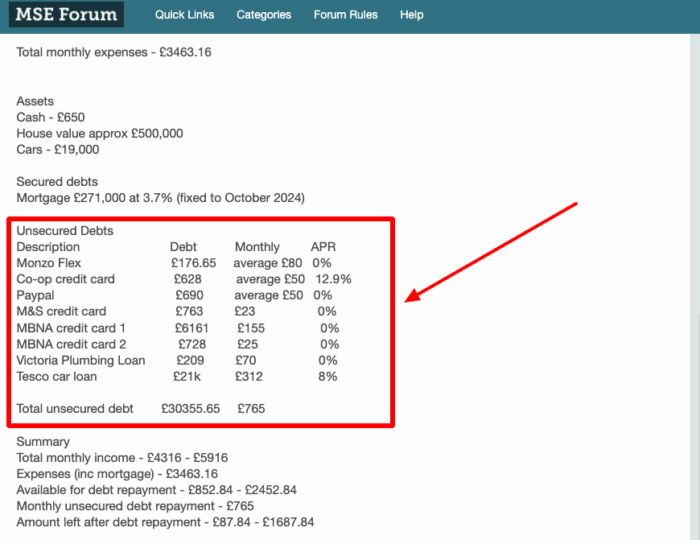

Average Monthly Debt Payments UK

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

In the UK, many people are paying off debt each month. As of September 2021, the average household pays back £373. This is a lot of money, and it is a big worry for many. This article will help you understand more about this.

We know you may have questions about this debt. You may want to know why it is going up and what you can do about it. Don’t worry, you are not alone. Each month, over 170,000 people come to our website for guidance on their debt problems.

Here’s what we’ll talk about in this article:

- Why debts are going up.

- How debt can make you feel stressed.

- What you can do if you are worried about debt.

- How much debt people in the UK have on average.

- How to use a tool that can help you pay off your debt.

We really do understand how hard it can be to deal with debt, as some of us have had to pay off debts too. We hope that this article will help you feel less worried and more in control of your money.

Let’s dive in.

What is causing the rise in debts?

When looking at the rising trend of average monthly debt payments across UK families, it’s impossible to ignore the complex web of factors that are causing this worrying trend. It’s very important to look into the many factors that have affected the level of financial stability among people in the UK. Here are some important things to think about:

- Inflation

- Rise in cost of living

- Unemployment

- Availability of credit

- Wage stagnation

- Rising childcare costs

The Unseen Burden: The Impact of Financial Stress on Well-being

When people in the UK talk about the effects of their growing debt, real financial problems are often the first thing that comes to mind. But under all of these problems is an effect on mental and physical health that is often overlooked but very real. When you look closely at how financial stress, mental health, and physical health are all connected, you can see a complex web of effects.

When it comes to mental health and debt, things often get stuck in a vicious loop where stress over money makes mental health problems worse and vice versa. When debts get bigger, worry and stress levels go up at the same time. This can lead to more serious mental health problems, like depression. The overwhelming fear of having too many bills can show up as trouble sleeping, constant stress, and a general feeling of hopelessness that permeates daily life.

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Average monthly debt in the UK

To begin understanding the scale of the issue, let’s take a look at the numbers!

- In September 2021, the average monthly loan repayment amount per household was £373. This is up 22% from the previous year and is the highest average amount in the last ten years.

- In September 2021, almost 10% of households in the UK reported that loan repayments were a heavy financial burden.

- In August 2022, the average amount of unsecured debt per adult in the UK was £3,877.

- In August 2022, the average household had £2,244 in credit card debt.

- The average amount of debt per household in the UK (including mortgage debt) is £65,346, which is an average of £34,337 per adult. This equates to 107.4% of average earnings.

- In August 2022, outstanding consumer credit lending reached a total of £205.1 billion, which was an increase of £690 million from the previous month.

- Within the aforementioned outstanding consumer credit amount, £62.4 billion was credit card debt, which averages £2,244 per household and £1,177 per adult.

It has been predicted that by 2025, household debt of all types will rise from £2,019 billion (where it stood in 2020) to £2,447 billion. This would increase the average household debt to £85,906.

If you have debts, you can use my free pay-off calculator to get an estimate of how much your debts will cost, including interest and your repayment period.

A loan payoff calculator might be a valuable resource if you have a loan debt in the UK and are struggling to meet repayments or just want to stay on track.

Common types of unmanageable debt

There are several different types of debt affecting UK consumers, with many people reaching the point of seeking help to manage their debts.

Below, you can discover the average debt amount of those who sought help in 2021 for these common types of debt:

- Personal loans – £7,503

- Credit cards – £6,853

- Catalogues – £1,813

- Overdrafts – £1,481

- Payday loans – £1,376

- Store cards – £1,146

Debt solutions in the UK

Creating a plan for managing debt well becomes very important when people are in a lot of financial trouble. The UK offers many options and solutions to help people come up with a plan to handle, lower, and finally get rid of their debt.

Debt Management Plans (DMPs): Debt Management Plans make it easier to pay back unsecured bills by making a personalised repayment plan. This means figuring out how much money you have available, taking out the amount you need for living expenses, and using the rest to come up with a reasonable, doable payment plan to show your creditors.

Individual Voluntary Arrangements (IVAs): An IVA is a formal deal between a person and their creditors that they will pay back their debts over a certain amount of time, usually five to six years. This means working with a professional to come up with a plan for repayment that creditors will agree to.

Bankruptcy: Bankruptcy is a way to get rid of bills if a person can’t afford to pay them back. There will be a formal solution, and your cash situation will be looked at in great detail.

Debt Relief Orders (DROs): DROs can be an alternative for those with lower debt levels, a low income, and minimal assets. It allows the suspension of debt payments and the potential writing-off of debts after a specified period.

Negotiation with creditors: An informal arrangement involves directly negotiating with creditors to establish an alternative repayment plan that is more in tune with your financial capability.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

Support with debt in the UK

If you are struggling with debt in the UK, there are plenty of guides on the MoneyNerd website to help you. Alternatively, contact one of the below organisations for free and impartial financial advice.

| Organisation | Phone | Website |

| Stepchange | 0800 138 1111 | https://www.stepchange.org/ |

| National Debtline | 0808 808 4000 | https://www.nationaldebtline.org/ |

| Citizens Advice | (England): 0800 144 8848 (Wales): 0800 702 2020 |

https://www.citizensadvice.org.uk/ |

Average Monthly Debt Payment FAQs

There are specific eligibility criteria for each of these options, so it’s a good idea to speak to a financial advisor to determine which is best for you.