Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

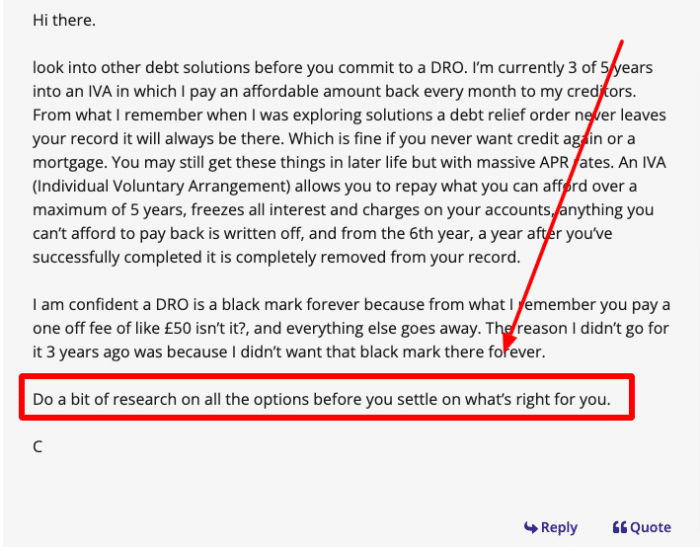

Deciding on the right path to deal with debt can be hard. Are you thinking about an Individual Voluntary Arrangement (IVA) or a Debt Relief Order (DRO)?

You’re in the right place to find answers. Every month, 170,000 people visit our website looking for guidance on debt problems.

In this guide, we’ll help you understand:

How an IVA works and how to apply for it

The process of a DRO and how to get one

The debts that you can include in an IVA or a DRO

The effects of choosing a DRO or an IVA

Which debt solution is better for you: DRO or IVA

Our team is made up of people who have had debt problems too; we understand that you might be confused about the IVA process or concerned about paying off your debt. But don’t worry; we’re here to help you make an informed decision.

Don’t worry, here’s what to do!

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Fill out the 5 step form to find out more.

How does an Individual Voluntary Arrangement Work?

An IVA is a formal and legally-binding agreement between you and your creditors which states that you will make monthly payments towards your debt for an agreed-upon period of time.

This time is typically five years. You will only be obligated to pay an amount of money each month that is affordable to you.

At the end of the agreed-upon duration, if there is debt remaining which hasn’t been paid off yet, it will be written off.

The great thing about IVAs is that they are affordable, manageable and quite flexible depending on what your financial circumstances are like.

You will never be pressured to pay more than you can afford, and as a result of this, you can get a significant portion of your debt written off.

Furthermore, an IVA obligates your creditors to freeze all interest and charges on your debt. Thus, you save a lot of money you would have otherwise had to pay in interest.

Your monthly IVA payments are determined by the disposable income you make every month. You must provide proof of your household income and expenses when applying for an IVA.

If you have a lot of valuable assets, such as a house or a car, then an IVA is the appropriate debt solution. This is because an IVA protects your assets from being seized and sold off by creditors.

While IVAs are a great way to eliminate your debts, some debtors have trouble getting them approved. This is because your creditors have to agree with the terms of your IVA for it to be put in place.

Please note that your creditors are under no obligation to accept your proposal when it comes to Individual Voluntary Arrangements. Thus, there’s a chance that you may have to seek some other way to manage your debt.

Another important thing to note with IVAs is that they stay on your credit file for six years. This is true even if the IVA itself lasts five years. Thus, while your IVA finishes in five years, it still affects your ability to obtain credit for 12 months.

Your name is also placed on the Insolvency Register and it stays there throughout the duration of your IVA. Your name will get removed within three months after your IVA finishes.

The Insolvency Register is a public database that people can look up to determine whether you

As a debtor, you need to be aware of how an IVA affects your life before you apply for one.

How does a DRO Work?

A DRO is a formal and legally-binding agreement between you and your creditors. A DRO lasts for 12 months, and when it is put in place, your creditors are not allowed to contact you regarding your debt or demand payments for them.

After the period of one year has passed, your financial circumstances are reassessed. If it’s found that you still can’t afford to pay back your debt, then your debt is completely written off.

While this may seem like a much more attractive solution than an IVA or a debt management plan, the truth of the matter is that a DRO has very strict eligibility criteria.

To be eligible for a DRO, your debts must total up to less than £30,000. In addition, you must have little to no assets (up to £2000 worth of assets and a vehicle worth no more than £2000 unless modified for a disability) and must have a disposable income of no more than £75.

Please ensure you meet all the eligibility criteria before applying for a DRO.

To get a DRO, you must pay an application fee of £90. You can pay this in instalments if you’d like. Please note that you will not get this money back if your DRO application is rejected.

While it’s true that a DRO is mainly for individuals with little to no assets, you may still get approved for one if you have assets that have a value of less than £2,000 and they are assets which you need for your work or your studies, etc.

A DRO is often considered a cheaper and quicker alternative to bankruptcy because, just like bankruptcy, it results in your debts being completely written off.

It’s important to note that you don’t have to make any payments during the one year a DRO is in place.

Make sure that you are aware that if your financial circumstances do improve by the end of the moratorium period, you will be obligated to pay back your debts.

While a DRO is a formal and legally-binding agreement, it does not need court approval to be put in place.

Please note that just like an IVA, a DRO is also logged into your credit report and has an extremely negative impact on your credit score as a debtor.

It’s also important to note that while a Debt Relief Order only lasts a year, it stays in your credit file for six years.

Which Is Better?

There’s no one solution which is better than the other. It all depends on your financial situation and which debt solution works best for you.

For example, you will never be able to qualify for a Debt Relief Order if you have a ton of valuable assets. Of course, if you have valuable assets, you would want to protect them. In this case, an IVA would be the best choice for you.

On the other hand, if you have little to no assets, there’s no point opting for an IVA, as you would not be reaping the main benefit of an IVA, which is the protection of your assets.

There’s also no point opting for an IVA if you have a spare income of less than £75. This is because your creditors are highly unlikely to agree to the terms of your IVA if you present them with monthly payments of less than £75.

If you want to become debt-free quickly and don’t have a lot of assets, then a Debt Relief Order would be the right choice for you as a Debt Relief Order lasts one year, whereas an IVA can last from anywhere between five to seven years.

As a debtor, you must look at all aspects of your finances, such as your monthly income, expenditure, debts, assets and credit record, to choose between debt solutions.

Debt Relief Orders are typically intended for low-income individuals who can’t afford to repay their debts and are facing financial hardship. In contrast, IVAs are intended for individuals who can afford to repay their debts but just need a manageable framework.

An IVA will protect your assets, freeze your interest and allow you to pay back your debt in a manageable way.

A DRO will freeze your payments for a year and if your financial circumstances after that year has passed, your debts will be written off.

Only through a specific adviser known as an ‘authorised intermediary‘ can you apply for a DRO.

A government official known as the official receiver will decide whether or not to approve your DRO application.

You cannot apply for a DRO alongside someone else. If you and your partner want a DRO, you must apply separately. This means that each of you must pay a £90 application fee.

To apply for an IVA, you must find an insolvency practitioner (IP) through the Insolvency Service website. Each IP will have their own fee schedule, so you must contact them to determine whether they are right for you.

I must reiterate again how important it is to get independent, professional debt advice before agreeing to anything.

What are the consequences?

When you file a Debt Relief Order, it is recorded on the Insolvency Register, together with your personal information.

Because the Insolvency Register is open to the public, the DRO will also be published on your credit report.

This will negatively influence your credit rating in the short term because it indicates to lenders that you have missed debts and had trouble repaying credit.

This can make opening new bank accounts difficult and have mortgage implications.

After six years, all evidence of your DRO will be deleted from your credit file, allowing you to start restoring your credit rating.

IVAs, like DROs, are recorded on the Public Insolvency Register and will thus have a credit score impact.

Having an IVA against your name can make it harder to obtain fresh credit in the short term, but the facts of your IVA will be removed from your credit report six years after your arrangement began.

What Debts can be included in an IVA?

Debts that can be included in an IVA are:

Catalogue debt

Personal loans

Credit card debt

Gas and electric (utility) arrears

Council tax arrears

Overdrafts

Payday loans

Store card debt

Income tax and national insurance arrears

Tax credit or benefit overpayments

Debts owed to family and/or friends

Any other outstanding bill for miscellaneous services

What Debts can be included in a DRO?

Debts that can be included in a DRO are:

Household utility bill arrears such as rent, gas, etc.

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.