MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.

Could you legally write off some debt? Answer below to get started.

This isn’t a full fact find, MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you puzzled by a sudden letter from Ruthbridge Debt Collectors? Maybe you’re asking if you must pay this debt or if it’s even yours.

Don’t worry, you’re not alone. Each month, more than 170,000 people come to our website seeking help with debt problems, just like yours.

In this easy-to-understand guide, we’ll help you:

Understand why Ruthbridge Debt Collectors have contacted you.

Check if the debt really belongs to you.

Find out if you’re able to pay the debt back.

Learn how to work out a payment plan.

See how you might write off some Ruthbridge debt.

Our team is made up of people who’ve faced the same worries as you. We’ve been in your shoes, so we’ll give you clear, simple advice on dealing with Ruthbridge Debt Collectors.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Why do Ruthbridge Debt Collectors Debt Collectors Keep Contacting You?

If you have run up some debt, you will usually be contacted by a debt collection agency, rather than the company itself, which can cause a bit of confusion.

If Ruthbridge Debt Collectors are contacting you, it’s probably down to outstanding debt, that you may have completely forgotten about or may not even be aware of.

As independent debt collectors purchasethe debt from other organisations, they don’t start making a profit until they get some payment from debtors.

This is why they are always so keen to get hold of you, and they may even consistently call or send out letters to try and get a reaction from you.

It is not unusual for debt collection agencies to use a range of tactics to try and get hold of the money you owe, but it may not be legitimate for them to do so.

Is the Debt Yours?

If you are being contacted by Ruthbridge Debt Collectors, the first step is to get a hold of written confirmation on the debt, and proof of where it originated, as well as the total value of the debt.

It may seem higher than you remember, as there could be interest added on that you are not aware of.

The debt collectors should be able to provide you with confirmation. If they can’t do this, you are not obliged to pay this debt.

If you receive written confirmation of the debt you owe from Ruthbridge Debt Collectors, you must take steps to pay it back.

If you can’t afford to pay the full amount, you may be able to arrange a payment plan or give them a partial payment to clear off the debt.

Do not ignore the debt collection company, though, as they are unlikely to just disappear, and it can cause extra stress if you are getting contacted often about your debt.

How to Cooperate With Ruthbridge Debt Collectors

At the end of the day, Ruthbridge Debt Collectors are running a business, and are looking to make money.

Unfortunately, debt chasing is often not dealt with in the best manner. It is a good idea to cooperate with the debt management company, as long as they are also following the appropriate guidelines.

These are some ways to do this.

1. Make contact

It can be easy to just ignore contact from Ruthbridge Debt Collectors, but this won’t make the problem go away.

In fact, the more you ignore them, the worse the situation will get, as unpaid debts may affect your credit rating if you owe debt.

You will also end up suffering from more stress and anxiety with incessant contact.

Even if you can’t make payment straight away, you should speak to them about your situation. Use our free sample lettertemplatesto help you communicate more effectively with Ruthbridge Debt Collectors.

2. Arrange payment

If you can only make small payments, it is better than paying nothing.

Most debt collectors will accept any payment, but they may ask for proof of your income and expenditure.

It is much better to pay it all off if you can, but if not, set up a repayment plan.

If Ruthbridge Debt Collectors are not willing to accept your situation or they are threatening to visit your home or other distressing behaviour, you can report them to the Financial Ombudsman.

You can contact the Financial Ombudsman on 0800 023 4567 or 0300 123 9123

How to Work Out a Payment Plan

The best way to work out a reasonable payment plan is to analyse your income and expenditure.

The most important bills should be paid first, such as your rent/mortgage and energy bills, as well as your budget for food.

If you need money for travel, you should keep that aside, and you can pay back whatever is left over.

If you can’t pay

Of course, it may be the case that you can’t afford to pay the debt back, and in this case, you should come to another arrangement.

For example, deferring the payment until you get paid, or you may want to enter into an Individual Voluntary Arrangement.

An IVA allows you to write off some of your debt, although you may not be able to access credit for five years after this.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

You may also consider setting up a Debt Management Plan. A DMP you to make single monthly payments to a debt charity, which distributes the funds to your creditors.

Another option is the Debt Relief Order (DRO). If you have only £75, or even less left after your essential payments, you may be entitled to apply for this.

A DRO provides debt relief for a 12-month period, after which the debts are usually discharged.

As a last resort, consider declaring bankruptcy (or sequestration in Scotland). Keep in mind that your assets may be sold to repay creditors. However, any remaining debts are typically wiped out after 12 months.

Next Steps

Work out what you can afford to pay back and speak to Ruthbridge Debt Collection Agency about entering into a payment plan or paying the debt off completely if you can afford to do so.

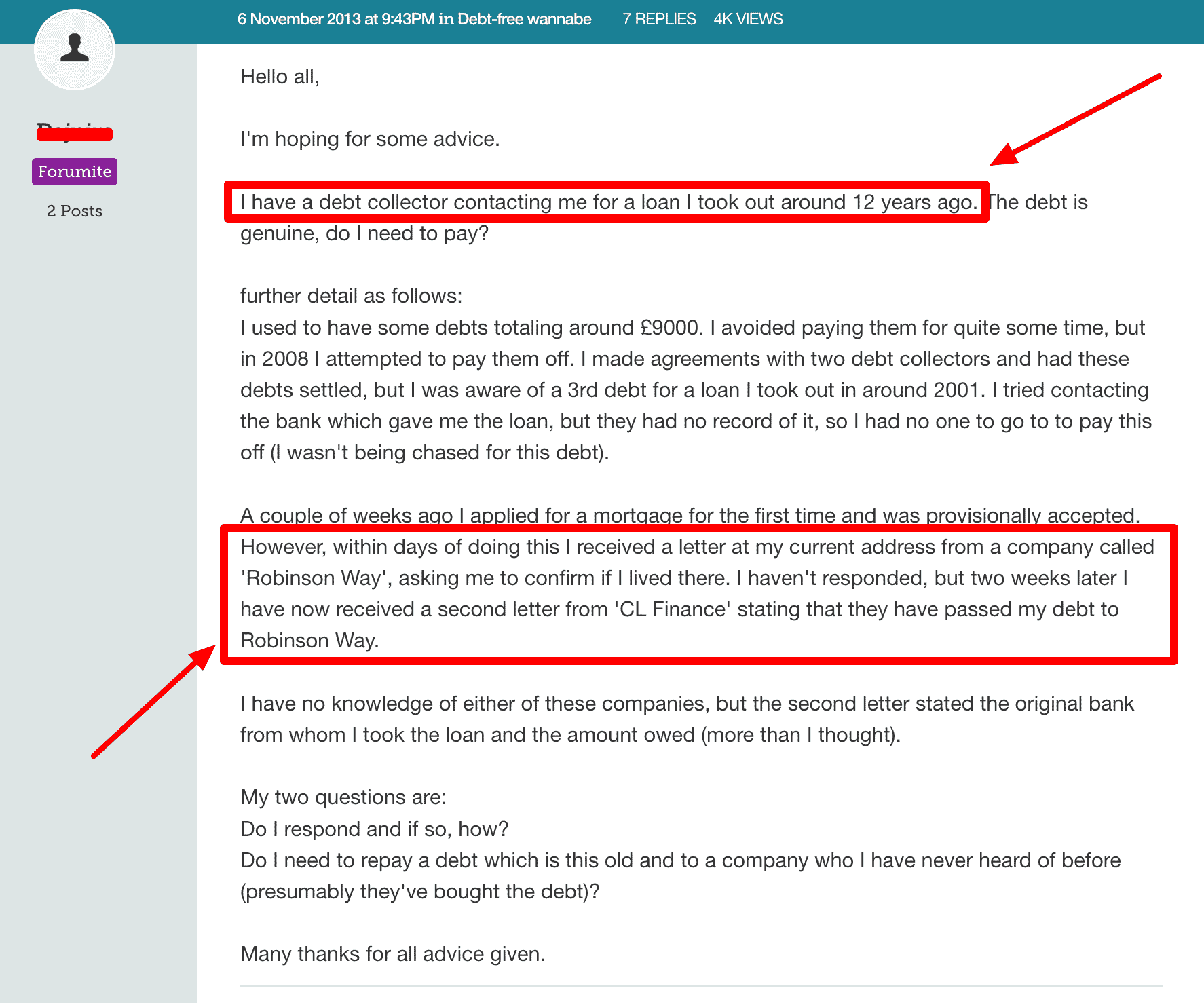

As you can see Robinson Way starting to chase a debtor mere days after their mortgage application and a full 12 years after the debt was originally chased.

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

MoneyNerd’s founder, Scott Nelson, has a decade of financial industry experience, including 6 years in FCA regulated loan and credit card companies. Troubled by a lack of conscience in the industry, he founded MoneyNerd to give genuine advice to those in debt and struggling financially.

Janine Marsh is an award-winning presenter and a valuable member of the MoneyNerd team. With a wealth of experience as a financial expert, she's been featured on BBC Radio 4, BBC Local Radio, and BBC Five Live, and is a regular on Co-op Radio.