ACI Debt (Asset Collections & Investigations) Should You Pay?

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Have you received a letter from ACI Debt (Asset Collections & Investigations) and are unsure about what to do? You’re in the right place. This article aims to answer common questions and ease your worries.

It feels confusing to get a letter about debt you might not know about. You may be asking yourself, should I pay? Is this real? What if I can’t pay?

You’re not alone. Over 170,000 people visit our website each month for help on debt matters.

In this article, we’ll help you:

- Understand who Asset Collections and Investigations are.

- Learn why they might be contacting you.

- Find out if you have to pay ACI debt collectors.

- Discover ways to possibly write off some ACI debt.

- Learn about what happens if you can’t afford to pay.

Research shows that 64% of UK adults find interactions with current debt collectors stressful1. So, we understand how you feel. In fact, some of our team members have also dealt with debt collectors.

Don’t worry; we’re here to help. Reading this article will give you more knowledge about ACI Debt and what steps you can take next. Let’s get started.

Why are they contacting me?

Usually, companies like ACI debt collectors will get in touch because a creditor has passed on your information to them.

This often means that you have an outstanding debt with another company, and they’ve failed to recover it. In some cases, ACI might be legally assigned to deal with your account.

This is quite common, as debt collection agencies buy billions of debt annually at rock bottom prices- at an average of 10p to £1! 2

Asset Collections and Investigations will try and recover whatever money you owe. They will provide you with a variety of payment options, but ultimately will want you to pay however much you initially borrowed, plus some interest and fees.

Typical Collection Process

Understanding the debt collection process is crucial when dealing with ACI debt collectors. The quick table below explains the key stages and actions involved, helping you learn how to manage your financial situation. If you’d like to learn more, don’t forget to read our specialized guide.

| Stage | Actions | What you should do: |

|---|---|---|

| Missing one or two small payments | Calls and letters from the debt collector asking for payment. They may enquire about reasons for missing payments. | Contact the debt collector and offer to pay what you can. If you are struggling to pay the debt, get in touch with us to explore your options. |

| Missing large or multiple payments | Their contact will become more frequent, urgent, and threatening. | Contact the debt collection agency and offer to pay what you can. You may also make a complaint if you think the letters are a form of harassment. |

| Debt collector visit | After a few months, if the debt is significant (£200+) you will receive notice of a debt collector visit. They have to notify you before arriving. Debt collectors cannot take anything from your home – they may only ask for payment. | If a debt collector shows up at your home, ask them to show proof of the debt and their ID through a window. Do not open your door or let them in. You can arrange a payment plan with the debt collector, but make sure to get a receipt of this. |

| Court | If you still do not pay your debts to the original lender/debt collector agency, they will take you to court and either attempt to: – File a CCJ against you. – File an attachment of earnings order. – File a lawsuit against you. |

You must show up to your court date. From here, you can either dispute the debt, or the judge will likely suggest a manageable repayment plan for you. |

Do I have to pay them?

» TAKE ACTION NOW: Fill out the short debt form

This is another frequently asked question when dealing with debt collectors.

Ultimately, we all have to pay our debts somehow. However, the exact circumstances of your debt will determine whether or not you have to pay ACI.

There are two main things to consider here. The first is whether your debt is too old to be enforced.

If it has been 6 years – or 5 years in Scotland – since you last made a payment towards your unsecured debts and you have not written to your creditor about your debt during this time, it is statute-barred.

This means that the debt is not enforceable. It still technically exists, and you still technically owe the money, but there is no legal way for you to be forced to pay or for the debt to be enforced.

Keep in mind that not all debts become statute-barred!

Any HMRC debts, for example, will stay enforceable for decades. Any debt that had a County Court Judgement (CCJ) attached to it during the 5 or 6-year window will always be enforceable.

The second thing to think about is whether or not they can prove if the debt is actually yours to begin with. However, if the creditor or debt collector cannot prove you owe the money, they can’t make you repay it.

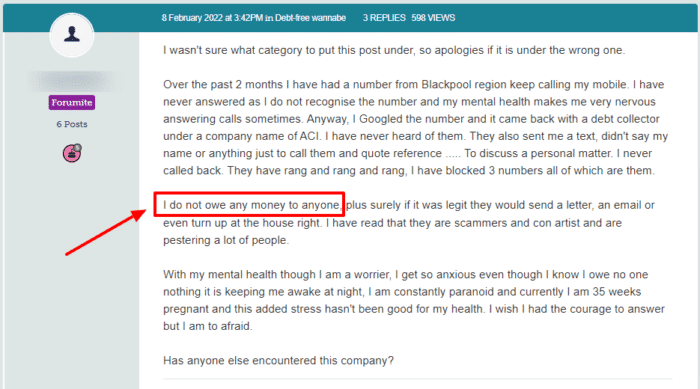

Sometimes debt collectors make mistakes and contact the wrong people about debt. Look at this example:

This person may need to write to ACI and tell them that they have the wrong person. This may be enough to get them off their back!

You can find a ‘prove the debt’ template online, which outlines the necessary FCA guidelines.

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Should I ignore them?

It’s never a good idea to ignore companies like ACI debt collectors. In reality, it’s not going to make them go away or forget about the money you owe. All it means is that they’ll continue to hound you and they may take more action against you.

Of course, it’s understandable that you might not want to face up to a difficult financial situation. However, it’s important to know that there are plenty of options available for helping you deal with your debts.

The first thing you should do when you hear from a company like ACI is to reach out to them directly. They may be able to help you come up with a repayment option that is more manageable for you.

Ignoring them or refusing to pay at all will probably mean that ACI take you to court.

What action can they take?

If you continue to ignore and refuse to pay ACI, there are several steps that they or the creditor might take. The first thing they’ll do is add charges and interest to what you owe. This can mean you eventually have to pay back more.

Next, they might try taking a CCJ (County Court Judgement) against you. This is a legal order forcing you to pay your debts and it can have serious implications for your financial health.

If you continue to refuse to pay, the creditors or debt collectors might petition to have the bailiffs sent to your home. If a bailiff comes, they can seize your belongings to cover any debts that you owe.

We recently spoke to the Mirror about debt collectors and bailiffs. While a bailiff may be permitted to take your possessions, a debt collector never can. All they are allowed to do is ask for a payment.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

Does a CCJ affect my credit score?

If ACI takes you to court, they will be doing to get a County Court Judgement (CCJ) against you.

A CCJ is an order from a judge to pay your debt. The court will provide you with a payment scheme to follow. If you don’t stick to it, ACI may take you back to court to get bailiffs authorised.

A CCJ will have a very negative impact on your credit score and will be visible on your credit file for 6 years.

During this time, you will probably find it just about impossible to get credit. This is because a CCJ flags you as a ‘high-risk’ customer – someone who is likely to have difficulty paying back their debts.

After 6 years your CCJ will no longer be visible and you will probably find it a bit easier to get credit.

What if I can’t afford to pay?

If you can’t afford to pay ACI in one go, they have to offer you a payment plan.

You may be able to negotiate a freeze in your interest or even a brief payment holiday to help you get back in control of your finances.

But what if you still can’t afford to pay? You may need to consider a debt solution.

There are several debt relief options available in the UK, so we recommend speaking to a debt charity. Their advisers will be able to help point you towards the best debt solution for you. We have linked a few organisations that offer free debt counselling services at the bottom of this page.

Debt Management Plan (DMP)

A DMP is an informal debt solution that lets you pay off your debts via a single monthly payment.

Because it is informal, it is not legally binding so you are not tied into a DMP for a minimum number of payments.

Individual Voluntary Arrangement (IVA)

An IVA is a formal agreement between you and your creditors. You agree to pay a monthly sum that is distributed amongst your debts, and your creditors agree not to contact you during your IVA.

IVAs typically last for 5 or 6 years, and any outstanding debt is wiped off when it ends.

Keep in mind that IVAs are not suitable for everyone. You need to owe several thousand pounds to more than one creditor to be eligible. You also need to demonstrate that you have some disposable income every month.

Trust Deed

IVAs are not available in Scotland. Instead, you will need to opt for a Trust Deed.

Trust Deeds work in the same way as an IVA – you pay an agreed sum each month that is shared amongst your creditors, they can’t contact you, and any leftover debt at the end of your Trust Deed term is written off.

Debt Relief Order (DRO)

A DRO is a good option for those facing financial hardship with no assets and little income.

For 12 months, you make no payments, but your creditors freeze your interest and don’t contact you.

If your finances haven’t improved during this year, you may be able to write off your unsecured debts.

Bankruptcy

If you have debts but no realistic possibility of ever paying them off, you may need to declare bankruptcy.

Bankruptcy has an unfair stigma attached to it as it may be your only way of getting a financial fresh start. That said, it is a serious financial situation that should not be taken lightly.

Sequestration

Sequestration is the Scottish version of bankruptcy.

If you have little income and not valuable assets, you may be able to apply for a minimal asset process bankruptcy (MAP). A MAP is a quicker, cheaper, and more straightforward version of sequestration so worth considering.

How do I complain?

If you think that ACI has been unreasonable or behaved inappropriately, you can make a complaint. You can also make a complaint if you feel that they have broken any of the Financial Conduct Authority’s (FCA) guidelines.

Make your first complaint to ACI so that they have the chance to sort out the issue themselves. Fortunately, the ACI Debt complaints procedure is quite straightforward!

aIf you feel that they have not taken your complaint seriously enough or have not addressed your issue properly, you can escalate matters.

You can make any secondary complaint to the Financial Ombudsman Service (FOS). They will investigate and, if your complaint is upheld, Arvato may be fined. You could even be owed compensation.

ACI Debt Contact Information

| Post: | ACI, PO Box 123, Blyth, NE24 9ES |

| Telephone: | 01253 531528 Monday to Thursday 8:30am – 6:00pm Friday 8:30am to 5:30pm |

| Email: | [email protected] |

| Website: | https://www.aciuk.co.uk/ |

Where can I get help?

If you are dealing with a debt collection company or just struggling to manage your money, we recommend speaking to a debt charity.

There are several charities and organisations in the UK that offer free debt counselling services and free financial counselling services. Their advisers will be able to walk you through your options and find the best solution for you.