How Much Will Debt Collectors Settle For?

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you puzzled about a letter from a debt collector? Not sure where the debt came from or if you should pay? You’re not alone. Many people face this problem, and we’re here to help. Over 170,000 people come to our website every month to get advice on debt problems.

In this article, we’ll help you understand:

- How debt collectors decide how much to settle for.

- Ways to make a good settlement offer.

- Tips for talking to debt collectors.

- How debt settlement affects different types of debt.

- The law around debt settlement in the UK.

Believe it or not, nearly half of individuals who deal with debt collection agencies have experienced harassment or aggression1.

Our team has lots of knowledge about these situations, as some of us have even had to deal with debt collectors ourselves, We really do understand how you feel, and we’re ready to help you work out what to do next.

Let’s start on this journey together.

What is a ‘Full and Final’ Settlement Offer and How Does it Work?

A debt settlement process can seem daunting which is why I suggest you seek advice from a debt expert first.

If you get a lump sum of money through inheritance because you sold an asset or you received a gift from family or friends, you could use it to pay off debt collectors.

It’s a good debt negotiation strategy in certain situations.

Depending on the amount of money you have, you may be able to pay off the full debt amount and become debt-free, which is a good option, as research shows that the average unsecured debt amount has increased by 27% year-on-year (to £16,174)2. This means that anything you can do to be debt-free is a golden opportunity.

If the lump sum you’ve received is less than the debt you owe, you could opt to make a ‘full and final’ offer to your creditors/debt collector.

A debt collector could agree to receive a lump sum payment, and in return, they may write off the rest of your debt.

While it’s something that some debtors can’t afford, a settlement is definitely a more hassle-free debt solution as compared to others.

This includes an Individual Voluntary Arrangement (IVA) or a Debt Management Plan (DMP).

It is because the full debt amount owed is paid off in one go rather than a series of monthly payments.

How Do I Make a Settlement Offer?

Settling a debt may seem like a complicated procedure but really, it’s all mostly common sense. That said, there are debt solution strategies that an advisor could walk you through.

Making a fair settlement offer stands a better chance of being accepted.

To make a settlement offer to your creditor or creditors, you’ll first need to figure out how much you’re going to settle for.

If you only have one creditor it’s fairly simple. You’ll just offer to pay them the entirety of the lump sum amount you have.

However, if you have multiple creditors, you’re going to need to divide the sum equally among them.

For example, suppose that the lump sum of money you have is about 80% of the total debt that you owe. In this case, you should offer each creditor 80% of the total amount that you owed to that particular creditor.

Always remember that before you send any money to creditors, ask them if they accept your offer. Be sure to get their acceptance in writing so that you have proof in case of any dispute in the future.

Make sure you keep all the letters and any other correspondence you have with debt collectors and your creditors. Just in case you need to refer to them in the future.

I suggest you keep these for at least six years after you have paid the settlement amount to your debt collector or creditors.

This is because a debt typically stays on your credit report and affects your credit score for six years.

The task requires a lot of micromanaging if you have a lot of creditors.

Every creditor may not be receptive to your offer and they might need convincing.

You’ll probably have to deal with them individually and hopefully, you’ll be able to get them all to agree to your offer. But I suggest you seek debt advice from one of the UK’s debt charities first.

To ask your creditors or debt collectors to accept a full and final settlement offer, use our free letter template.

Once all your creditors have agreed to your offer, be sure to send each of them the agreed-upon amount by the due date.

Make sure to keep proof of payment from each of them just in case a dispute comes up in the future.

» TAKE ACTION NOW: Fill out the short debt form

How Likely is it that My Offer will be Accepted?

This is a difficult question to answer as it varies from person to person.

Most creditors are unwilling to accept a full and final offer unless you have already debt defaulted in the first place.

If you have been making low monthly payments in the past or no payments at all, your creditors could be happy to receive a lump sum payment even if the amount is less than what’s owed.

Many creditors are also likely to be swayed by a full and final offer if they know that otherwise it would take you a long time to settle the full amount.

In most cases, it’s a good idea to be transparent about your situation. I suggest you share all financial information that you comfortably feel you can with your creditors.

Transparency in debt settlement is essential.

This will not only make them more understanding of your situation but it will also make them see that a full and final offer is actually the better choice.

Especially in the long run rather than a conventional monthly payment plan.

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

My Creditor has Proposed a Full and Final Offer, What Should I Do?

While this is extremely rare, it can definitely occur if you have been missing payments or providing a lot less in your payments than what was agreed upon.

Your creditor (or creditors) may be fed up with you falling behind on payments and they may want you to settle what’s owed.

Of course, there’s a high chance that you won’t have any money to fulfill this offer but if the offer is good, I suggest you take a hard look at your options.

If there’s any way you can secure the amount necessary to pay your debts, I suggest that you do.

It could also be a good idea to assess the situation and see if you could negotiate with your creditors to bring the settlement down to a more affordable sum.

For example, if they have suggested 60% of the total debt owed, see if you can bring it down to 40% or 50%.

Again, be thorough about your situation and financial information to make them understand that this would be a much better option than you slowly paying off your debt for what could be years.

Last but not least, read the letter they’ve sent you with the utmost care.

Ensure that they have agreed to write off the rest of the debt once you pay off the agreed-upon amount.

Make sure you get the information in writing.

Janine, our financial expert, explained that while debt collectors can visit your home for payments, they cannot come to your workplace, act threateningly, force payment, or discuss your finances with others. If they violate these rules, you can complain.

It’s important to know your rights and those of the debt collectors you’re dealing with to have an edge over the situation in case certain terms and not agreed upon. Here’s a quick table summarizing debt collectors’ rights.

| Debt Collectors Can | But They Can’t |

|---|---|

| Contact you by phone or mail. | Call you after 9pm or before 8am. |

| Conduct home visits (on rare occasions) and knock on your door. | Forbily enter your home, or stay if you ask them to leave. |

| Threaten to take you to court by suing you for payment on a debt. | Harrass you, including threats of violence, repeated calls and visits, or abusive language. |

| Negotiate a debt settlement. Tip: make sure to get this new arrangement in writing. | Visit your workplace. |

| Access your bank account, but only after a court judgment has been made. | Take anything from your home or threaten to do so. |

| Sell your debt. | Speak to other people about your debt without your permission. |

| Contact you frequently. | Keep doing so if you request that they reduce communications. |

Possible Drawbacks of Full and Final Settlements

I’ve listed some of the possible drawbacks of making a full and final settlement here:

- You must have enough money to make an attractive offer to creditors

- Creditors could demand you pay the full debt amount

Plus, creditors could mark debts as ‘partially settled’ debts on your credit report. It would make getting finance in the future for up to six years.

Will This Settled Debt Show Up in My Credit Report?

Debt settlements are a sigh of relief for any debtor but just like most debt solutions, it’s going to stay in your credit report for a while.

Once you settle your debt, your creditors will mark the debt as ‘partially settled’ on your credit file.

It will show other lenders that the complete amount was not paid back by you in order to settle the debt.

It will negatively impact your ability to secure credit in the future.

The record of a debt settlement stays in your credit file for 6 years after it was settled.

Keep in mind that if your debt defaulted, then it’s going to stay in your credit file for six years after the date it defaulted.

In short, having a County Court Judgement (CCJ) of a credit report impacts your credit rating.

Reaching a partial settlement in regard to the debt does not change this.

The psychological benefits of debt settlement

Being debt-free leaves you with a feeling of relief at not having to deal with paying off what you owe.

Rather than stress and anxiety, you feel:

- Happiness

- A sense of life satisfaction and well-being

The Office for National Statistics (ONS) carried out a study which identified that people in debt felt a sense of subjected well-being at being debt-free.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

Impact on different types of debt

It’s worth noting that “priority creditors” have more powers to get debts paid than non-priority creditors.

As such, you may find that a priority creditor is less likely to accept a full and final settlement offer.

Priority debts include:

- Mortgage or rent arrears, and you’re being threatened with court action

- Council tax arrears

- Utility arrears where the supplier is threatening to disconnect you or install a prepayment meter

If you’re unsure what to do, I suggest you contact one of the UK’s leading charities that provide free debt advice.

My Creditors Refused to Settle Debt, What Should I Do?

While getting your offer refused can definitely be discouraging, you still have the lump sum of money.

As long as you have that, there are other options you can pursue to pay off your debt.

For example, you can opt for an Individual Voluntary Arrangement (IVA).

An IVA is typically a process that lasts five years where you make payments to your creditors each month.

However, if you have a large sum of money at hand, you can opt to pay off your creditors at once using that amount rather than choosing a monthly payment method.

However, you should keep in mind that when you choose an IVA, even if you pay it all at once, a record will stay on your credit history for 6 years after it was initiated.

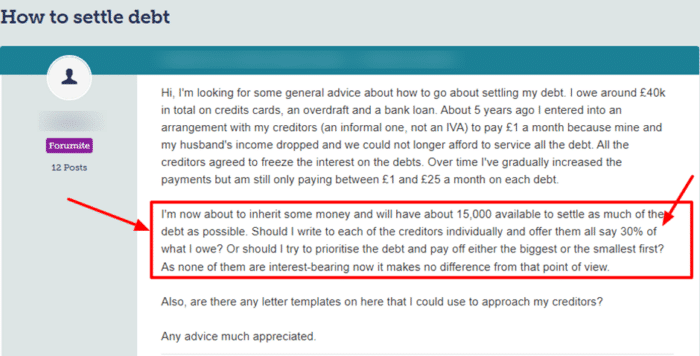

See the question one person asked on a popular forum about paying off debts.

Source: Moneysavingexpert

What is a Debt Management Plan (DMP)?

Alternatively, you could consider a Debt Management Plan (DMP) if you happen to receive a lump sum.

You could contact an independent charity such as Payplan or StepChange to help you put together a debt management plan.

They’ll assess your financial information and give you advice on how much you should be paying as part of your debt management plan each month.

You could also consider a Debt Relief Order (DRO) if you are not a homeowner and meet the other eligibility criteria.

I’ve listed them here:

- Your debt is less than £30,000.

- You do not have a lot of assets that have much value.

- You do not have a lot of income.

If you feel you are eligible for a DRO, you should contact a DRO adviser.

An adviser will assess your situation and help you fill in the application which will then be sent to an approved intermediary.

While the DRO adviser cannot charge you for advice, the DRO application does have a £90 fee.

Misconceptions about debt

Many people in debt are scared to deal with their debt because of stories they’ve heard.

Most of the time, these fears are usually unfounded, and I’ve listed some of them here:

- When I miss a payment on a debt, I will be blacklisted. A blacklist does not exist

- I could go to prison for debt. This is not true unless the debt is an unpaid criminal fine, Council tax (England only), business rates, child maintenance arrears

- If I don’t pay a debt to a utility supplier, they’ll cut off my supply. Not true

- I’ll be liable for someone else’s debt who lived at my address before I did. Not true

- My debts will go away if I leave the UK. Not necessarily true

Understanding the Legal Aspects of Debt Settlement

It’s important that you understand the legal aspects of debt settlement. I suggest you discuss your situation with a debt expert at one of the UK’s leading charities.

Charities provide free debt advice and could help you decide how to make a debt settlement offer.

That said, some debt situations require more than ‘advice’. In this instance, a solicitor could be of assistance.

This can be especially true if you need legal representation in a complex court case.

Potential tax implications of debt settlement

Although settling a debt can leave you less stressed, it does come with a few risks.

I’ve detailed these below:

- Late payments recorded on your credit file

- Potential fees and other charges

- Settlement fees

- Tax implications

The tax consequences of debt settlement for companies should not be overlooked.

When a company repays less than a debt’s total value, the amount forgiven is taxable.

However HMRC provides tax relief when a company is in financial difficulties.

In short, a company in trouble financially can benefit from paying less without paying 20% tax on a forgiven amount.

Negotiation Tips for Debt Settlement

Negotiating with creditors can be stressful especially if you’re struggling with your finances.

If you need time to seek debt advice from an expert, you can ask creditors to allow you a breathing space.

If they agree, and most should, it means that enforcement should stop. Plus, creditors shouldn’t continue charging interest and charges for sixty days.

That said, you should:

- Make sure all creditors provide their acceptance of a full and final settlement offer in writing. Keep copies in case you need them should a dispute arise which could be years later

- Do NOT send a lump-sum payment before creditors accept your offers

- It tends to be more legally binding if a creditor accepts money you were given by a relative or friend

- If the debt is significant, you may want a solicitor to draw up an agreement which creditors and you sign

- Always keep copies of letters and other correspondence

Staying On Top Of Your Debts

One of the hardest parts about being in debt is that the industry isn’t at all transparent.

One common tactic used by Debt Collectors is contacting you under multiple names and addresses.

Sometimes, it’s for practical reasons, but even then it can be confusing and intimidating. So it’s important to try to keep a level head and research what’s going on.

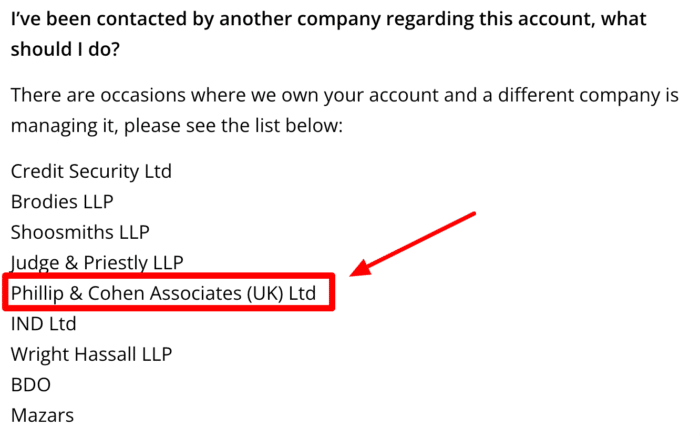

Some of the biggest debt collectors in the UK operate under multiple names.

- Robinson Way will sometimes contact you under the name Hoist Finance.

- Cabot Financial Group recently bought Wescot Credit Services

- Credit Style communicate as both Credit Style and CST Law.

- Lowell Financial also owns Overdales and collects debts under both names.

In fact, in the case of PRA Group, they’ve been known to use multiple company names. As you can see in the image below.

If you’ve been contacted by a debt collector recently, it’s worth going through your post and emails to check that you haven’t missed anything, just in case they’ve started writing to you under a different name.