Welcome! If you’re worried about your credit score and want to know what the ClearScore bands mean, you’re in the right place.

Each month, over 170,000 people visit our website for guidance on topics just like this one. You’re not alone.

We understand your concerns and are here to help you. In this easy-to-read guide, we’ll explain:

The five ClearScore bands and their meaning

The difference between ClearScore and Equifax

Ways to improve your ClearScore band

How to manage if your ClearScore rating goes down

What is considered a good ClearScore in the UK

We know that credit scores can be confusing, especially when they change. Don’t worry; we’re here to help make sense of it all for you.

By the end of this article, you’ll have a better understanding of what your ClearScore means and how to improve it. Let’s get started!

What is the difference between Clearscore and Equifax?

Equifax is one of the three main credit reference agencies in the UK. ClearScore is not a credit reference agency.

Rather, ClearScore provides users with access to the data that Equifax holds on them, free of charge.

What are the New Clearscore Bands?

Before April 2021, Equifax had a credit score scale out of 700. Additionally, Equifax used five rating bands, which helped you to understand how good or bad your credit score was.

These bands were as follows:

Very Poor

Poor

Fair

Good

Excellent

But then things got updated which saw the credit score rating systems change. As such credit score values changed. But the influence of credit bands on lenders isn’t affected.

As of April 2021, Equifax UK credit scores are no longer measured according to the scale above.

Many people who were in the Poor band before are now in the Fair band

The Good band is larger than it was and so more people will find themselves in it

The Excellent band is split into 2, Very Good and Excellent. Some people who were in the old excellent band will find themselves in the Very Good band.

You may have found yourself in a different Clearscore band. This doesn’t necessarily mean that your credit score has improved.

The benefits of a good Clearscore credit score are numerous. It helps you to obtain better deals and credit at better rates.

Having a poor credit score doesn’t always mean obtaining credit is impossible. However, the deals you get on your credit products will come with higher interest rates.

What is a good credit score out of 1000?

What is considered to be a good credit score in the UK depends on the credit reference agency used.

According to Experian, a score between 881 to 960 is good. Whereas, a good Equifax UK credit score is between 670 and 739 is good.

However, lenders in the UK tend to consider individuals with credit scores higher than 670 as fairly low risk.

So, comparing credit scores across agencies can be a little confusing since the changes were implemented.

Why is my Clearscore rating So Low

The reasons for low Clearscore ratings have left many people confused.

After the new Clearscore score bands were released, some people discovered they had fallen into a new, lower band.

For example, an individual with a credit score of 420 was Good in the old banding system. The same credit score of 420 now lands the individual in the Poor band.

This can come as quite a shock, especially for those who have actively worked on improving their score.

Remember, just because the name of the band you fall into has changed, your credit score remains the same.

Therefore, lenders will not see your score any differently. They will have the same thoughts about your credit record as they did before, regardless of the label the new Clearscore band gives you.

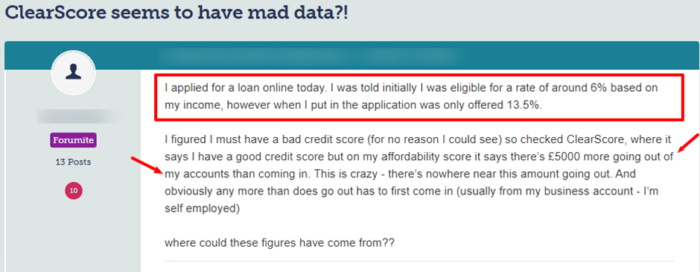

Check out this message a concerned person posted on an online forum.

Your Clearscore credit rating may have dropped for several reasons. In short, there are some factors affecting Clearscore ratings which I’ve listed below:

Late or missed payments.

A change in your credit limit.

Expensive purchases.

An application for new credit (e.g., a new credit card, loan, or mortgage).

Closed or cancelled credit cards.

How Can I Improve It?

I’ve listed some tips for improving Clearscore ratings here but, the most important factor in your credit rating is your credit history.

This is what is used to come up with your score.

Improving your credit history does take time, but following the tips I share below is a great place to start:

Make all payments on time and don’t miss a payment. Pay everything on time whether it’s your phone bill, water bill or credit card payment. Missed payments are worse than late ones, but late ones do harm your credit score too.

Remove your ex-partner from your credit history if you’re no longer financially connected

Use your credit responsibly and pay on time to build trust with lenders

Check your credit score to ensure it is correct

Don’t apply for lots of credit products in a short period

Ensure you’re on the electoral register

Try to keep your credit card balances below your credit limits

Work with debt advisors, especially when struggling with debts. They can help you to work out agreements with lenders and potentially avoid CCJs or bankruptcy, which can seriously affect your credit rating for many years.

I have some useful articles on how to deal with debt and the threat of CCJs, have a read if this is a present concern.

What is the Highest Clearscore Score?

The highest Clearscore score is 1000. A score between 811 and 1000 places you in the Excellent Clearscore band.

The benefits of high Clearscore scores will help you to get the best credit terms when borrowing.

What the Score Bands Mean to You

Knowing your Clearscore score band is a great way of helping you to understand the health of your credit rating.

In short, the personal implications of Clearscore bands can impact many aspects of your financial standing.

Clearscore uses the same scale and rating as Equifax.

The Clearscore score ranges from 0 to 1000.

Your credit history determines your score and the band that score will fall into on the scale.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!