Can I Use a Home Equity Loan to Buy Another House?

Representative example: If you borrow £34,000 over 15 years at a rate of 8.26% variable, you will pay 180 instalments of £370.70 per month and a total amount payable of £66,726.00. This includes the net loan, interest of £28,531.00, a broker fee of £3,400 and a lender fee of £795. The overall cost for comparison is 10.8% APRC variable. Typical 10.8% APRC variable

Representative example: If you borrow £34,000 over 15 years at a rate of 8.26% variable, you will pay 180 instalments of £370.70 per month and a total amount payable of £66,726.00. This includes the net loan, interest of £28,531.00, a broker fee of £3,400 and a lender fee of £795. The overall cost for comparison is 10.8% APRC variable. Typical 10.8% APRC variable

Are you wondering how to use the value of your house to buy another? This is a common question and we’re here to help.

This article will explain how you can use a Home Equity Loan to buy a second house. We’ll guide you through:

- Understanding what home equity is.

- Knowing the true cost of a bad home equity loan.

- The process of applying for a home equity loan.

- Weighing up the good and bad sides of home equity loans.

- Using home equity to buy a second home or an investment property.

Every month, over 6,900 people visit our site to learn about loans that are safe. We know it might feel big and scary, but remember, you’re not alone. We’re here to help you understand Home Equity Loans.

Is it possible to do it?

It is possible to use your home equity to buy another house. You may want to unlock your equity to contribute a lump sum towards a second home deposit or have enough existing home equity to buy another property outright. You may even want to make a second home purchase to rent out as an investment.

You can do this in theory, but you will still need to prove that you can repay the initial home equity loan, and then you will need to prove you can afford the second home mortgage while also declaring you have a home equity loan. As I see it, buying a second house for some people is a solid option, but you still need to be approved for all the credit required to make it happen.

How much can I use?

You can utilise no fixed amount of equity to help you buy a second home. It will depend on your financial situation and proving you can meet the payments. However, the maximum amount of equity a lender will allow you to access is often between 80% and 85%. So you will be unable to use more equity than this in most cases. As mentioned earlier in the article, the amount of equity depends on the lender.

» TAKE ACTION NOW: Compare deals from the UK’s leading lenders

Can I use it to pay off my current mortgage?

Using a home equity loan to pay off your current mortgage or even a proportion of it is possible. This can be beneficial if the loan has a better interest rate than what your mortgage is charging you. However, you should consider all other applicable fees, such as loan closing costs and early mortgage repayment fees. It might not be a good strategy for you.

Buying a second home vs an investment property

The difference between buying a second property and buying a new property to generate rental income is usually clear-cut. The former is purchasing a home you will use exclusively at different times of the year. For example, buying a house by the coast or in the Lake District for summer holidays with the family.

The latter is when you buy a second property that will be rented out to other people who pay to live there – or pay to holiday there. In this case, you’ll usually require a buy-to-let mortgage instead of a standard residential mortgage.

Lender |

APRC |

Monthly payment |

Total amount repayable |

|---|---|---|---|

| United Trust Bank Ltd | 5.09% |

£217.17 |

£26,060.42 |

| Equifinance | 5.65% |

£218.14 |

£26,177.08 |

| Selina | 6.34% |

£219.34 |

£26,320.83 |

| Pepper Money | 6.86% |

£220.24 |

£26,429.17 |

| Together | 7.2% |

£220.83 |

£26,500.00 |

| Norton | 7.61% |

£221.55 |

£26,585.42 |

| Masthaven | 8.25% |

£222.66 |

£26,718.75 |

| Evolution | 10.56% |

£226.67 |

£27,200.00 |

| Loan Logics | 11.2% |

£227.78 |

£27,333.33 |

Representative example: If you borrow £34,000 over 15 years at a rate of 8.26% variable, you will pay 180 instalments of £370.70 per month and a total amount payable of £66,726.00. This includes the net loan, interest of £28,531.00, a broker fee of £3,400 and a lender fee of £795. The overall cost for comparison is 10.8% APRC variable. Typical 10.8% APRC variable.

Search powered by our partners at LoansWarehouse.

What are the Advantages?

The benefits of using a home equity loan to buy a second house as a rental investment are:

- Increase your second property deposit – the deposit on your second mortgage may need to be bigger than your first, especially if you require a buy-to-let mortgage. A buy-to-let property equity loan can provide a lump sum amount that increases your second house deposit and makes it all possible.

- Lower interest payments – home equity loans typically have some of the lowest interest rates on the credit market. You could save money on interest by using a home equity loan instead of other options.

What are the Disadvantages?

Just like any source of credit, there are also downsides to using a home equity loan, such as:

- Increased equity at risk – everyone who becomes a homeowner exposes themselves to the risk that the housing market could topple against them and lose equity in a once more valuable home. If you buy a second property using equity, you increase the risk of dreaded negative equity.

- Debts are less streamlined – instead of having the same number of mortgages as homes, you will also have a home equity loan similar to a mortgage (but not the same!). Your debts are less streamlined and can be more tricky to manage.

- Closing costs – you’ll still be subject to closing fees and other potential costs.

Can I use a HELOC to get a second house?

You can also use a home equity line of credit (HELOC) to buy another property. A HELOC is similar to a home equity loan with some key differences, namely:

- It provides you with a line of credit over the draw period of many years. Homeowners can access this credit as they wish, a bit like using credit cards.

- Many lenders provide HELOCs with a variable interest rate rather than fixed interest.

- Repayments only begin after the draw period ends rather than immediately after the loan is taken out.

You can leverage home equity to access a large sum to be put towards a buy-to-let or standard mortgage or purchase a property outright.

Home equity loans for all purposes

- Stuck paying high interest on credit card debts & loans?

- Looking to fund a home improvement project?

- Dreaming of finally taking the once-in-a-lifetime trip?

Polly

“This was by far possibly one of the nicest experiences I’ve had getting a secured loan.”

Reviews shown are for Loans Warehouse. Search powered by Loans Warehouse.

Can I get it with a poor credit score?

It’s not impossible to get a home equity loan, HELOC or remortgage with a bad credit history, but it is more complicated. Lenders prefer to lend to people with a track record of being able to repay their credit on time and in full, so securing a home equity loan with poor credit can be difficult.

You might still be offered a loan or a new mortgage, but you may have to pay more interest than those with a good credit score. Search the market to discover all your options. If you don’t qualify for other alternatives because of bad credit, prioritising improving your credit score is a good idea.

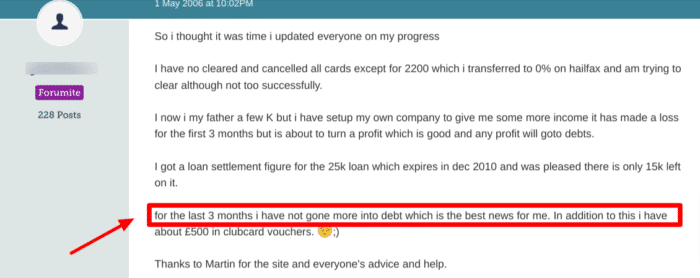

This MoneySavingExpert forum user was in a financial predicament and was looking for a way to get out of debt. Using advice from other forum users, he managed to get his financial situation under control.

Can I get a second loan?

It is possible to have two or more home equity loans at once, but there are second home equity requirements you must meet. This will only be possible if your income and financial circumstances prove you can afford to repay these loans together. When you apply for a second home equity loan, you must disclose that you already have an existing loan and possibly a mortgage.

When there is a second or third lien of credit, lenders can have more difficulty recovering money in the event of defaults and may be less inclined to lend to you.