at this stage.

If you continue to ignore the lender’s correspondents, they will register a default on your credit report, making it harder for you to get a credit card or loan in the future. If further defaults are recorded, the lender will initiate the process of repossessing your asset used as collateral.

What happens after my asset is repossessed?

The asset is then sold, often at an auction, and the money is then used to pay off all arrears and fees. Any remaining money will be given back to the debtor. If not enough money is raised from the sale, possibly due to the asset decreasing in value (most likely the case with property), then the debtor will still need to pay the shortfall. This might even lead to filing for bankruptcy.

The impact of secured debt on your credit score

Securing a debt can have an impact on your credit score, both positively and negatively. If you keep up with repayments, then your credit score could improve. However, missed payments and repossession can significantly impact it negatively.

Should I take out secured debt?

Taking out a secured debt may be a good idea, especially if you’re looking for a larger loan amount than what is offered through unsecured debt or if you just want to find a lower rate of interest.

However, you should fully understand the risks involved when taking out a secured loan. There may be other credit options available. Each person is different, and the decision should come down to personal aims and circumstances. To seek clarity on your own situation, you could speak with a loan broker or financial advisor.

It’s also really important that you understand all of the legal terms and conditions in the credit agreement before taking out a secured loan to prevent you from signing a contract with unfavourable terms unknowingly.

The pros of secured debt

- Access to larger loans – secured debt typically enables borrowers to access a larger loan amount, which can be useful for purposes such as home renovations.

- Competitive interest rates – by using an asset as collateral, secured loan providers can usually offer competitive rates.

- Variation and accessibility – there is a wide variety of secured loans, and these are advertised widely in the UK.

The cons of secured debt

- Asset at risk – the asset you use to secure the debt is at risk of repossession. Even if you think the loan is affordable now, situations can change, and it may become unaffordable.

- Appraisal fees – the asset you want to use as collateral may need to be valued to determine how big of a loan you can get (e.g. home equity loan). This could come at a cost you need to front.

- Additional costs – there could be further costs associated with a secured debt, such as admin fees and closing costs.

Can secured debt be written off?

Secured debt can only be written off if the lender agrees to it, which is highly unlikely given they can easily recover the debt by seizing and selling your listed asset.

Instead of asking them to write off the debt, you should try to negotiate a new repayment structure that is more affordable. By agreeing to pay less for longer, your payments could be lower, but you can pay back for longer. Lenders are willing to negotiate to avoid having to repossess your asset.

Alternatively, you may want to consider suitable debt solutions.

Can you get secured debt with bad credit?

It may still be possible to take out a secured debt with a bad credit rating. By using an asset as collateral and reducing perceived lending risk, lenders that may have rejected you for unsecured credit may be more willing to lend to you through secured debt. However, this is not guaranteed, and you may have to pay a higher rate of interest.

In my experience, some lenders do specifically advertise secured loans to individuals with an unsatisfactory credit score.