Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you worried about your loan debt? Do you feel it was sold to you unfairly? This article is here to help. Each month, over 170,000 people turn to us for advice on debt solutions.

In this easy-to-understand guide, we’ll show you:

What an “unaffordable loan” means.

How to gather proof of an unaffordable loan.

The steps to make a simple claim for a refund.

When and how to take your claim to the Financial Ombudsman Service.

Ways to avoid common mistakes when claiming a refund.

Dealing with debt can be challenging, and it’s common to feel unsure about seeking help. In fact, Citizens Advice revealed that 60% of adults facing financial difficulties hesitate to seek assistance.1

If that’s your case, don’t worry — you’re not alone. We’re here to guide you through the steps to possibly get a refund on your loan if it was irresponsibly sold to you.

Let’s tackle this and discuss your options.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

What is an “unaffordable loan”?

If you couldn’t make repayments without borrowing more from another loan or credit card, then your loan was probably “unaffordable”.

The Financial Conduct Authority says:

“the borrower should be able to make the required repayments without undue difficulty, whilst continuing to meet other debt repayment obligations and reasonable regular outgoings.”

For the loan to be affordable, you should have been able to repay the loan AND have enough left over to pay other expenses such as rent, bills, food etc.

It should not cause you financial distress.

If you rolled over your loan or borrowed more soon after paying off your loan, or your loans were getting bigger each time and breaking the interest rate cap, this would be good evidence that the loan was unaffordable.

Also, if your loan was a significant part of your outgoings or missing some of the repayments, this is a good indicator that the loan was unaffordable and that your provider was loan mis-selling.

Here’s some extra ammunition…

The Financial Conduct Authority has made it clear how lenders must behave. They recently came out with a list of rules. If you think the lender has broken any of these responsible lending practices, you could add them to your claim. Lenders must not:

Refuse to negotiate with you if you are developing a repayment plan.

Refuse to deal with a not-for-profit debt advice body, debt counsellor, debt management firm or with another person acting on your behalf unless they can demonstrate that there’s a good reason for doing so

Pressurise you to pay a debt unreasonably – for example, within too short a period of time or in amounts you can’t afford

Take disproportionate action to recover the debt, for example, initiating legal action unless they have fully explored other solutions.

Make empty threats of actions which they don’t intend to take or are not entitled to take

Budget Advice

Understanding how to budget effectively can be crucial, particularly when facing the challenges of unaffordable loans.

I’ve put together this table that provides 10 simple tips that will help you lower your expenses.

Budgeting Advice

How You Can Lower Your Expenses

Arrange a Debt Repayment Plan

To negotiate, contact your creditors via phone, email, or letter to explain your financial situation, and offer to pay an amount you can afford.

Save on Utility Bills

Compare energy providers to find a cheaper deal. Use energy-efficient appliances. Reduce water usage with low-flow fixtures.

Save on Groceries

Shop with a list to avoid impulse buys. Buy store brands instead of name brands. Look for sales and use coupons.

Cut Back on Non-Essentials

This includes dining out, entertainment, subscriptions, and luxury items. Look for free or low-cost entertainment options and cook meals at home.

Transportation Costs

If possible, use public transportation, carpool, or consider biking to work. If you own a car, maintain it regularly to avoid costly repairs.

Negotiate Bills

Contact service providers (like phone, internet, and cable) to negotiate a lower rate or switch to a cheaper plan.

Consolidate Debts

If you have multiple debts, consider a debt consolidation loan or a balance transfer credit card (with caution) to lower interest rates.

Sell a Financed Car

When you sell a financed vehicle, the proceeds can be used to pay off the remaining loan balance.

Use Cash Instead of Credit

To avoid accumulating more debt, use cash or a debit card for your purchases.

Seek Professional Advice

If you’re struggling, consider contacting a debt advice service like StepChange or National Debtline. They offer free, confidential advice.

If you still find yourself struggling to make ends meet, there’s no harm in exploring other options. In the next section, we’ll talk about how seeking a refund could be a solution worth considering, and I’ll guide you through the process.

How to gather evidence of an unaffordable loan

Compiling strong evidence to support your claim that a loan was unaffordable is essential for increasing your chances of a refund.

Here’s a detailed guide on how to gather the necessary documentation and submit additional proof:

Bank Statements: Collect bank statements for the period you took out the loan. These statements should cover at least three to six months before and after the loan application. Look for income deposits, regular expenses (rent/mortgage, utilities, groceries, transport), and other outgoings showing your financial situation.

Payslips: If employed, gather your payslips for the same period as the bank statements. These will help verify your income and provide a clearer picture of your financial stability.

Benefits or Other Income Sources: If you received benefits, pensions, or had any additional sources of income, gather documentation to support these. This includes letters from the Department for Work and Pensions (DWP) or any other relevant authority.

Credit Reports: Obtain a copy of your credit report for when the loan was taken out. Credit reports provide information about your credit history, including other loans, credit cards, and debts you had at the time. This will help paint a broader picture of your financial commitments.

Loan Agreements and Terms: Keep copies of the loan agreement, terms, and conditions, showing the amount borrowed, interest rates, repayment terms, and associated fees.

Correspondence with Lender: Save any emails, letters, or communications you had with the lender during the loan application or repayment process. This can include correspondence related to late payments, missed payments, or financial difficulties.

Financial Hardship Evidence: If you experienced financial hardship during the loan period, gather documents that provide evidence of this. This could include redundancy letters, medical certificates, or any other relevant documents that affected your ability to repay the loan.

Other Debts and Financial Commitments: List all other loans, credit cards, and debts you had when you took the loan. Include details of the lenders, outstanding balances, and repayment amounts.

Budgets and Expense Sheets: If you kept any budgeting records or expense sheets during the loan period, include these to demonstrate how your income was allocated and if there was a financial shortfall.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

The amount of money you will be refunded will be based on when the lender realised you couldn’t afford the loan.

This may have been at the start of the loan if, for example, they didn’t do a sufficient affordability check or creditworthiness assessment when you were applying.

You’re best asking for a full refund on all interest and charges; when it gets sent to the Financial Ombudsman Service, they will decide what’s fair.

This way, you’re maximising what you might get.

In addition, if any of the ‘extra ammunition’ bullet points above were broken, you should ask for additional compensation because your situation was mishandled when you informed the lender of your circumstances.

Case study: Marie’s refund request went to the financial ombudesman and they ordered Amigo Loans to pay back £500. The debt collectors were told that they no longer needed to collect.

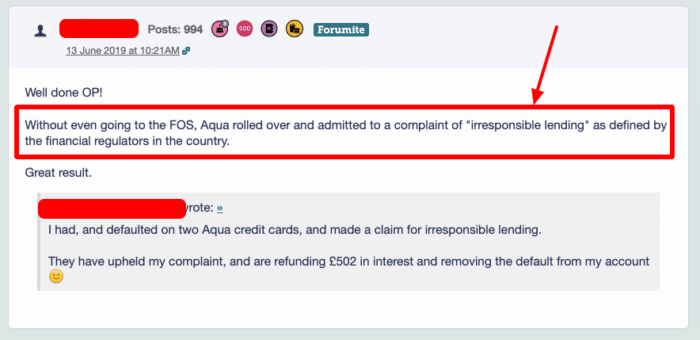

Another example, as shown below, is Aqua repaying interest on credit cards and removing defualts frm credit files, fortunatly without further action from the FOS.

The first step before you make a claim is to collect some data:

Go to CreditKarma and get a copy of your credit file. We do this because sometimes when you make a claim, the lender will delete your loan from your credit file, and we may need all these details if we have to escalate to the Financial Ombudsman Service.

2. The next thing to do is ask the lender for all the details about your loan. Under the new GDPR regulations, you can make a ‘subject access request’ for free.

To get these details, send the template below via email:

I am making an irresponsible lending claim. To help me with my claim please send me details for all of my loans, showing when each loan was taken out, the amount of interest and fees that were added and what I have repaid to date.

If any of my loans have been sold to a debt collections agency then please let me know the date of the sale and the name of the debt collections agency.

Under the General Data Protection Regulations you are not allowed to charge me for requesting this information.

The loans that you gave me were unaffordable and therefore I should not have been approved. Please refund all interest and any charges that I have paid. The refund should include statutory interest. Finally any negative information should be deleted from my credit file.

Get this letter as an A4 Template.

I’ve put the letters you’ll need into A4 Templates to simplify this process. You can simply input your details (name, address, etc), print, and send! It couldn’t be easier.

The regulations say you must be sent this information within one month. Also, this email officially starts the complaint, which gives the lender eight weeks to reply.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Once the lender has sent you a full list of your loan details, you can send a full complaint. Don’t worry; this is very simple; just follow the template, no need to do calculations or read complex law – I’ve done that for you!

Everyone’s story is different, so just delete the sections in the template below that don’t apply:

I’m following up with some additional details regarding my irresponsible lending claim that I sent via email on DD/MM/YY.

I have had loans with you between the dates of DD/MM/YYYY and DD/MM/YYYY.

The monthly repayments that you were charging me was such a large proportion of my income that I was forced to borrow again.

Between the dates of DD/MM/YYYY and DD/MM/YYYY my average net income was around £X a month.

If you have a dependents such as a wife and kids to support, add details here. Eg. My wife and I have two children which we must support. Child tax benefits averaged around £X a month.

My monthly expenses totalled around £X a month. This is made up of £X rent/ mortgage, £X council tax, £X bills, £X transport costs, £X clothes, £X supermarket shop, £X child expenses and £X for other debt repayments (loans and credit cards).

Looking at my income and expenses, it’s clear that there is no way I could afford to make the repayments on your loans. I had to take out other loans and credit cards to ensure that I could pay living expenses for the next month.

As a lender you should have realised when you lent to me and from the number of times I had to borrow more that my level of debt was increasing. It was irresponsible of you to lend to me in the first place and to continue to do so. [Add specific details if you have them – eg. How many loans, how often, how much etc.]

If you would have checked my credit file, you would have seen that I had other loans and credit cards and would have seen that I had issues such as late payments/ credit defaults/ CCJs.

Given all of the above, it’s clear that I should never have been approved for these loans as they were clearly unaffordable. Please refund all interest and any charges that I have paid. The refund should include statutory interest. Finally any negative information should be deleted from my credit file.

Get this letter as an A4 Template

I’ve put the letters you’ll need into A4 Templates to simplify this process. You can simply input your details (name, address, etc), print, and send! It couldn’t be easier.

Send the letter and keep a copy for your reference.

Now wait. The lender has up to 8 weeks to reply. When they do reply, one of three things will happen:

You get a full refund, are happy, and can cash that cheque!

The lender offers you just a small amount that you’re not happy about

The lender rejects your claim

In circumstance 1, congratulations! In circumstances 2 and 3, go to step 3 below.

Step 3 – escalate to the Financial Ombudsman Service

Once you’ve received a response from the lender, it’s time to decide if you want to proceed with step 3.

A lender often rejects your offer, hoping you will just give up. This is very common with my readers, don’t worry; there is still a chance that you’ll get a refund.

Thousands of people like you have escalated their claims to the Financial Ombudsman Service (FOS) and got a payout.

The FOS has reported that loan affordability complaints are the most common and have the highest chance of being awarded in your favour.

If you got an offer that is smaller than expected

Once you’ve got an offer from the company, you should consider it carefully. The best way to weigh it up is to look at what the refund is compared to the total amount of interest you paid across the lifetime of your loans.

You may want to take it to the FOS if it’s just a small proportion. We’ve seen people get 20x what they have been offered in the initial refund.

Really there’s no downside to escalating the FOS, as there’s no scenario where the original offer will not be valid.

Also, remember to ask to have any negative credit bureau reports removed from your file before accepting the offer.

They might not be able to do this, but there’s no harm in asking before you accept the offer; however, once you’ve accepted the offer, they will be less likely to help you.

You have six months to escalate to the FOS as part of the loan refund process, so don’t hang about, just get it done.

Should I go to the Financial Ombudsman?

You should seriously think about sending your complaint to the Financial Ombudsman if:

The company does offer a refund, but you think it’s too low

The company says they’re not going to refund you anything.

The company doesn’t reply to your letter within eight weeks.

The company says that they can’t refund you due to selling the loan to a debt collector.

The company says they can’t refund you due to the loan age.

You believe the company have carried out fraudulent loan practices.

Beware, companies have been known to say that you don’t have any basis for your claim. However, they’re trying to dissuade you from escalating to the FOS. Many readers have had a refund, even after being told no by the company. Common things that they might say that you can ignore:

The company blames you for entering in the wrong details during the application – this is not a valid defence, as if you were desperate for money, you would say anything.

The company says you can’t claim because you showed that the loans were affordable by repaying them early – this is not a valid defence as they don’t know what other bills you may have had.

The company says that you were borrowing less and less over time – this is not a valid defence as they could still be unaffordable even if you are borrowing less over time.

The company says they didn’t have to do a credit bureau check – this is not a valid defence either!

The steps when you escalate to the Financial Ombudsman Service

The Financial Ombudsman Service will deal with your claim in two steps.

Step 1: An FOS Adjudicator will review your case and decide how much the refund should be. Most cases get settled at step one.

Step 2: If both the company and yourself accept the offer, step 2 doesn’t happen. If the company or yourself doesn’t want to accept the offer, it goes to a FOS Ombudsman for a final decision.

How to escalate your claim to the Financial Ombudsman Service

The first thing to note is that you should make a separate complaint for every company you’re dealing with. If you send it all together, it may confuse things.

There are lots of ways to send your claim to the FOS:

phone

post

online

The FOS website explains very clearly the steps you need to take.

After you have submitted the claim

You can expect to receive the first contact from the FOS in 2 to 3 weeks. Ideally, you would have submitted everything the FOS needs to process the claim.

However, if this is not the case, they may contact you for additional details, in which case you’ll have the opportunity to upload again.

Now you won’t get a formal reply from the FOS Adjudicator for around 3-4 months, as that’s how long it takes for the FOS to get a response from the lender and process your claim in the appeal process.

Could you legally write off some debt?

Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.