What Are My Rights with Bailiffs? What Can They Take?

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you worried about a bailiff coming to your home or taking your things? If so, this is the right place for you.

Each month, more than 170,000 people come to our website seeking guidance on dealing with issues like this. You are not alone.

In this easy-to-understand guide, we will cover:

- Who bailiffs are and what they can do.

- Steps to take if a bailiff is threatening to visit your home.

- How to keep your property safe from bailiffs.

- Ways you might be able to reduce your debt.

- Where to find more help if you need it.

We know that dealing with bailiffs can be scary. Some of us have had to do it ourselves. We understand how you feel, and we’re here to help.

Read on to learn more about your rights and how you can handle this situation with confidence.

Do bailiffs have a right of entry into my property?

In most cases, you are not required to let bailiffs inside your home or place of business, and they are not permitted to enter your home between the hours of 9 pm and 6 am. When they go to a property for the first time, they can only use “peaceable means” to get in. They can’t use force in any way.

This indicates that they are able to enter through a:

- Door

- Gate

- Attached garage

They cannot enter your property by

- A window

- Climbing a wall or fence

- Climbing a locked gate or barrier

What happens if they are allowed access to your home?

The bailiff will enter your home calmly and orderly and start searching it as soon as they are inside. visit, they will not take any goods but instead will list everything they plan to buy and sell in the future.

Once a bailiff is on your property, they have the right to access all of the rooms within, and they are able to use force to obtain entry to other portions of the property.

They have the right to return at a later time, enter your home without your consent, and use whatever means are necessary to do so in order to remove the items in question.

However, they are only able to seize and confiscate property in order to cover the debt, such as unpaid council tax, as well as any expenses associated with the case, and nothing more.

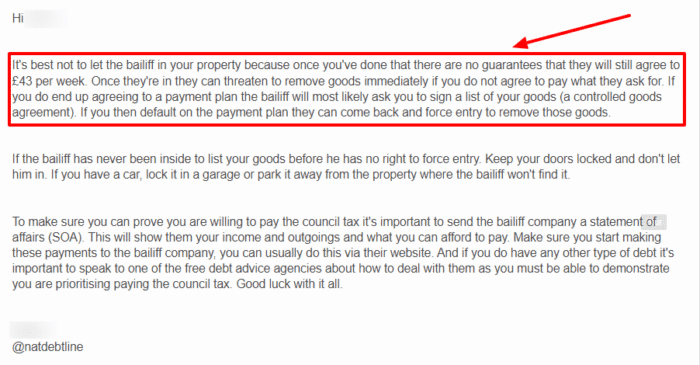

This is why I don’t recommend letting bailiffs into your home in any circumstances. Debt charities often give out this advice, as you can see from the National Debtline’s response on a forum about rights of entry.

When can a bailiff force entry?

There are very few situations where a bailiff can force entry, including:

- Collecting unpaid fines: They can force entry as a last resort if they have a Magistrates Court warrant.

- If they have gained peaceful entry before: if you have allowed them in peacefully before, they can force entry in the future if you do not let them in,

- County court bailiffs entering a commercial property: they can only do this if there is no living accommodation attached and they have permission from the court

- Collecting income tax or VAT – they have to have permission from the courts and have previously failed to enter a property peacefully.

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly payments

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

What happens if I receive a Notice of Enforcement?

If you have received a Notice of Enforcement informing you that a bailiff is going to call at your residence, you may be able to arrange some sort of payback to the lender first. If this is the case, you should do so as soon as possible. A bailiff is required to give you at least a week’s notice before their initial visit.

Make sure you are aware of who your creditor is, as it is possible that the person who first extended credit to you has already sold the debt to a debt collection agency. You also have the option of asking the court to put a hold on the bailiff’s activity by filing a motion on your behalf. Even if you are unable to stop the legal process, it is possible that you still have time to make an offer to repay the amount over a longer period of time.

You do not have to let the bailiff into your home in order to discuss this – you can talk to them through a window or keep them on the doorstep.

» TAKE ACTION NOW: Fill out the short debt form

Can bailiffs take everything?

No, bailiffs can’t take everything in your house.

There are strict rules on what bailiffs can’t remove from your property. These items include:

- Anything that belongs to someone else – this includes things that belong to your children

- Pets or service animals

- Vehicles, tools, or equipment that you need for your job or to study up to £1,350

- A mobility vehicle or any vehicle with a valid Blue Badge

- Anything permanently fitted to your home – kitchen units, etc.

Bailiffs also can’t take things that you need to live. These items can be anything that you use for your ‘basic domestic needs.’ They can take some of these things, but must leave you with:

- A table with enough chairs for everyone in your home

- Beds and bedding for everyone in your home

- A phone or mobile phone

- Any medicine or medical equipment that you need to care for someone

- A washing machine

- A cooker or microwave, and a fridge.

If you think that a bailiff has taken something that they shouldn’t, you need to complain immediately. I go through the complaints process below. You can also contact a debt charity for some advice. I have listed several charities that offer free advice at the bottom of this page.

What if I am a vulnerable person?

Before you start addressing the notice of enforcement, you should know that if you:

- Are disabled in any way or extremely ill

- Suffer from any kind of mental illness

- Have children or are pregnant

- Are under the age of 18 or over the age of 65

- Are dealing with a stressful situation such as the death of a loved one or unemployment

- Don’t speak English very well

You are considered a vulnerable person. This means that any bailiffs will have to follow some additional rules to ensure their visit is as easy on you as possible.

Furthermore, if any of these conditions apply to you, you can get more time to deal with the notice of enforcement. You can also get more time if the notice of enforcement was not sent to you properly by the bailiff.

If you fall into any of the above categories, you need to either tell the bailiffs yourself or get a relative or carer to do it for you. You can then contact the bailiff by phone or by post. I have a free letter template that you can use to explain your situation.

When you speak to the bailiffs, you need to:

- Tell them that you’re vulnerable

- Explain why you would find dealing with bailiffs more difficult than other people in the same situation

- Ask them to stop any visits in the future because it will cause harm and distress to you

- Tell them if a letter or a visit could make your situation worse – this could be the case if you have a mental health problem or a heart condition, for example.

Make a note of what you agree with the bailiffs about future contact. This will make it easier to argue with them if they don’t stick to this new agreement, or if you need to make a complaint.

How do I complain about a bailiff?

If you think that your bailiff has been unreasonable or behaved inappropriately, you can make a complaint. You can also make a complaint if you feel that they have broken any of the Financial Conduct Authority’s (FCA) guidelines.

Make your first complaint to your bailiff’s company or agency so that they have the chance to sort out the issue themselves. If you feel that they have not taken your complaint seriously enough or have not addressed your issue properly, you can escalate matters.

You can make any secondary complaint to the Financial Ombudsman Service (FOS). They will investigate and, if your complaint is upheld, your bailiff may be fined. You could even be owed compensation.

If your bailiff or their company is not registered with the FCA, you can make your secondary complaints to the Civil Enforcement Authority (CIVEA). CIVEA has its own set of guidelines and procedures for dealing with complaints against its members.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

How do I complain about a High Court Enforcement Officer?

If your bailiff is from the High Court rather than the County Court, they are probably a High Court Enforcement Officer (HCEO).

If you think that your HCEO has been unreasonable or behaved inappropriately, you can make a complaint. You can also make a complaint if you feel that they have broken any of the High Court Enforcement Officer Association’s (HCEOA) Code of Best Practice.

Make your first complaint to your HCEO’s company so that they have the chance to sort out the issue themselves. If you feel that they have not taken your complaint seriously enough or have not addressed your issue properly, you can escalate matters.

You can make any secondary complaint to the HCEOA. They will investigate your complaint thoroughly and provide you with a report if your complaint is upheld. If the HCEO’s behaviour was very poor, they may be fined, and you could even be owed compensation.

Can bailiffs come in if you are not there?

The vast majority of bailiffs do not possess the authority to enter your home if you are absent. However, depending on the type of debt owed, bailiffs may be able to enter a property even if the doors are locked, with the assistance of a locksmith. If a bailiff is collecting tax arrears or debts for criminal fines, then they can enter.

Bailiffs are prohibited from entering your home if you are not there, if there are only minors (those under the age of 16), or if there are people who are vulnerable. They will not come to your home if you have any vulnerable people living there, such as pregnant women, people who are ill or have mental health issues, or pregnant women. If you are considered vulnerable, the bailiffs are required to follow a specific set of guidelines.

How to avoid bailiffs entering your home

The most effective course of action is to do all in one’s power to prevent the entry of the bailiffs. It is crucial that you let everyone in the house know about the impending visitor and that they are aware of how important it is to keep the doors secured at all times. Teach your kids not to answer the door or let anyone else in.

In the majority of cases, the only way a bailiff will be able to enter your home is if you open the door for them or if you let them in yourself unless you have previously granted them access. You will receive at least a week’s notice prior to the initial visit, giving you ample opportunity to get ready for it. Even after you have received notice, you still have the opportunity to prevent the bailiff from calling by making arrangements to pay the amount.