Klarna Missed Payment – Should you Pay?

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Have you missed a Klarna payment and are wondering what to do next? You’ve come to the right place for answers. Each month, over 170,000 people visit our website seeking advice on debt matters.

In this simple guide, we’ll explain:

- What to do if you’ve missed a Klarna payment

- The options Klarna offers to help you settle the debt

- How your daily credit limit is checked by Klarna

- The impact of a missed payment on your credit score

- How to handle debt collectors if you find yourself in that situation

In 2022, arrears on household bills increased by 68% from £1,739 to £2,9201. So, it’s quite common for people to miss payments.

If you find yourself in this situation, don’t worry! We are here to help you find the answers you need to manage your Klarna debt.

How They Deal With Failed Payments

When you don’t have the funds to make a Klarna payment on time, talk to Klarna customer support before the due date.

They may be able to offer a solution. That said, Klarna tries a second time two days later when a payment request fails.

If that request also fails, you’ll receive:

- A statement of the full amount owed to Klarna

- You’re given 15 days to settle the outstanding

- You won’t be able to use Klarna till you make the payment.

Your account is marked in arrears until Klarna, and you receive a Klarna account block until they receive the money owed.

Don’t ignore any messages because sorting out the problem at this stage could save you a lot of stress, hassle, and the Klarna Financing consequences.

When It Gets Tougher

Problems start when Klarna can’t get in touch with you.

Klarna will pass details to a debt collection agency (DCA) as the consequences of Klarna late payment. It could happen after they attempted to contact you by text, email and letter.

A debt collector is persistent. They will contact you by phone, letter, or even knock on your door.

Avoid this when you can because dealing with Klarna debt collectors can be ultra-stressful. It can also lead to issues with County court judgement (CCJ) and Klarna.

You can resolve the matter when a debt collector gets in touch. You can:

- Pay the amount in full.

- Return the goods you purchased using Klarna (in some instances)

Klarna tells the debt collection agency when you pay the outstanding. Klarna never sells debts to collection agencies on amounts owed on their Pay in 3 and Pay in 30 schemes.

Debt Solutions Comparison

Dealing with debt can be challenging and scary. But don’t worry; there are different debt solutions that can help you manage your finances effectively.

These are:

| Debt Solution | Description | Formality | Debt Type | Debt Range | Legally Binding | Impact on Credit Score | Asset Risk | Monthly Payment | Duration | Creditor Agreement Required |

|---|---|---|---|---|---|---|---|---|---|---|

| Debt Management Plan (DMP) | Agreement to pay back non-priority debts in one monthly payment. | Informal | Non-priority debts | Any amount |

No | Yes | No | Varies | Varies (until debt is paid) | No (but creditors must be informed) |

| Individual Voluntary Arrangement (IVA) | Agreement to pay back all or part of your debts over a set period. | Formal | All or part of debts | Usually over £10,000 | Yes | Yes | Possible | Fixed | Fixed period, usually 5-6 years | Yes (75% by debt value must agree) |

| Debt Relief Order (DRO) | Freezes debt for a year and be potentially written off. | Formal | Non-priority debts | <£20,000 debt | Yes | Yes | No | None during freeze | 12 months | No (court approval needed) |

| Bankruptcy | Legal status for those who cannot repay debts, potentially writes off debts. | Formal | Unmanageable debts | Any amount, typically high debt | Yes | Yes | High | None during bankruptcy | Usually 12 months, then discharge | No (court process) |

| Consolidation Loan | Taking out a new loan to pay off all existing debts. | – | Multiple debts | Based on loan amount | Varies | Yes | Depends on loan type | Fixed | Depends on loan terms | No |

| Payment Holiday | Temporary relief or reduced payments offered by creditors. | – |

short-term financial difficulties | Any | No | Yes | Low | Reduced or paused payments | Break of up to 6 or 12 months, depending on circumstances, payment history, and creditor’s policy. | No |

| Informal Negotiation | Direct negotiation with creditors for reduced payments or extended terms. | – | All debts | Any | No | Possible | No | Negotiable | Until agreement terms are met | No |

| Statutory Debt Repayment Plan (SDRP) | Plan to repay debts over a reasonable time, with protections from creditor action. | Formal | All debts | Varies | Yes | Yes | No | Fixed | Varies, based on ability to pay | Yes |

| Equity Release | Homeowners release equity from their home to pay off debts. | – |

Debts of homeowners, typically older individuals aged 55+ | Varies and depends on property value | Yes | Yes | Asset (home) is used as collateral | Varies | 8-10 weeks timeframe from application to fund disbursement. Lifetime; repaid on house sale/death. | No |

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Delayed Payment vs Missing It

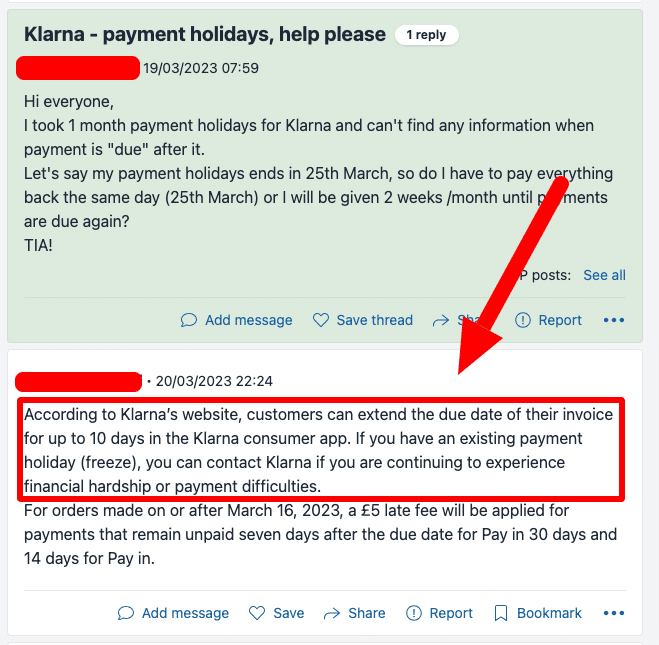

You can delay your Klarna instalment when you have trouble paying on time. But only for ten days on Pay in 3 and Pay in 30 plans!

It’s called ‘Snoozing’, a payment before the instalment is due. You can do this once in a single order.

A late payment when ‘snoozed’ won’t affect your credit score either. But if you still fail to pay what you owe, Klarna takes the matter further.

You can’t use the Klarna ‘Snoozing’ feature‘ on Klarna Financing.

When you fail to pay, credit reference agencies get notified. It could hurt your credit rating and your ability to borrow money when it happens.

Dealing With Debt Collectors

As mentioned, settling things could get tougher if a debt collector gets involved.

There’s the stress of dealing with a debt collection agency. There may be extra charges too!

I advise being truthful and letting the debt collector know about your situation. Never ignore them because they won’t go away.

You’ll have to pay what you owe.

Unless you can prove you returned the goods you bought using a Klarna buy now pay later service. Or you did not buy the goods.

It’s best to sort things out before it reaches the debt collection agency stage.

When it gets to this point, you could be reported to the credit bureaus and see your credit score suffer. In turn, this will make it very difficult to get any form of credit for the next six years, including mortgages, car finance, and even mobile phone contracts.

If you continue to ignore it, it could even go to court and see you issued with a county court judgement (CCJ), and believe me; this is something you don’t want.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

Will It Affect My Credit Score?

You might be concerned about the impact of Klarna on credit history.

However, a missed payment will not impact your credit score – even when you fail to pay on time. This applies to all Klarna buy now, pay later products.

» TAKE ACTION NOW: Fill out the short debt form

Account Blocked?

Klarna blocks your account when you fail to make a scheduled payment.

The block may last for twelve months! Even after you pay off what you owe. It may remain, thanks to the Klarna underwriting model. Unless your creditworthiness is good, that is.

To avoid this, contact Klarna when you are about to miss a payment. Work something out with them and set up a way to make the payment another way.

Klarna Contact Details

| Website: | https://www.klarna.com/uk/ |

| Phone number: | 0203 005 0833 (Local rate) |

| 0808 189 3333 (Freephone) | |

| 0203 005 0834 (COVID 19 related) | |

| Operating hours: | Mon to Sat 9 am – 6 pm Closed on public holidays. |