Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you searching for ways to cancel a trust deed? Or, perhaps you’re interested in knowing more about trust deeds.

Either way, you’ve made the right choice by being here. Each month, over 170,000 people like you visit our website seeking advice on debt solutions.

In this easy guide, you’ll learn:

What a trust deed is and how it works

How to cancel a trust deed

What happens after your trust deed ends

If you can write off some debt

Who to contact for help

According to the Money & Pensions Service, 700,000 people are either in problem debt already, or are at risk of experiencing problem debt.1 So we know how hard this can be.

But don’t worry. We’re experts on money matters, and we’re here to help you understand and deal with them.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

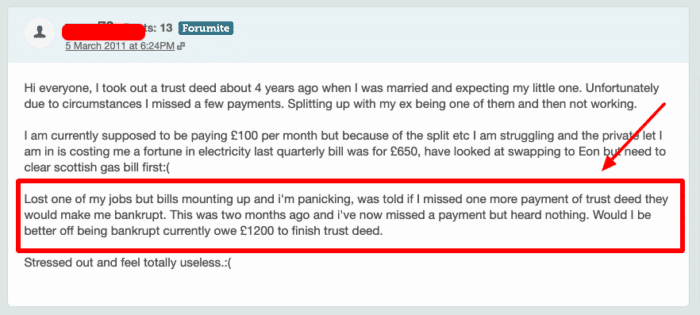

Cancelling a Trust Deed

A Trust Deed is a legally binding agreement thatcannot be revoked at will.

If you cannot pay the installments your creditors find acceptable, your Trust Deed may fail.

The failure of a Trust Deed will most likely lead to your sequestration – so you could lose your belongings.

People often contemplate cancelling their Trust Deed due to unexpected life changes such as employment shifts, unexpected expenses, or financial circumstances.

Understanding these reasons can add clarity to the process.

Apart from sequestration, cancelling a Trust Deed can also impact your credit rating for several years, making it challenging to obtain future credit or loans.

It’s also worth noting that your financial stability could be at risk if you face aggressive actions from creditors.

Its terms bind you once you’ve entered into a Trust Deed.

However, like any contractual agreement, there are stipulations and nuances. It’s always recommended to consult with a legal professional if considering cancellation to minimise the financial implications of cancelling a Trust Deed.

How will you cancel a Trust Deed?

There is a straightforward method to come out of a ScottishTrust Deed, yet it needs your trustees to consent.

They could contact your creditors as part of the Trust Deed termination process, prompting them to say they mean to end the Trust Deed and are looking for their discharge.

This would impact returning you to the starting point, and then you could set up an installment plan/Debt Arrangement Scheme (DAS) if you wish, all things considered.

Remember, if you cancel a trust deed, you are no longer covered by protection from creditors.

It will be written in your agreement that it is so long to run for and when you will be discharged.

Typically it is forty-eight months, i.e. four years from the date you sign it (however, it tends to be longer). Be that as it may, this release isn’t automatic, unlike what happens in sequestration.

Your creditors must release your trustees before you can be discharged. This implies that a Protected Trust Deed may stay open in the Register of Insolvencies for quite a while after four years.

Your discharge is generally binding on the entirety of your creditors.

This implies they can’t pursue you for the money you owed them before you consented to the arrangement.

Yet, there are two exceptions. These are;

Debts not covered by the arrangement (like overpayment of social security), or if a creditor who protested the agreement can demonstrate in court that he would have more cash back if he had been bankrupt. This is an exceptionally uncommon function in reality.

In the event that the Trust Deed fails to get protected, your discharge doesn’t stop creditors who protested in any case still pursuing you for the money you owe them.

Consistent communication with your trustee is crucial.

Whether facing difficulties with payments or simply needing clarity on your agreement’s details, your trustee is there to guide and support you throughout the tenure of your Trust Deed.

Other ways available

There are a few different ways to manage personal debts in Scotland. Scottish Trust Deeds aren’t accessible to everybody (and aren’t the ideal alternative for everybody either).

A Debt Payment Programme under the Debt Arrangement Scheme is one alternative. It could allow you to completely reimburse your debts while your regularly scheduled instalment is diminished to a reasonable sum. Interest stops, and you have lawful security from your creditors.

This alternative likewise offers some adaptability, similar to emergency payment breaks.

A Debt Management Plan could push you to reimburse your debts completely. It’s not ensured that interest will stop, and no formal lawful protection is granted.

Your regularly scheduled instalment is diminished to a moderate sum. This is an especially adaptable alternative.

Bankruptcy is utilized to manage more critical debt issues. It works likewise to a secured Trust Deed; however, it probably won’t be appropriate for some mortgage holders.

You can go bankrupt regardless of whether you can’t manage the cost of a regularly scheduled instalment (in contrast to the other debt arrangements).

Who do you contact for help?

If you are struggling with debt, you should look for counsel at the earliest opportunity.

Seeking advice and managing your debt at the beginning phase may assist you in avoiding the more severe outcomes of being in debt, for example, legal activity by your creditors or sequestration.

Various people can give free, classified, and unprejudiced money guidance vis-à-vis in your neighbourhood.

A few associations may likewise offer information and guidance via phone. If you request guidance, ensure the individual managing you knows you live in Scotland. Debt regulations and solutions can differ significantly across regions.

Therefore, for those residing in Scotland, it’s crucial to seek advice tailored to Scottish laws and financial practices

Some helpful contacts who will offer free advice on debt

Could you legally write off some debt?

Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.