Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you worried about a bailiff company threatening you with Section 69 of the County Courts Act 1984? You’re on the right path to finding answers. Each month, over 170,000 people come to us seeking guidance on debt issues just like yours.

In this easy-to-understand article, we’ll explain:

What Section 69 of the County Courts Act 1984 really means.

How to handle bailiffs and avoid your things being taken.

Ways to calculate the interest you might owe.

Tips on how to avoid court action over debt.

Advice on dealing with big debts.

We know it’s stressful when you’re dealing with bailiffs. Some of our team members have been in the same boat. But remember, there’s always a way out.

Here’s how you can handle the situation in the best possible way.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

What is the County Courts Act 1984?

The County Courts Act 1984 is an Act used to regulate the way county court proceedings are conducted in the United Kingdom, including matters relating to debt. It was devised in 1984 but has been updated and amended over time. The Act covers a wide range of topics, not just debt-related issues.

What is Section 69 of the County Courts Act 1984?

In Section 69, the law states that a claimant can ask the debtor to pay interest on the money they failed to repay. This means when a debtor is asked to repay the debt by a judge, the court can make a further judgment asking the debtor to pay interest on the debt as per a claimant’s request.

There’s something identical for those claiming damages against a company for breaking contractual terms.

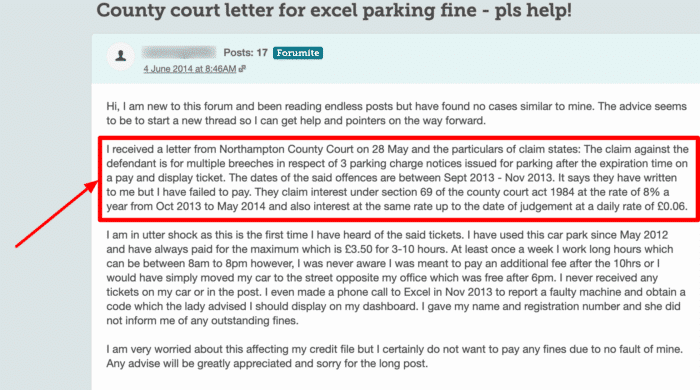

Here, you can see this forum user on MoneySavingExpert has received a letter saying interest will be claimed against them as part of the County Courts Act 1984 Section 69 and they are looking for advice.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Under theCommercial Debts Interest Act 1998, also known as the Late Payment of Commercial Debts(Interest) Act 1998, the plaintiff may claim a statutory rate of interest at 8 per cent per annum.

This interest can be added to commercial debts where one company claims against another company for contractual damages or breaking the terms of a contract, resulting in damages or debt. This interest payment of commercial debts must also be claimed, as there is no automatic right to the interest payment. If there is no claim made, the 8 per cent interest rate would not be applied.

Is statutory interest simple or compound?

This base rate of interest applied to the debt under the 1998 Act is simple interest rather than compounded interest.

The difference between simple and compound interest is that simple interest is calculated on the original (principal) amount, whereas compound interest is calculated on the original amount and on the interest already accumulated on it.

How do I calculate statutory interest at 8% per year?

If you are trying to calculate how much interest your creditor may claim from you, it is possible to work out the statutory interest of your debt. However, it’s not as simple as just working out 8% of the debt owed.

The 8% interest calculation method is done by:

Multiplying the total debt amount by 0.08

Divide the answer to the above by 365 (= daily rate of interest)

Multiply the daily rate of interest by the number of days the debt has been owed

For example, if you have a debt worth £500 that you have owed for 100 days. The claim would be calculated as follows:

500 (money owed) x 0.08 = 40 (= annual rate of interest)

40 / 365 = 0.11 (= daily rate of interest)

0.11 x 100 (days) = 11

In this case, the statutory interest rate of 8% would equal a sum of £11 awarded to the claimant in interest and thus added to the debtor’s account to be repaid.

Why you should aim to avoid legal action

If you genuinely owe money on a loan or credit card, you should aim to avoid legal proceedings. Making a late payment is not the end of the road, and you can still do plenty to avoid a court date and the risks of legal proceedings.

Being taken to court might not just make you pay more back in interest (if claimed), but you may be charged with the creditor’s solicitors’ fees for the trial and other fees relating to the recovery of the debt, including enforcement action.

Unpaid debts and legal actions could also have long-term financial implications, such as potentially affecting your credit score, so the way I see it, it is best to avoid them taking legal action if you can.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

The initial ways to avoid going to court and potentially having to pay a rate of 8% interest is to communicate with your creditor and:

Negotiate a Payment Plan

Many creditors will welcome offers to repay via a new repayment plan. Often, they will reduce the amount you have to pay but may increase the interest so you pay more over time.

Although this might not be ideal, the monthly sum you will pay is affordable and prevents you from experiencing further financial difficulty.

Before you agree to a repayment plan like this, ensure you have worked out an accurate budget. Only by knowing what you can realistically afford to repay can you commit to a new agreement with the confidence of not making the situation worse.

We have a great budgeting 101 guide to help you do just that and to help you manage your money in the future, too.

Use Free Debt Solutions

But you don’t have to agree to a payment plan directly. Instead, you could use a free debt solution offered by charities, such as a Debt Relief Order or a Debt Management Plan.

There are a number of excellent charities acting on behalf of debtors to make debt recovery less stressful.

Some charities cannot provide formal debt solutions, such as Individual Voluntary Arrangements (IVAs).

If you need one of these or other more complex solutions with lots of details, you would need the support of an insolvency practitioner at a debt management business. You pay for their help, but they can sometimes save you money.

More assistance with late payment of commercial debts

If you are due to face legal action and want to know more about fixed interest entitlement among creditors, industry news or debt solutions, we recommend speaking with a registered charity offering advice services.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.