Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Worried about your debt and wondering if it’s normal? Let’s find out. This article aims to give you answers.

Here’s what we’ll cover:

The current average personal debt in the UK

What causes the most debt

How debt differs by age, region, and gender

Feeling unsure about your debt can be hard. But don’t worry; you’re not alone. Every month, over 170,000 people visit our website for advice on debt matters.

We’ll use clear facts and figures to help you understand debt in the UK. Let’s get started!

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

UK Personal Debt Statistics

Here’s a snapshot of average debt in the UK:

At the end of February, the UK population owed £1.698.4 billion, an increase of £15.1 billion or £286 per adult.

The average adult owes £33.410 in total debt.

In March 2021, the Office for Budget Responsibility predicted that the total UK household debt would climb from £2,006 billion in 2020 to £2.354 billion in 2025, resulting in an average total debt of £82,641 per household in the United Kingdom.

Water, electricity, and gas cost the average UK household £4.20 each day.

During the first quarter of 2021, 290 people were declared insolvent or bankrupt in England and Wales.

Between December 2020 and February 2021, 2,267 employees were laid off every day.

In the months of October to December 2020, a property was repossessed every 15 hours and 46 minutes.

There were an additional 18 UK mortgages in arrears every day that was more than 2.5% late.

850 people were out of work in the UK every day in the last year.

There is an average cost per day of £23.25 for couples and £28.22 per day for a single parent to raise a child from birth to the age of 18.

According to the same source, personal debt has increased by £498 per adult since the fourth quarter of 2019.

This works out at more than £26 billion more debt across the UK in just 12 months. Thus, UK debt trends have been on the rise since the pandemic struck.

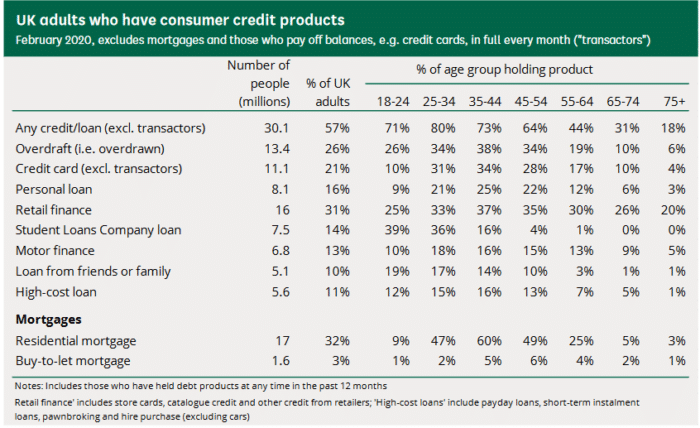

Debt by Age Group

The table below displays the percentage of adults in the UK, broken down by age group, who have or have had various types of consumer credit products in the last 12 months (2017 data).

Overall, people aged 25-44 are the most likely to have consumer credit, with 71% of those aged 25-34 doing so, compared to only 20% of those aged 65 and up.

Debt levels are highest among homes with a head of household aged 18 to 34 years old, with an average non-mortgage household debt of £10,400. In general, the older a person gets, the less debt he or she owes.

If age is something that needs to be taken into account when it comes to looking at the average personal debt in the UK, then we must also look at the region, too.

Salaries, house prices, and the general cost of living differ from region to region around the UK, so, therefore, levels of debt will differ because of affordability.

We found these useful tables from the House of Commons Library (put together by the FCA) that show the difference between the average debt by region for those with a mortgage, a student loan, and those without.

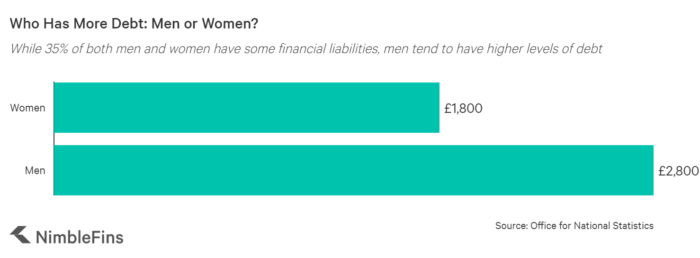

While men are much more likely to have debt than women, women are perceived to be less confident and informed about financial services than men and therefore are more unlikely to be carrying debt.

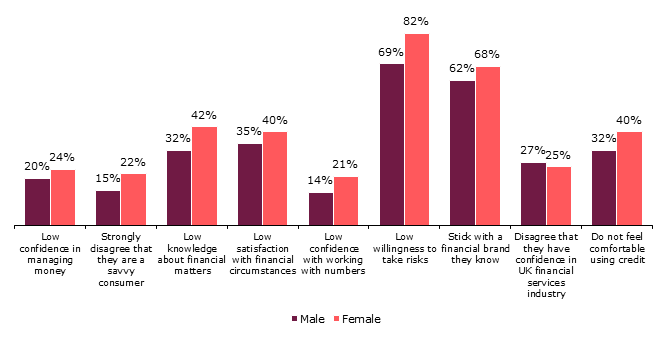

The Financial Lives survey from the FCA invites people to rate themselves on a variety of confidence and risk factors.

The graph below depicts the percentage of persons who rate themselves as low (0-6 on a scale of 0-10) or who agree or disagree with various claims.

Source: FCA, Financial Lives Survey 2020

The results demonstrate that men and women had similar levels of dissatisfaction with their own financial circumstances.

However, there are some notable differences in their levels of risk aversion and confidence in financial affairs, including:

Men are more at ease when it comes to interacting with financial services than women.

Women are more likely than males to report they lack confidence in their ability to manage money or understand financial issues.

Women seem to be more risk conservative in their financial management.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

There are so many different stories about why people landed in debt. The most common is to do with losses of income and unexpected expenses.

Sometimes it is the result of simply overspending and a lack of financial literacy.

Nearly 50% of all reasons for falling into debt in the UKwere unemployment or redundancy, reduced income or benefits, lack of control over finances, and missed payments.

Not only that, but England and Wales declared 313 bankrupt or insolvent individuals every day between August and October of 2021. That’s one every 4 minutes 37 seconds.

Of course, a lot of the unemployment and redundancies can be put down to the pandemic, and many people who were still employed were put on furlough to help subsidize income, and we witnessed the UK economy falling into hardship.

Because of this, there was a significant amount of government debt accrued from millions of people nationwide being put on furlough. Borrowing from credit lenders became inevitable as families tried to keep up with monthly repayments on necessities.

But, many people in England and Wales found themselves paying out way more than they could afford.

However, these other causes are still valid reasons for going into debt.

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.