Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you worried about letters arriving at your address for someone else’s debt? You’re not alone. Every month, over 170,000 people come to our website for advice on their debt issues.

This helpful guide will show you what to do if you find yourself in this situation. We’ll cover topics such as:

Understanding if you can be held responsible for someone else’s debt.

What steps to take if debt letters or calls are aimed at a past resident.

How to deal with debt collectors who want to visit you over another person’s debt.

What to do if you’re getting letters for a joint debt you’re not responsible for.

How to clear a debt that’s not yours.

Our team has lots of experience with these types of problems. We understand how worrying it can be, which is why we’re here to help you sort it out.

Let’s get started!

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Can You Be Liable for Someone Else’s Debt?

No, you cannot legally be liable for debt that someone else owes.

However, there are certain circumstances in which the loan is either taken through a joint bank account or a joint credit card (joint liability), or there is a personal guarantee (co-signing a loan) given in your name while getting the loan approved.

In these instances, you’re liable for a debt that someone else took.

We must also mention that in the case of marriage, debts accumulated during the marriage may also be considered joint debt, depending on the circumstances and location within the UK.

But if no such factor was involved during the period of loan approval, then you cannot be held responsible for the owed amount later.

If you’re being held liable for such loans, you need to clear out the situation and talk to the creditor regarding the false information they have.

If you don’t recognise a debt you’re being held accountable for, you should get out of it by opening a dispute.

Do not pay any part of the debt until it has been verified, as it can be seen as an admission that you owe the debt.

The action of disputing should be takentimely so that the creditor is very well informed that you’re not the person they are looking for.

But before you can do so, you must confirm that you really are not responsible for the debt. Also, check that the creditor is legitimate.

Ask the creditors to send you both a debt validation notice, as well as provide more information about their company. This is in line with the fair debt collection practices as set out by the FCA.

A validation notice will help you figure out if you really don’t owe them the money and who really is the actual debtor.

Whereas the additional information will serve as proof that the collector isn’t actually trying to scam you.

For example, the company contacting you may be:

Your original creditor

A debt collection agency acting on behalf of your creditor

A third party who has bought the debt from your creditor

Bailiffs in England and Wales or sheriff officers in Scotland.

Important: No matter the situation, never give out your personal information to just anyone claiming to be from debt collection agencies.

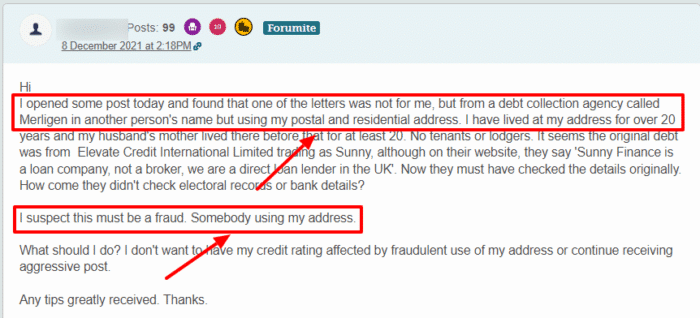

In addition, sometimes being pursued for a debt that isn’t yours can be the result of identity theft or fraud. If you suspect this is the case, tell the debt collector somebody stole your identity, and you don’t owe the debt.

Next, contact the credit reference agencies and tell them to investigate and update your records. Don’t forget to report the case to Action Fraud.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

You must deal with any creditor who might be wrongfully putting you responsible for loans that you did not take.

A timely response is essential in this case because if you don’t dispute a debt within 30 daysof the letter or call, the creditor will assume that you’re liable for the debt and will continue to make efforts to get the money from you.

Be sure to contact the creditor in writing and keep a copy of the letter and proof of postage.

Here are a few ways you can deal with a debt that isn’t yours:

1. Debt Letters Addressed to a Previous Resident

It is somewhat common for creditors to send a debt letter to your home when it actually needs to be sent to the previous resident of your address.

In such cases, simply return the letter to the sender and inform that the actual debtor has shifted.

Such issues happen because debtors fail to inform their creditors of their new address or the creditors don’t update the debtor’s address information on time.

2. Phone Calls & Texts From an Unknown Creditor

If you receive any phone calls from a creditor regarding a debt that isn’t yours, just inform them that it’s the wrong contact and the loan was not taken in your name, so they don’t call you again.

If they still continue to make unsolicited debt collection calls, just write a complaint or block their number.

If you receive a message from a collector for debt collection, however, mistaken identity is very rare here. There’s a greater chance of the debt being illegitimate.

Therefore, don’t respond and just block the number.

If the phone calls and texts won’t stop, consult a solicitor or seek advice from Citizen Advice. Make sure you collect evidence of the harassment from creditors (e.g. calls with dates and times, letters, etc).

You can also complain to the Financial Conduct Authority (FCA).

3. Debt Collectors or Agencies Want to Visit You Over Another Person’s Debt

If a debt collector from an agency comes over to your residence and asks to come inside, don’t let them in if the owed money was not taken in your name.

Ask them to leave, or communicate with them at a safe distance from your house (preferably through a door chain).

They cannot legally take anything from inside your residence if you’re not the person they are looking for.

To deal with bailiffs at your doorstep, show them your council tax, which will be solid proof that the place you’re in is yours, and they are not looking for you.

4. Being Contacted for a Family Member’s or Relative’s Debt

Even if you’re being contacted for debts of your family member, you’re not liable for any of the owed money.

The most you can do is inform your relative about the constant letters you receive and ask them to pay the debt off.

5. Getting Letters for a Joint Debt You’re Not Responsible For

If it is a joint debt, then you are responsible for it. There is no other way around it.

We understand that sometimes you just agree to take a joint loan with someone in your name in order to help them, but it is recommended that you don’t do so.

If the actual debtor stops paying the amount, the creditor will come after you, and rightfully so. And you’ll be liable for the full debt, not just your “half”.

Even if you didn’t spend the money, you’d be required to fully settle the debt.

Besides, your credit history could be damaged by the other person’s irresponsible spending behaviour.

Before you agree to share debt, make sure you’re comfortable with how the other person spends money and know what will happen if you break up.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

If you get a letter of a debt belonging to someone else, here’s how to deal with it: Cross the name on the envelope and write ‘not known at this address’ across it.

Post the letter back to the sender. This should stop them from sending more letters or bothering you anymore.

7. Getting Letters for a Deceased Person with Unpaid Debts

If you’re being contacted by creditors who want to collect a debt from you on behalf of a deceased person, know that you’re in no way liable for the debt.

The deceased person’s debts are supposed to be paid back through their estates, properties, etc.

If that isn’t enough, then the collector will have to write off the remaining debt, and they can’t hold you accountable for that debt.

The only exception is if you had taken a joint loan or had given a personal guarantee for the loan taken. In these cases, you’re liable for the debt.

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.