Debt over 10 years old in the UK – Can You Be Chased? Laws

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you wondering if you have to pay a debt that is over 10 years old? You’ve come to the right place for answers! Every month, over 170,000 people visit for guidance on debt issues.

This article will help you understand:

- What it means when a debt is over 10 years old.

- If you can still be chased for this debt.

- What to do if you are unsure about an old debt.

- How to deal with debts you’re not responsible for.

- How to get free and impartial debt advice.

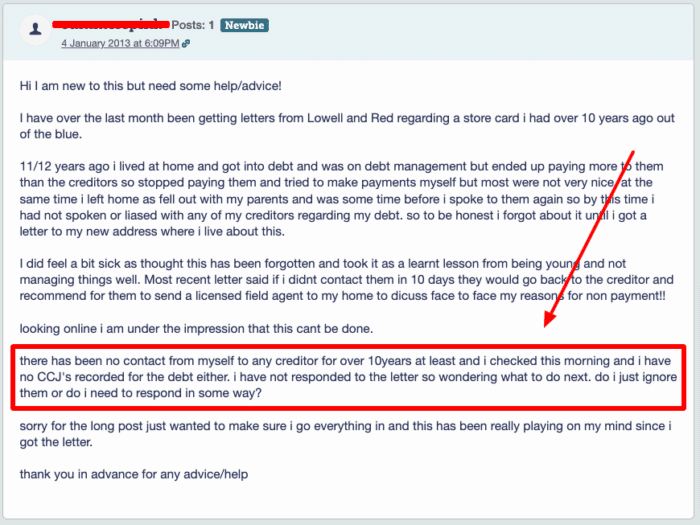

A study by Citizens Advice found evidence of poor practices by debt collectors in the UK, including the collection of very old debt.1 So, it’s understandable to be concerned about your debt.

Don’t worry; you’re not alone! We’re here to help you find ways to deal with it.

Paying your debts over ten years old

Debts over ten years old also come into play, so read on to find out what to do.

Debts you’re not responsible for

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

‘Statute-barred’ – Debts over six years old

» TAKE ACTION NOW: Fill out the short debt form

Can I be chased for debt after ten years?

A County Court Judgement (CCJ) can also be chased.

A CCJ can be enforced for up to six years without permission from the court. If the creditor wants to enforce the judgment after this period, they must get permission from the court.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

Where can you get free and impartial debt advice?

The following debt advice services can give you more information on debt solutions, such as a debt management plan (DMP), Individual Voluntary Arrangement (IVA), debt relief order and more.

| Organisation | Website | Phone number |

| Stepchange | http://www.stepchange.org | 0800 138 1111 |

| National Debtline | http://www.nationaldebtline.org | 0808 808 4000 |

| Citizens Advice | http://www.citizensadvice.org.uk | England: 0800 144 8848 Wales: 0800 702 2020 |