Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you wondering how long a debt can be chased? You’ve come to the right place. Every month, over 170,000 people visit this site for advice on debt matters.

This article will answer your queries and guide you on:

Understanding the time limit for chasing a debt in the UK.

Whether you need to pay a debt older than six years.

How the statute-barred limitation period works.

Checking if your debt needs to be paid.

How to deal with debts you’re not required to pay after six years.

It’s quite common to feel concerned about debt. After all, a study by Citizens Advice found evidence of poor practices by debt collectors in the UK, including the collection of very old debt.1

Don’t worry! Our aim is to provide you with clear, simple information to help you make the best decisions.

Let’s get started.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Do I Have to Pay a Debt Older than 6 Years?

There’s a chance you won’t have to pay a debt if it is older than six years old. This does depend on a few factors.

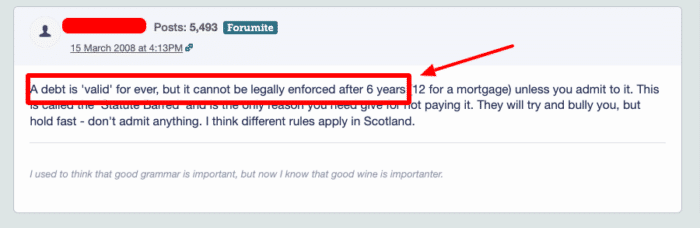

Debts older than six years can become statute-barred.

The Limitation Act 1980, or the Statute of Limitations, decided on the length of time that creditors can chase a debt.

Not all debts will fall under statute-barred territory.

The Limitation Act 1980 only applies when there has been no acknowledgement of the debt or payment towards the debt in the limitation period and only applies to residents of England and Wales.

Paying off debts in the UK older than six years is necessary if you’ve had a CCJ issued against you during the limitations period. The limitation period is how long the creditors and debt collection in the UK must take court action against you.

This will depend on the type of debt it is (unsecured/secured) and to who you owe the money.

A CCJ can have some pretty severe effects on your credit record, so take advice from debt charities such as Stepchange before it gets to that point.

Plenty of options are available to help you manage your debts and avoid the CCJ (County Court Judgement) implications.

When Does the Statute-Barred Limitation Period Start From?

The date the limitation period begins can be the most recent from any of the following.

When you or a third party acknowledges that you owe the debt, make sure you state that you don’t owe it during all communication, be it a letter, email, or phone. Keep a copy or record of all communication you make, as you might need it to use as evidence to support your claim.

From the date of your last payment made towards the debt. The payment counts if it was made on your behalf by a third party, such as a debt management service.

A defaulting term date or time when the creditor could have started legal action against you but failed to do so. This information is found in the terms and conditions of the loan but not always. If the creditor began court action at the time, the debt cannot become statute-barred.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Before dealing with debt collectors, the first step is deciphering if you must pay the debt and if it’s now statute-barred.

Begin by looking at the debt and calculating how long has passed since you last paid on it. You must also check to see if it has been six years since you last contacted the creditor.

You may not have to pay the debt you owe in other circumstances, too, including:

If you felt pressured into signing the agreement by the creditor

If the creditor didn’t make the terms of the agreement clear at the time of signing

The creditor failed to check that you could afford the repayments at the time of signing

The debt isn’t yours

Speak to UK Debt Management Services for free and impartial advice if you are not sure.

Understanding secured and unsecured debts is important, so check out this guide.

Remember, you must not have paid or acknowledged the debt for six years for it to meet Statute-barred debts criteria. These debts must also be paid if they have a CCJ issued against you within the limitations period.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Secured loans such as mortgages have an extended time limit.

These secured debts can be chased for up to 12 years. Additionally, different debts can be chased indefinitely.

These debts include money owed to HM Revenue and Customs, such as income tax, VAT, and capital gains tax. You also must pay money owed to the Department of Work and Pensions for benefit overpayments.

Will My Old Debt Be Written Off?

Having a statute-barred debt older than six years doesn’t mean the debt is written off.

The debt won’t simply disappear. It will still appear on your credit file, which can have serious implications when seeking credit.

Furthermore, the creditors can continue to ask you to repay the debt. They can’t legally enforce debt repayment under debt enforcement in the UK.

Many creditors will continue to chase a debt that is statute-barred. If you want to check debt to see if it is no longer enforceable, there are steps you can take.

Check your credit file.

Inform your creditor that the debt is statute-barred and enforcement is no longer an option.

You can avoid getting a CCJ if your creditors take you to court and can prove the debt is statute-barred.

It’s also possible to stop debt collectors from harassing you and removes the need for dealing with debt collectors. You can achieve this by reporting them to the Financial Conduct Authority or taking them to court.

Remember to keep proof of postage and a copy of any communication you make with the creditor and only write to them if you’re certain the debt is statute-barred.

Get Help with Your Debt

You don’t have to panic or deal with debts alone. There are debt advisors that will help you.

If you’re dealing with debt collectors, want to establish if a debt is statute-barred, or simply wish to avoid debt building up, contact one of the debt advising services in the UK:

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.