MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you worried that bailiffs may come to your home because of catalogue debt? We’re here to help.

Our website guides over 170,000 people each month to find solutions for their debt problems, so you’re not alone.

This article will clearly explain:

The process catalogue companies follow if you fall behind on payments.

What a CCJ is and how it can lead to bailiffs coming to your home.

Ways to manage your debt and avoid court action.

How catalogue debts can affect your credit score.

Where to get professional advice on dealing with debt.

We understand how stressful it can be to face the threat of bailiffs and loss of your things. It’s a hard spot to be in, but we’re here to help. We have loads of useful tips and easy-to-understand advice to guide you through this tough time.

Let’s start answering all your burning questions.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Can a Bailiff Come to My House for Catalogue Debt? What can Bailiffs Take?

A catalogue debt is a non-priority debt. This means that you should not prioritise it over your basic payments, such as living costs and utility bills.

Catalogue companies do not have the authority to send bailiffs to your home if you have been unable to make payments lately.

If you start missing payments, then the catalogue company will contact you in regards to why that is. If you are unable to pay them, then your account will default, and further action may be taken against you.

There is a chance that the catalogue company may hire a debt collection agency to collect their debt from you. You may get phone calls from a debt collector, but you must keep in mind that debt collection agents don’t have any extra-legal powers.

A debt collector is not allowed entry into your home unless you invite them in. They are also not allowed to take any of your possessions in order to pay for your debt. They can only inquire about your debt and ask you about the status of your payments towards your creditor.

It’s important for you to know that, unlike other types of agreements, such as Hire Purchase, you do not have to return the item to the company if you start falling behind on your payments.

If you still refuse to make your payments, then the catalogue company may take court action against you in the form of a County Court Judgment (CCJ). If the CCJ passes, you will be obligated to make payments to the catalogue company until your debt is paid.

If you fail to make payment to your CCJ, then the court could send bailiffs to your house. Keep in mind that the decision and authority to send bailiffs to your house lies with the court, not the catalogue company.

Bailiffs are not allowed to take items that don’t belong to you. They are also not allowed to take pets or items that you need in order to make a living or for your studies. They also cannot take items that you need for domestic purposes, such as kitchen appliances, washing machines, etc.

If they happen to take any of these items and you feel that they took something they did not have the right to seize, you can lodge a complaint and get your goods back.

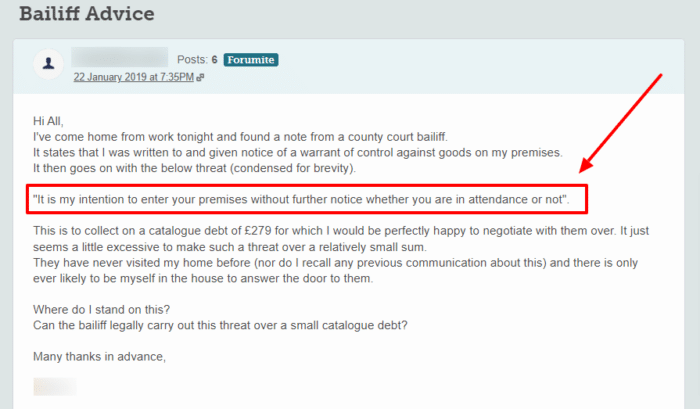

Bailiffs also can’t enter your home without your permission. Keep in mind that bailiffs are different to High Court Enforcement Officers and bailiffs generally can’t force entry to your home with a CCJ.

In this example, the bailiff is overstating their powers! Your legal rights against bailiffs are largely the same as your legal rights against anything else. The key difference is that bailiffs can enter your home if you let themin, if they have previously been in, or if you leave doors unlocked. They can also take items – including your car – that you leave on public highway or on your drive.

They can’t enter the forum user’s premises if they don’t let them in. If you get a similar letter from a bailiff, you can contact any of the charities that I have listed towards the bottom of this page. They will be able to tell you, with certainty, the exact limits on what your bailiffs can do.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

It’s a good idea to keep making regular payments towards your catalogue debt each month. You’ll definitely be asked to make a minimum payment each month but it’s not a good idea to keep making minimum payments for an extended period of time.

This is because if you keep making minimum payments, it’s likely that they will not cover the interest on your debt. Remember that catalogue debts usually have a considerably high interest rate.

Thus, if you keep making minimum payments, your debt might keep increasing to the point where it becomes completely unmanageable for you. Not only that but you’re also at risk of being in ‘persistent debt’.

Persistent Debt and Catalogue Debt Repayments

As mentioned earlier, if you keep making minimum payments, you will never be able to pay off your debt completely. This is known as persistent debt.

If you’ve been making minimum payments for a while, the catalogue company may send you a letter informing you of this and they might ask you to increase your payments.

If this isn’t manageable for you and you need help, then I suggest you contact a UK registered charity such as Stepchange for debt advice. . They have experts who will analyse your financial situation and give you debt advice as to how to move forward.

After 18 months of making minimum payments, you will have paid more towards interest and charges than you will have towards your actual balance. Your catalogue company will contact you and encourage you to take action.

If your account is still in persistent debt after 27 months, you will be contacted by your catalogue company again. Once again, they will encourage you to take action.

They may hire debt collectors as well even if you’ve been making minimum payments as they may be dissatisfied with the amount you’ve been paying.

If you’ve been in persistent debt for 36 months, the catalogue company should figure out a way to help you pay off your debt. This could be in the form of an affordable payment plan or by you clearing your debt using your credit card or a loan.

If you can’t pay your catalogue company using these methods, then they will consider options such as freezing interest or reducing the minimum payment on your account.

Keep in mind, however, that this may cause them to suspend your account. Not only that but it will be mentioned in your credit file and will definitely have a severe impact on your credit score.

If you’re having trouble getting out of persistent debt, I highly suggest you seek help from a professional such as from an independent debt charity. Charities that offer free financial counselling services include:

When you purchase an item from a catalogue company and it arrives, you should first make sure that it’s definitely something you want/need.

You have up to 14 days to cancel the order after you’ve received the item. This could be if the product is not satisfactory, if you’re having second thoughts about it or if you’ve realised that you can’t really afford it.

You may have to cover the postage costs in order to send the item back to the catalogue company but this will be a lot cheaper than staying in debt and paying back an item you don’t want or need.

If you’re having second thoughts about an item and feel that you can’t really afford it, I suggest that you think about whether you really need it. If you need it for your job or your studies, then I suggest you seek advice from a professional.

They can help you determine whether you’ll be able to realistically pay off the debt or not. Not only that but they can also give you advice in regards to what the best payment plan should be for you considering your financial situation.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Catalogue debts aren’t going to affect your credit score until you stop paying.

Once you have missed a few payments or defaulted on an account with your original creditor – which negatively impacts your credit score too – and your debt is sold to collectors, it will appear as a second collection account on your credit file and the original entry may be marked as ‘sold’ which doesn’t look good!

If they don’t add a second entry to your credit file, the entry for your original debt can be changed to add the debt collection company’s information.

These collection accounts will negatively impact your credit. They are visible for 6 years and will impact your ability to get credit or use some credit products during this time.

This is because companies use your credit file to see if you are a ‘high-risk’ customer – someone who might have difficulty paying their bills on time. If you have a CCJ, you have had such trouble paying back your debt that someone had to go to court about it.

Understandably, companies are going to be reluctant to give you credit!

After 6 years, it is no longer visible on your credit report and you should find it easier to get credit again.

You also need to be aware that any debt solutions that you use will also be visible on your credit file for 6 years, and your credit score may be affected. However, once these 6 years are over, your debt solution will no longer be visible, and you may find it easier to get credit again.

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.