Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you trying to understand whether you should repay your JD Williams catalogue debt and what actions to take if you can’t?

You’re not alone. Our website gets over 170,000 visitors each month, all seeking guidance on debt solutions.

In this easy-to-understand guide, we’ll share:

Who JD Williams is

The steps to take if you can’t pay

What happens when you fall behind on JD Williams payments

If paying the minimum amount each month is a good idea

Different ways to pay off a JD Williams debt

We know that not being able to pay a catalogue debt can be concerning. It can be hard knowing what to do or who to talk to. But don’t worry. We’re here to help you understand your options and choose wisely.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

What happens when I fall behind with payments

First, contact their customer support and explain your situation. Next, seek professional advice from a debt charity if you fall behind with JD Williams payments.

You may also try to set up a paydown plan with the company, which allows you to repay the arrears at an affordable rate. They should be able to set up a fixed repayment plan for you, including the arrears.

When you miss payments or make a payment late, the consequences can be far-reaching. Their customer support will attempt to contact you several times. Don’t ignore their messages.

Plus, you’ll accumulate late fees when you don’t pay on time. This includes:

An administration fee of £12 when their customer support tries to contact you.

JD Williams could report you to credit reference agencies, making it harder for you to borrow, and get further credit. Of course, this only comes after you’ve ignored several reminders and missed your payments.

You may be asked to pay the total amount owed to JD Williams.

Your agreement could be terminated.

JD Williams may start legal proceedings to recover what you owe.

A debt collection agency could get involved to recover the debt which you’ll have to pay for

In short, when you ignore their messages and don’t pay on time or at all, things get harder to settle. The amount you originally owed would have increased substantially, and you could be left facing a debt collector.

Understanding JD Williams late payment fees and how it works can help you avoid paying back more than you should.

You may also end up with a County Court Judgement (CCJ) being issued against you. This allows JD Williams to employ various means (e.g. bailiffs, repossessions, etc) to enforce the debt.

A CCJ stays on your credit report for six years, which may make it difficult to obtain credit in the future.

If you think JD Williams has moved too quickly to issue a CCJ against you, you can complain to the Financial Ombudsman Service via the Online Dispute Resolution platform. This is an online tool for consumers to resolve disputes about their online purchases. It was set up by the European Commission.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

When you have a JD Williams debt and want to sort things out, I strongly suggest you do so. There are various options available, including:

1. Ask for an informal agreement

The main thing is to stay in contact with JD Williams and let them know about your situation. Their support team may offer you a solution to set up a paydown plan. And, if they do, make sure you can afford to pay the amounts and that you can do so on time!

2. Think about a consolidation loan

I must caution that you apply for a consolidation loan only when you have several debts on top of a JD Williams debt. With a consolidation loan, all the money you owe various creditors is covered in a manageable monthly payment.

Unfortunately, paying off what you owe may take longer when you take this option. In short, your debt increases over time. I suggest you ask for independent advice on dealing with catalogue debtbefore choosing this option.

3. Consider a balance transfer

Another option is to consider a balance transfer. There are lots of 0% credit card offers being promoted across the online shopping sphere. And they could help get you back on track.

For example, JD Williams charges 39.9% APR. By opting for a balance transfer, you reduce the interest you pay, even if you’ll eventually have to pay the amount you owe on the credit card. That’s one of the major drawbacks of catalogue credit balance transfers.

Also, the interest rate can rise considerably once the 0% interest offer ends. So strive to pay off the balance whilst this offer is still in place to avoid racking up more debt.

What should I do if I can’t pay?

When you can’t pay a JD Williams debt, I suggest you stay in touch with the company. Don’t ignore any letters or messages you’re sent. Unfortunately, the problem will not go away. In fact, the situation could get worse, and the amount you owe will increase.

Next, contact a debt charity for free, impartial advice. For example, if you owe money to several creditors, consider contacting a debt management company like PayPlan. They offer free advice and could help you sort out the problem.

The main takeaway is to stay on top of the situation because the right debt solution could get you back on track with your finances.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

No, not really. It may sound like a good idea, but paying the minimum every month would not cover all the interest added to your account. You then fall into what is known as ‘persistent debt’.

This means that the monthly amount you pay only goes towards reducing the balance outstanding. It does not cover the interest, charges and fees that your debt accumulates.

JD Williams customer support should let you know about the situation when this happens. The company should offer advice on what you should do to get out of persistent debt. I suggest you pay more than the minimum monthly amount if you can.

Paying more and doing so regularly is the key to avoiding persistent debt with catalogue shopping.

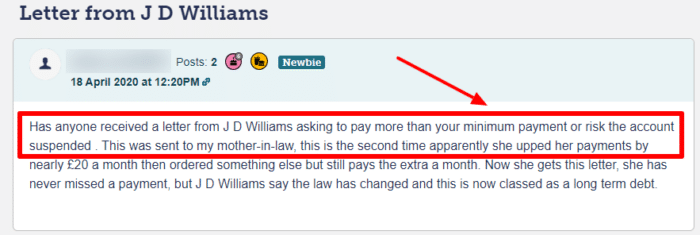

Remember, if you make only minimum payment (4% of the balance outstanding) every month, you risk falling into persistent debt. JD Williams may suspend your account if you are in persistent debt and you do not enter a paydown plan.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

MoneyNerd Limited does not provide debt advice. With your consent, we may introduce you to The Debt Advice Service, a trading style of Pacific Financial Solutions Limited, who can provide information about debt solutions and your available options. Fees may be payable if you enter into a formal debt solution. MoneyNerd may receive a referral fee. Your credit rating may be affected. Free debt guidance is available from MoneyHelper at moneyhelper.org.uk.