Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you moving to a new country but worried about your unpaid credit card debt? We’re here to guide you. Each month, over 170,000 people visit our website for advice on managing their debts.

In this article, we’ll explain:

What happens to your unpaid credit card debt when you move abroad.

The powers of creditors and debt collectors in other countries.

The effects of not paying your credit card debt.

If you can write off some of your debt, and how to do it.

How your credit history is impacted if you move abroad.

Dealing with debt can be tough, especially when you’re moving to a new place. Don’t worry; you’re not alone. We’ll walk you through your options and help you find a way to handle your debt that suits you.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Can My Creditors Chase Me for Debts if I Move to a New Country?

The short answer is yes. However, there are many nuances to it as matters can take on a whole new level of complexity depending on your specific financial situation.

It also depends a lot on how you’ve dealt with the creditor regarding your move abroad.

If you have been communicative with them and have left them a forwarding address, they will not be as aggressive with pursuing you but of course, they will be in contact with you and will expect you to pay it back eventually.

On the other hand, if you have purposefully moved out of the country to avoid your debt and have just vanished without informing your creditor, there’s nothing stopping them from starting a County Court Judgment (CCJ) at your last known address in the UK.

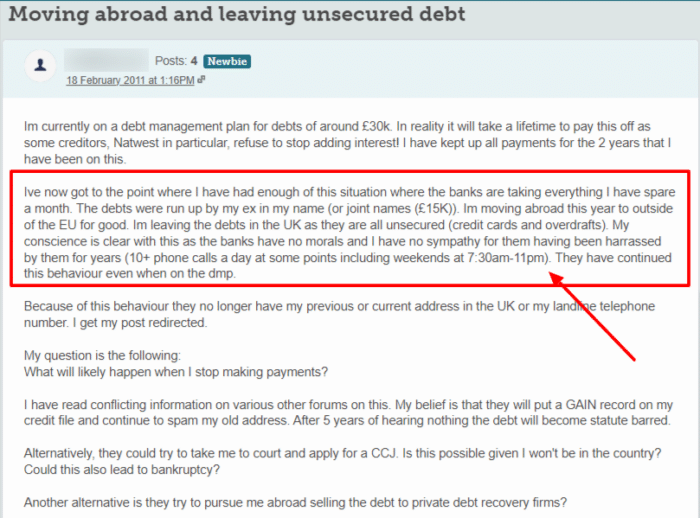

Take a look at this example:

If you are in a similar position as this forum user, you need to act cautiously and sensibly. You might think your conscience is clear, but legally you are not and other people might not agree with your moral standpoint – you still owe the money to your creditors!

If you have any assets in the UK, then your creditor can start a charging order which would seize these assets against your debt. Note that this can be done entirely in your absence.

Furthermore, a CCJ will reset the statute-barred timer for your debt. This means that if you were to ever return to the UK, you could still be answerable for your debt. You could even be sent a court summons.

Failing to attend courtwhen summoned is a criminaloffence, and you could get arrested when you enter the UK in the future, even if you think that the debt has become statute-barred.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Do Creditors and Debt Collectors have the Authority to Collect Money from Me in Another Country?

While it’s true that a lot of creditors have the right to pursue you for the debt you owe here in the UK, their powers and authority may be severely limited or even non-existent in other countries.

Your creditor may smartly hire a debt collection agency which has a partner or “sister” agency in the country to which you moved to. This sister agency can then pursue you for the debt you owe in the UK.

You can still dispute this practice as the agency would be attempting to collect debt you owe in the UK in another country. There’s a lot of grey area here, which you can definitely use to your advantage.

However, most of the time, debt collection agencies are much more well-versed in how debt collection laws work in different countries, and you are probably just going to end up being bested.

You also need to keep in mind that your creditor might be able to launch legal action against you in your new country. you will be bound by the laws of your new home, and, unlike the UK, other countries can imprison people for not paying their debts.

This is why my advice is always that you should always try to never let it escalate to that point. When accounts get sold or transferred (and that too internationally) it can become quite complex and difficult to handle.

However, you will probably find that you can quite easily make international bank transfers to your creditors or UK-based debt collectors. You can even use an international financial service company to organise or set up the payments for you.

Can My Debt be Sold to Another Debt Recovery Agency in My New Country?

Yes, it definitely can be sold to a debt recovery agency in the country you chose to move to.

Ultimately, moving abroad rarely works out if you’re just moving abroad to escape your debt. Everything is digital and connected and it’s normally very easy to track people down.

Some countries such as Australia and Canada have reciprocating agreements with the UK which enables them to pursue debtors that have moved abroad to these countries.

Thus, your creditor could definitely sell your account to a recovery agency in that country who would use the usual tactics that these companies employ in order to get you to pay up.

Once a debt is sold to a recovery agency in the country you moved to, you may start getting letters or phone calls from collectors regarding your debt. They may not have the power to get you to pay up but if you keep on refusing, they might get the court involved depending on what country you’re in.

You can opt to use the grey areas in international law to dispute the debts claim but again, this is generally a very risky idea. I would much rather suggest that you just figure out an affordable payment plan so that you can pay back the money you owe over a certain period of time.

If you’re moving abroad with the intention of running away from your debts, your credit history may not be of much concern to you.

However, I can definitely tell you that your credit history and credit file is something that you should be very concerned about.

In most countries, you will find it very difficult to obtain any kind of credit until you have been a resident of that country for at least some time. So, during your initial time in the new country, you might have to rely on your UK credit report in order to help you secure credit.

As you can probably expect, if you’re running away from your debts, your credit score will be in extremely bad shape. Thus, you will have a lot of difficulty securing any kind of loan or credit to buy a car or a home. Setting up your new life in another country with a bad credit score will definitely be extremely difficult.

What’s the Best Course of Action Regarding Unpaid Debts?

With all of the aspects I’ve highlighted today, I can say with certainty that the best course of action for you would be to take care of as much debt as you can while you’re still in the UK.

This may seem difficult if you have to leave on an urgent basis. In this case, I suggest that you seek advice from an independent charity. They have experts who will analyse your circumstances and help you draw up a plan that would be best suited to your needs.

In any case, you should always aim to pay off as much money as you can while you’re still in the UK. That way, once you do move abroad, you’ll be able to live a worry-free life without having to worry about any money that you owe.

You will also have the peace of mind of knowing you can return to the UK anytime you want without having to face any court action.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

We’ve all wondered – what exactly will happen if you stop paying off your credit card debt? Well, the answer is a whole lot of bother.

Your creditor will send you reminders and then demands that you pay any missed payments

If you don’t pay, your account will default

If you still don’t pay your debts, your creditor can choose to sell your debt to a debt collection agency or employ an agency to chase you for the missed payments.

If you don’t pay the collectors, your creditor or the collection agency might be able to take legal action against you to get their money back. Legal action usually starts with a CCJ.

Conclusion

In the end, all I have to say is that in today’s digital age, everything is connected. Just because you’ve moved abroad does not mean that your debts are not going to follow you there.

Be sure to be transparent with your creditors about why you’re moving out of the UK and ensure that you’ll be able to pay what you owe to them regardless of your move.

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.