Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you wondering if you have a County Court Judgment (CCJ)? You’ve come to the right place. Over 170,000 people visit our website each month looking for guidance on debt solutions, including CCJs.

This article will help you:

Understand what a CCJ is.

Learn how you can check for a CCJ for free.

Find out how to deal with a CCJ if you’ve got one.

Discover ways to improve your credit score if you’ve had a CCJ.

We know the stress a CCJ can cause, as we’ve been there too. But don’t worry; we’re here to help you understand how to check for a CCJ and what steps to take next.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Here’s How You Can Check

The easiest and free way to check if you have a County Court Judgment is to get a copy of your credit score. This is also a great way to check what debt you owe.

You can get a copy of your credit score for free using:

Always use a credit rating agency that is registered in England and Wales, and is regulated by the Financial Conduct Authority (FCA). That way, you can be more sure of an accurate search.

You can also check if you have a CCJ against your name using the CCJ register online, but the process is a bit complex. However, it offers more details than online CCCJ checks on a credit referencing website.

A County Court Judgment will be listed on your credit report as such.

All you need to do is to consult your credit score online to see if you have a CCJ. For extra reassurance, you may want to consult the CCJ register, which can also be done online.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Can you check with credit reference agencies for free?

If this is your first time using a credit report agency, you should know that they typically charge a small subscription fee.

Many agencies, nonetheless, will allow you to browse for free for so long before charging you an account subscription fee.

To avoid paying the agency, you should sign up and unsubscribe before your trial ends. Use this opportunity to check for a CCJ for free.

Another option is to use an alternative credit reference agency to check your CCJ so you don’t have to pay. Free CCJ checks with credit reference agencies are possible with the following:

Experian.co.uk

Equifax.co.uk

TransUnion.co.uk

How do you find out who you owe a CCJ to?

Although it is relatively easy and free to check if you have a CCJ against your name, the same cannot always be said for finding out to which creditor you owe the money.

However, details such as the court that issued the CCJ will appear on your credit report.

You can then contact that specific court to ask whom you owe the money. There is typically a £6 fee to make this request.

Most people will automatically know the creditor that pushed for a CCJ because the creditor will have chased them for the debt previously.

But if you find out you have a CCJ out of the blue, it could be a mystery until you do some digging.

Is a CCJ public information?

When a County Court Judgment is issued, it is added to a public register, namely the Register for Judgments, Orders and Fines.

This means members of the public will be able to see a record of your CCJ.

If you have been issued a judgment recently, you might be able to stop it from being recorded on the register – thus avoiding it appearing on your credit file and affecting your credit rating. All you have to do is pay the full amount owed within a month from the date it was issued.

If you pay back in full but after 30 days of the date the CCJ was issued, it will appear on the public record of CCJs and your credit file.

It will, however, be recorded as satisfied.

Your CCJ is kept in the register for six years. However, the “CCJ register” does not contain records about lenders or claimants.

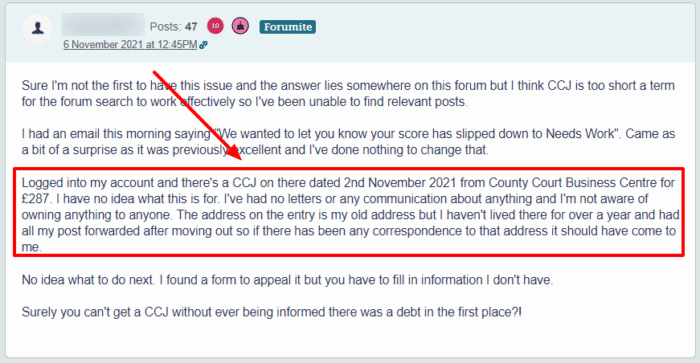

Can you have a CCJ without knowing?

You should be informed if you are being taken to the County Court about a debt in a letter of claim.

However, there are limited cases where the CCJ notification process is not followed correctly, or due to incorrect address issues, you are not notified of the legal action or the subsequent CCJ.

These instances are uncommon but not impossible.

The creditor is allowed to serve notice at your last known address if extensive measures have been taken to find your new address without success.

If you haven’t been notified of a CCJ by post but have a CCJ on your credit report as this forum user claims, you should check if you have a CCJ against your name.

We suggest you contact the court where the judgment was issued as soon as possible to have the CCJ set aside.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Debtors can apply to have a CCJ set aside (or cancelled) for several reasons.

One of the most common reasons to ask for this is that you did not receive notification of the claim at your correct address.

As we mentioned earlier, you should receive a letter of claim at your address beforehand so you have the chance to defend yourself or dispute the claim.

But you should not try to have the CCJ set aside if you know you owe the debt and believe you will not be able to defend the case successfully. Doing this as a delaying tactic will result in your defence being rejected, and you could end up paying more fees.

The CCJ set aside process varies depending on your circumstance. The court will also set the CCJ aside if:

The judgement was entered in error. In that case, request the court to set the judgement aside. You’ll pay £255 or more in court fees.

You paid the money before court date. Apply to have the CCJ set aside by providing the court with proof of payment.

The CCJ was cancelled because you paid the full amount within one month of it being issued.

How long will one last?

If you receive a CCJ and pay the full amount within one month, the CCJ will not appear on your credit report. But the judgment might still be reported by credit reference agencies during that month.

If you pay after one month, the CCJ duration on your credit report is six years, and your record will show that you’ve paid the debt.

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.