Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you worried about your debts because of mental health issues like ADHD? You have come to the right place.

Each month, over 170,000 people visit our website seeking advice on debt problems, so you are not alone.

In this article, we’ll help you understand:

How debt can affect your mental health

Why there is a link between ADHD and debt

How to ask for your debt to be written off due to mental illness

What to do after your loan is written off

Where to find more help

We know that dealing with debts can be hard, especially when you are not feeling well – many of us have faced the same worries.

But we’re here to help you understand your options and learn more about how you can manage your debts when you are dealing with mental health illnesses. Let’s dive in.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Can you Ask for Debt to be Written off due to Mental Illness?

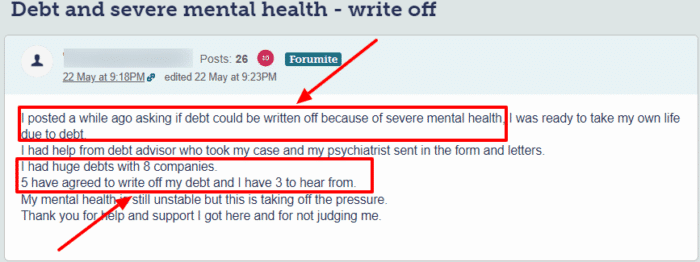

In general, yes, it is possible to get your debt written off because of mental illness – but there are a few conditions you should be aware of and a few protocols you need to follow.

Let’s look at each of such cases in detail individually.

Convincing Creditors to Write Off Debt

If you think your mental illness is making it very difficult for you to deal with your debts, you may choose to contact your creditors and ask them to write off your debts.

Under the Financial Conduct Authority (FCA) guidelines, lenders are required to treat people with mental illness fairly. Creditors should also consider writing off a debt if you’re unable to pay because of your illness.

Whether you want to inform your creditors of your issues is entirely your choice, but if you do, it may end up helping you with your negotiations.

Your creditor may understand your situation and offer you various options to help you deal with your situation. Writing off the entire debt, especially if it’s a big sum, is unlikely but not impossible. Especially if the debt is statute-barred, as those can’t be reinstated in the future.

However, instead of entirely writing off your debts, creditors may choose to back off for a certain period. They may also agree to:

Not employ debt collectors.

Contact you only at specific times.

Give you extra time to deal with your situation.

Bring in specialists to help you handle the situation.

Notice of Correction

If you’re struggling with your mental health illnesses, it may be a good idea to mention it in your credit report to inform potential lenders and creditors about the circumstances surrounding your debts.

A notice of correction is a passage that explains the reasons behind your credit rating.

It also conveys any contextual information that you may want to include in your credit report.

So, for instance, if your poor credit rating has primarily been caused by your mental health illness, you might want to explain it on your credit report.

That way, even if you have a bad credit score, creditors may understand your mental health as being the reason behind your poor score and may offerfinancial alternatives and other arrangements to make debt easier for you.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

A Debt and Mental Health Evidence Form, or DMHEF form, allows your creditor to receive information and updates about your mental illness from a health professional. This is done with your consent.

We suggest you use this form if you want to let your creditors in on your situation. It also lets your creditors take into account your mental health situation and make appropriate adjustments to their debt collection process.

Be sure to ask your creditors to write off your debt if you feel your mental health condition is causing you not to pay. You should do this in writing and send some medical evidence of your condition. Some creditors may be willing to forgive your debt if you’re mentally ill.

When you’re missing payments, the idea of unpayable debt looming over your head can be overwhelming.

Mental health and financial stress are interlinked. Several people suffering from mental health issues have reported that their condition worsened as a result of being in debt.

Owing people money can make a person feel worthless and inadequate, which is a big blow to one’s self-esteem.

Besides, several people face constant anxiety, depression, and fear because they’re drowning in debt.

The relationship between mental health and debt has been so commonly observed that a proper medical term, “debt stress”, has been coined to represent the debilitating mental impacts of debt.

Lastly, being unable to clear your debts may add to your health problems, causing a loss of focus, hypertension, irritability, attention problems, and a host of other mental problems.

The Link Between Debt and Depression

Debt and depression are often linked. You may feel depressed as a consequence of being in debt. You might be struggling to manage your debt because of existing depression.

Either way, debt depression can make life very difficult. The impact of depression on financial decisions is real.

However, it is important to know that you’re not alone in this, and there is always support available to you. If you are struggling with debt depression, there are many reputable charities and resources available to you for free.

For example, StepChangeprovides free and confidential advice to those struggling with debt.

The Link Between ADHD and Debt

Recent research suggests that there is also a strong link between ADHD and poor debt management. It is understood that individuals with ADHD struggle to focus on important and time-sensitive problems.

Consequently, people with ADHD are likely to let small fines and debt escalate into something more serious.

According to the NHS, ADHD is a mental health disorder. And it is legally considered to be a disability.

As such, if you are in debt and have an ADHD diagnosis, it is important that you share this information with your creditors. They may be able to make reasonable adjustments to your debt or repayment plan as required by the Equality Act 2010.

You could also get in touch with a debt charity, such as StepChange, for assistance.

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

From experience, after a loan is written off, the debtor originally responsible for repaying the loan is no longer required to repay it.

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.